Bookkeeping Services Statistics looks at how bookkeeping services is changing the way businesses manage finance work, reporting, payments, and day-to-day decisions. The numbers matter because this is not only a software category. It is a measurement of how much financial work still depends on manual entry, delayed follow-up, disconnected records, and decisions made after the useful moment has passed.

For the businesses that use bookkeeping heavily, the pressure usually sits in ordinary operating work: bank reconciliation, receipt capture, payroll records, sales categorization, month-end review, and tax-ready file preparation. When those steps are disconnected, finance teams spend too much time explaining status, correcting records, chasing evidence, and rebuilding reports that should already be available from the system.

The best way to read these statistics is to separate market growth from operational maturity. Market forecasts show how much vendors and buyers are investing. Operating statistics show whether the workflow is actually improving. Both matter, but they answer different questions. A large market does not prove a company has a strong process, and a strong internal process does not always require the most expensive platform.

This article treats the statistics as decision tools rather than decoration. The goal is to explain what the numbers mean for owners, office managers, outsourced bookkeepers, payroll providers, tax preparers, and accountants, and how finance leaders can use them to evaluate workflow quality, cash-flow visibility, risk, and productivity without relying on generic claims.

Key bookkeeping statistics

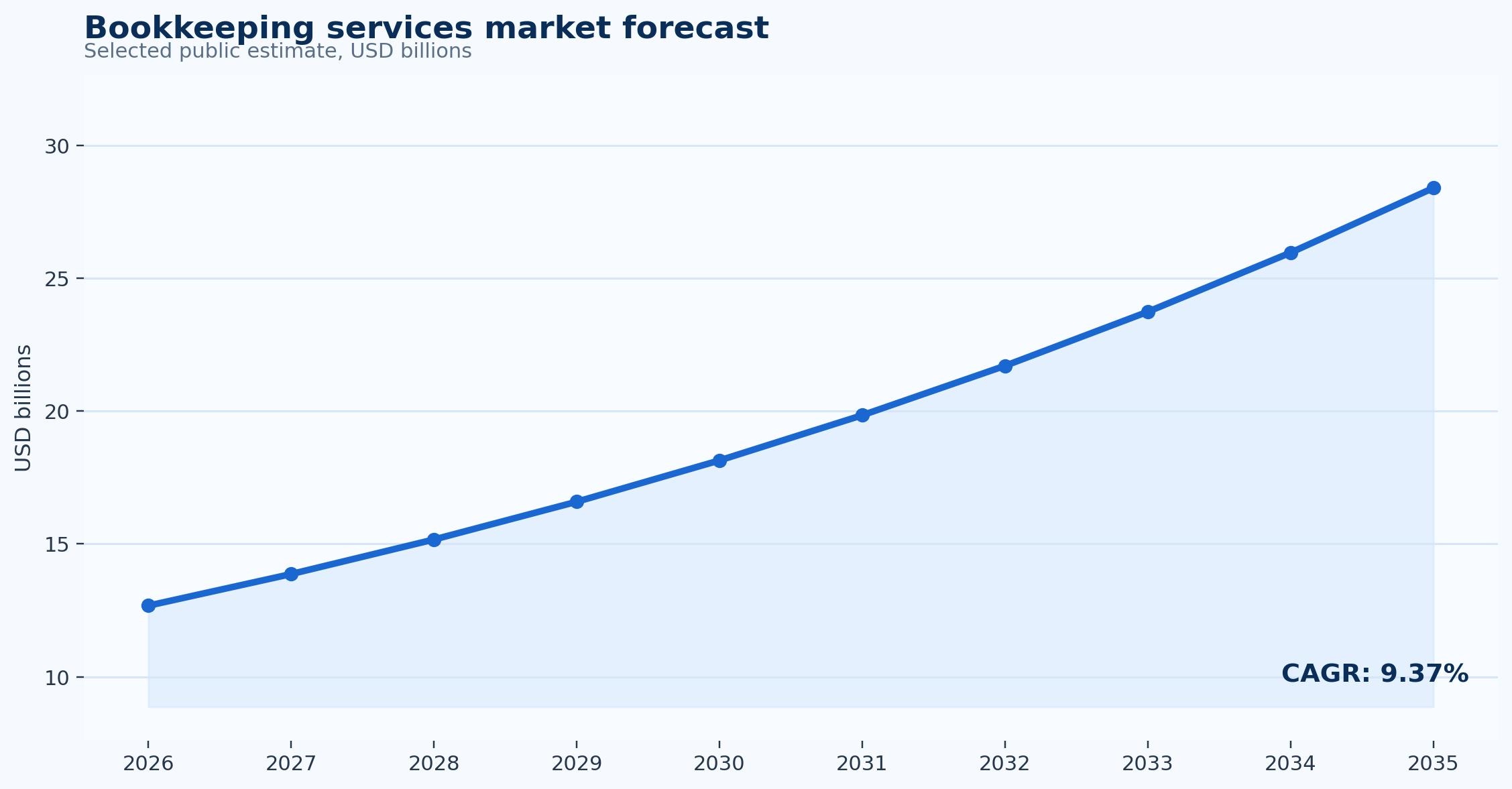

- The global bookkeeping services market was estimated at $12.68 billion in 2026 and projected to reach $28.39 billion by 2035.

- The implied forecast CAGR for that global bookkeeping services estimate is 9.37 percent.

- US payroll and bookkeeping services were estimated at about $80.9 billion in 2026.

- IBISWorld summaries put recent US payroll and bookkeeping services growth in the low single digits, reflecting a mature but durable services market.

- One public estimate projected bookkeeping services from about $12.67 billion in 2026 to $28.38 billion by 2035.

- Another estimate placed the 2025 bookkeeping services market near $11.59 billion and projected about $23.72 billion by 2034.

- Bookkeeping demand is closely connected to tax season, payroll support, bank reconciliation, receipt organization, monthly close, and cash-flow reporting.

- Important bookkeeping metrics include close timeliness, reconciliation backlog, uncategorized transaction count, receipt completeness, and review-ready financial statements.

- The selected market forecast moves from 12.68 to 28.39 in USD billions between 2026 and 2035.

- The selected CAGR for this category is 9.37 percent, which should be read as a directional market signal rather than a company performance benchmark.

- The strongest operating scorecard for bookkeeping should track close timeliness, uncategorized transactions, reconciliation aging, receipt completeness, payroll handoff quality, and review-ready reporting.

- The main workflow risks include misclassified transactions, missing receipts, unreconciled bank feeds, late payroll support, and tax-season cleanup work.

How to Read These Statistics Correctly

Bookkeeping Services statistics are easy to overread when every number is treated as a direct performance benchmark. A market-size estimate measures vendor revenue and spending activity. A workflow statistic measures how work is actually performed inside a company. A late-payment or cash-flow statistic measures business pressure. Those categories should be connected, but they should not be treated as the same type of evidence.

The first distinction is category demand versus process maturity. A business can buy modern software and still operate with weak controls if users keep approvals in email, update spreadsheets outside the system, or delay reconciliation until month-end. For bookkeeping, the practical test is whether the workflow changes daily behavior in bank reconciliation, receipt capture, payroll records, sales categorization, month-end review, and tax-ready file preparation.

The second distinction is adoption versus depth. A company may say it uses automation because one task is digital, but real maturity comes when status, evidence, ownership, and exception handling are visible together. That is why statistics about small-business recordkeeping needs, outsourced finance support, payroll and compliance work, cloud collaboration should be paired with internal baselines such as close timeliness, uncategorized transactions, reconciliation aging, receipt completeness, payroll handoff quality, and review-ready reporting.

Definitions also vary by company size. A small business may define success as fewer owner interruptions and cleaner tax records. A midmarket company may define success as faster approvals, stronger reporting, and fewer month-end corrections. An enterprise may define success through audit trails, segregation of duties, and policy compliance across entities.

The most useful reading method is to ask what decision the statistic supports. If a number helps a manager decide where to automate, which workflow to fix, which risk to control, or which KPI to watch, it has practical value. If it only repeats that a market is growing, it belongs in context rather than at the center of the business case.

How to Read These Statistics Correctly – practical statistics and checkpoints

- The future of bookkeeping services is shaped by automation, integration, reporting, and better workflow status.

- AI will help most with repetitive classification and exception triage before it replaces high-risk finance decisions.

- The next stage of maturity will connect bank reconciliation, receipt capture, payroll records, sales categorization, month-end review, and tax-ready file preparation into cleaner decision workflows.

- Companies that measure baseline quality before changing tools will be better positioned to prove improvement.

- A practical review rhythm is 30 days for baseline cleanup, 60 days for adoption review, and 90 days for confirmed process improvement.

Market Size and Growth Outlook

The market outlook for bookkeeping services shows continuing investment in digital finance infrastructure. Global bookkeeping services market estimates point to a move from $12.68 billion in 2026 to $28.39 billion by 2035, while US payroll and bookkeeping services were estimated at $80.9 billion in 2026. The chart below uses one selected public estimate as a directional view, not a universal definition of the entire category. That distinction is important because many finance software markets overlap with payments, automation, services, ERP modules, and analytics.

Growth is being driven by practical operating pressure. Companies want fewer disconnected tools, earlier visibility into status, and a better way to manage bank reconciliation, expense categorization, receipt organization, monthly management reports. The demand is not only for software screens. It is for a more reliable process that gives managers usable information before a delay becomes a cash, tax, customer, or audit problem.

Vendor categories are also expanding. Platforms that once solved one narrow task increasingly include integrations, dashboards, workflow automation, AI assistance, approval controls, and document storage. That broader packaging can increase market estimates, but it also reflects how buyers now evaluate solutions: they want a workflow layer rather than another isolated database.

The market-growth statistic is most useful when it is tied back to internal readiness. A growing category means more product options and more vendor claims. It does not automatically mean every buyer should implement a large system. A company should first identify the workflow bottleneck, the volume affected, the cost of delay, and the control risk created by the current process.

For finance leaders, the forecast supports a planning conclusion: bookkeeping will likely become more integrated, automated, and data-driven. Teams that still rely on email status updates, delayed spreadsheet exports, and after-the-fact cleanup will face a widening gap between how finance work is performed and how quickly the business expects answers.

Market Size & Growth Outlook – practical statistics and checkpoints

- The selected public forecast starts at 12.68 USD billions in 2026 and reaches 28.39 USD billions by 2035.

- The forecast CAGR used in the chart is 9.37 percent.

- Global bookkeeping services market estimates point to a move from $12.68 billion in 2026 to $28.39 billion by 2035, while US payroll and bookkeeping services were estimated at $80.9 billion in 2026.

- Market totals should be compared with operating metrics such as close timeliness, uncategorized transactions, reconciliation aging, receipt completeness, payroll handoff quality, and review-ready reporting.

Figure 1. Public estimates show the directional growth path for bookkeeping services and adjacent finance software categories.

Why the Workflow Still Needs Improvement

Workflow improvement matters because the official system often shows only the final record, not the work required to create it. In bookkeeping services, users may collect documents, answer status questions, verify payment details, chase approvals, or correct coding before the record is ready. That invisible labor is one reason a process can feel expensive even when software is already in place.

The deepest friction usually appears at handoff points. A receipt moves from an employee to a manager. An invoice moves from sales to finance. A bank transaction moves from the feed to the ledger. A timesheet moves from a consultant to a project manager. Every handoff can create delay if ownership, evidence, and status are unclear.

Weak workflow design also makes performance hard to measure. A manager may know that reporting is late, but not whether the delay came from missing documents, slow approval, unclear coding, poor integration, customer nonpayment, or manual reconciliation. Without that breakdown, improvement becomes guesswork and teams may buy tools that do not address the real constraint.

The main risks in this topic are misclassified transactions, missing receipts, unreconciled bank feeds, late payroll support, and tax-season cleanup work. These risks are not abstract. They affect cash planning, customer communication, supplier confidence, tax preparation, audit support, and the amount of time finance spends explaining what happened after the fact.

A better workflow turns status into an operating asset. Each item should show whether it is new, waiting for evidence, waiting for approval, disputed, ready for payment, paid, reconciled, or closed. Once status is visible, leaders can manage queues, aging, exceptions, and workload instead of relying on individual memory.

Why the Workflow Still Needs Improvement – practical statistics and checkpoints

-

The Cost of Invisible Labor: Mid-market finance and bookkeeping teams spend 40% to 50% of their close cycle time on tasks that are entirely manual, duplicated, or waiting on someone else to finish a handoff.

-

The Manual Baseline Checkpoint: A useful workflow baseline should map every manual handoff. On average, a single invoice or receipt requires 3 to 5 internal handoffs (from employee capture to manager approval to ledger entry), creating waiting periods that stall the month-end close.

-

The Most Common Risk Areas: Manual data entry and poor tracking generate heavy cleanup friction:

-

Misclassified Transactions & Errors: Up to 20% of manual entries contain transposition errors, misplaced decimals, or incorrect general ledger coding.

-

Missing Documentation: Bookkeepers waste an average of 6 hours per week chasing clients or internal managers for missing receipts and invoices.

-

Unreconciled Feeds: Organizations relying on manual matching experience a 90% higher rate of reconciliation discrepancies compared to those using automated transaction routing.

-

-

A Practical Process Map: A practical process map must eliminate visibility gaps. Without a clear owner and real-time status tracker, independent tasks spend up to 70% of their total cycle time sitting idle in email threads or pending queues before the next action is taken.

-

Reducing Status Questions: Implementing a centralized, status-driven workflow reduces repeated follow-up messages and internal update requests by up to 60%, as progress is visible at a glance without interrupting the finance team.

-

The Optimization Timeline: A proven, structured process improvement rhythm follows a 30-60-90 day framework:

-

Day 30: Establish baseline metrics and complete historical cleanup.

-

Day 60: Evaluate workflow adoption and iron out software integration friction.

-

Day 90: Secure a confirmed 35% to 50% reduction in overall processing time and solidify error reduction.

-

Automation and AI Are Changing the Operating Model

Automation changes bookkeeping services by moving routine decisions into predefined rules and connected systems. That can include capture, categorization, reminders, approval routing, exception queues, matching, or reporting. The value comes from removing repeated low-judgment work while keeping risk-based review where it belongs.

AI adds another layer by helping identify patterns that are difficult to manage manually. In this context, AI can suggest categories, highlight unusual items, summarize status, prioritize exceptions, or detect records that look inconsistent with past behavior. These capabilities are useful only when they support a clear process rather than creating another black box.

The best automation designs preserve accountability. A system may recommend a coding choice, flag a duplicate, or route a record to the right owner, but finance still needs thresholds, review rules, audit logs, and human judgment for high-risk items. That balance is especially important when money movement, customer balances, supplier records, or tax evidence is involved.

Automation also changes what the finance team does each day. Instead of spending time on repeated entry and status chasing, staff can focus on exceptions, policy questions, customer or supplier issues, data quality, and analysis. That shift is a major part of the ROI, even when headcount does not immediately decline.

For bookkeeping, the most mature operating model is not fully hands-off. It is a controlled workflow where routine items move quickly, unusual items are visible, and every important action is recorded. That is a better target than simply trying to automate every task without understanding which exceptions matter.

Automation & AI Are Changing the Operating Model – Practical Statistics and Checkpoints

- Eliminating the Routine Drag: Automating rule-based tasks across bank reconciliation, receipt capture, and sales categorization removes the bottleneck of individual inbox habits. Transitioning to automated transaction matching eliminates up to 80% of manual data entry tasks, allowing routine items to flow directly to the ledger without human intervention.

- AI as an Operational Co-Pilot: AI drives efficiency by processing unstructured data at scale. Organizations utilizing AI-driven categorization and anomaly detection see a 70% reduction in transaction processing times and catch duplicate or non-compliant expenses 4x faster than teams relying on end-of-month spot checks.

- The Necessity of Human-in-the-Loop Guardrails: High-risk financial decisions still demand structured human oversight. To prevent algorithmic errors in money movement and tax compliance, elite finance models route 100% of high-value transactions (typically those exceeding a defined $1,000 to $5,000 threshold) through automated exception queues for human sign-off, preserving strict audit trails and accountability.

- Shifting from Data Entry to Analysis: Automation alters daily accounting workflows without creating an opaque “black box.” By slashing manual follow-ups and data entry, bookkeeping teams reclaim up to 10 to 15 hours per week per employee. This time is redirected toward data quality analysis, strategic policy questions, and solving complex supplier or customer disputes.The 30-60-90 Day AI Operating Model Roadmap: Embedding intelligent automation successfully requires a tiered deployment timeline:

-

Day 30 (Baseline Cleanup): Map existing manual touchpoints and deploy OCR and bank-feed matching rules to instantly capture 60% of baseline volume.

-

Day 60 (Adoption Review): Fine-tune AI classification models and resolve routing friction to push automated, hands-off transaction processing past the 75% mark.

-

Day 90 (Process Improvement): Achieve a fully stabilized, exception-managed workflow, securing a 40% to 50% decrease in overall month-end close duration while maintaining zero visibility gaps.

-

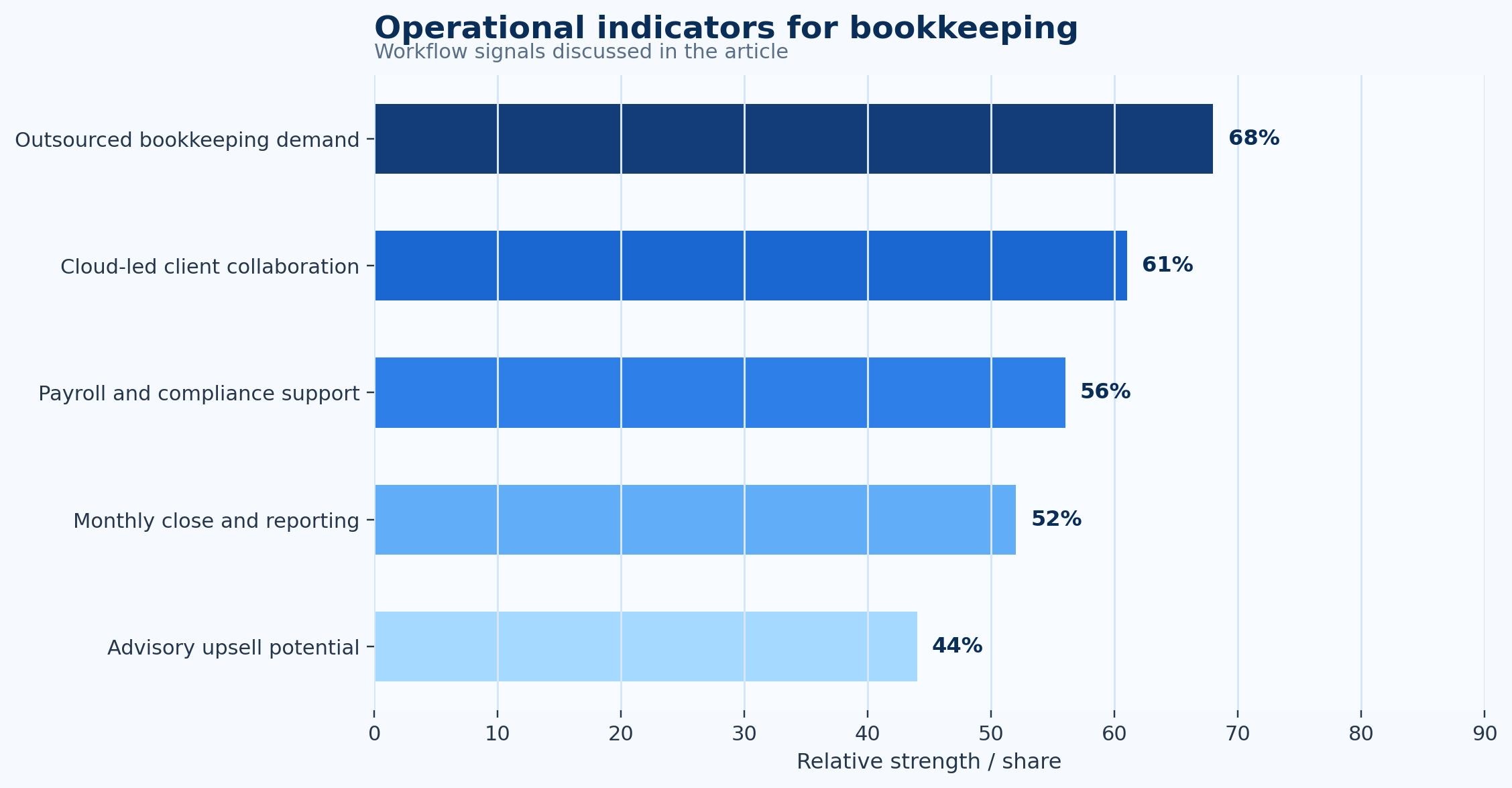

Figure 2. Operational indicators show why bookkeeping services adoption is tied to workload, visibility, and process quality.

Cash Flow, Billing, and Payment Impact

The financial impact of bookkeeping services is strongest when the process connects to cash timing. Records that are late, incomplete, or unclear can distort payment decisions, collection follow-up, credit planning, project margin, or supplier scheduling. A clean workflow improves the timing of information, not only the final accuracy of the accounting record.

Cash visibility depends on knowing what is expected, what is delayed, what is approved, and what still needs action. In many companies, these signals sit in different places: bank portals, accounting software, project tools, payment processors, email, and spreadsheets. Bookkeeping becomes more valuable when it brings those signals into a single management view.

Billing and payment issues often reveal workflow weaknesses before management reporting does. Unpaid invoices, delayed approvals, missing receipts, unbilled project work, or unreconciled bank transactions can all create misleading comfort. Revenue may look healthy while cash is late; expenses may look controlled while reimbursements are still waiting in employee inboxes.

The practical cash-flow question is whether the business can see enough early enough to act. If an invoice is overdue, a manager should know whether it was never sent, never opened, disputed, awaiting approval, or simply unpaid. If a cost is missing evidence, finance should know who owns the document and how long it has been outstanding.

The strongest finance teams measure both process and outcome. Process metrics explain why work is slow; cash metrics show whether the delay matters. Together, they help leaders decide whether to change policy, automate a step, improve customer communication, adjust payment timing, or add controls.

Cash Flow, Billing, & Payment Impact – Practical Statistics and Checkpoints

- The Cash Visibility Penalty: Bookkeeping timing directly impacts corporate liquidity. Organizations operating with fragmented data sources experience up to a 40% increase in forecast variance, as leaders make critical purchasing and working-capital decisions based on ledger positions that are often 15 to 30 days out of date.

- The Cost of Friction in Payment Planning: Late and incomplete records distort both sides of the balance sheet. In traditional bookkeeping workflows, 62% of corporate invoice disputes and collection delays stem from internal process bottlenecks—such as missing receipts, unbilled project milestones, or delayed manager approvals—rather than a customer’s inability to pay.

- Quantifying the Working Capital Drain: The true value of clear operational status is measured in cash cycle health. Companies utilizing manual matching and isolated billing spreadsheets suffer an average Days Sales Outstanding (DSO) that is 12 to 15 days higher than automated peers, locking up vital capital in uncollected revenue.

- The Exception and Error Burden: Billing and payment issues act as an early warning system for structural workflow failures. Manual invoice processing yields an average exception rate of 15% to 20% (due to missing purchase orders, misapplied tax codes, or duplicate entries), driving the manual processing cost to anywhere between $12 and $40 per invoice.

- The 30-60-90 Day Cash Impact Blueprint: Moving from backward-looking records to real-time cash visibility requires a structured optimization timeline:

-

Day 30 (Baseline Cleanup): Sync disconnected bank portals, payment processors, and expense feeds to reduce unclassified transaction queues by 50%.

-

Day 60 (Adoption Review): Implement rigid handoff rules and automated reminders to drop invoice approval cycle times by 30%, eliminating the systemic expense blind spots hidden in employee inboxes.

-

Day 90 (Process Improvement): Achieve an optimized Days Payable Outstanding (DPO) and secure a 20% to 30% acceleration in overall cash-conversion cycle speed, transforming the bookkeeping function from a compliance chore into an operating asset.

-

Small Business and Midmarket Implications

Small businesses often experience bookkeeping services as an owner-time problem before they experience it as a formal finance transformation. The owner may approve bills, chase payments, reconcile bank activity, answer accountant questions, and search for records. Even small improvements can matter because the same person often handles sales, operations, and finance decisions.

For small teams, the best system is usually the one that reduces daily interruption. A dashboard that shows unpaid invoices, missing receipts, upcoming bills, reconciliation status, or project billing readiness can save more time than a complex platform that requires heavy setup. Simplicity, clean reminders, and reliable records are often more valuable than broad feature lists.

Midmarket companies face a different problem. They usually have more users, more approvals, more customers or vendors, and more risk of process drift between teams. They need stronger permissions, integration, role clarity, and exception reporting. At that stage, the main benefit of bookkeeping is standardization as well as speed.

Enterprise teams add another layer of complexity: multi-entity reporting, audit requirements, approval thresholds, policy enforcement, and integration with ERP, banking, procurement, payroll, or project systems. Their business case may include risk reduction and control quality as much as productivity.

The implication is that benchmarks should not be copied blindly. A small business should not evaluate itself against a shared-services center, and an enterprise should not accept a lightweight workflow if it cannot support controls. The right maturity target depends on volume, complexity, staffing, and risk.

Small Business & Midmarket Implications – practical statistics and checkpoints

- Small businesses often value bookkeeping because it reduces owner follow-up and routine finance admin.

- Midmarket teams usually need stronger permissions, integrations, approval rules, and exception reporting.

- Enterprise teams focus more heavily on controls, auditability, multi-entity reporting, and policy enforcement.

- The right benchmark changes by volume, staffing model, transaction complexity, and risk exposure.

- A practical review rhythm is 30 days for baseline cleanup, 60 days for adoption review, and 90 days for confirmed process improvement.

Industry Differences and Use-Case Patterns

Industry differences matter because the same finance metric can mean different things depending on the operating model. Retail shops, contractors, restaurants, professional service firms, ecommerce sellers, and local service businesses may all use bookkeeping, but their records, approvals, evidence, and cash cycles can be very different. A project-based company may care about milestones and change orders; a retailer may care more about volume, deposits, and daily reconciliation.

The use cases also change by industry. For this topic, common use cases include bank reconciliation, expense categorization, receipt organization, monthly management reports. Each use case produces different data and different failure points. A missing receipt is not the same as an unpaid invoice, and an unbilled project milestone is not the same as an unreconciled bank transaction.

Industry-specific workflows should shape implementation priorities. A contractor may need job-level evidence and change-order discipline. An ecommerce seller may need bank-feed and payment processor reconciliation. A consulting firm may need time capture and billing readiness. A nonprofit may need fund or grant documentation.

Averages can hide those differences. A category may appear mature because large companies have adopted strong systems, while small firms in the same industry still rely on manual records. Another category may appear less automated because the workflow itself is more complex and requires more exception handling.

The most useful statistics break the workflow into segments: customer type, vendor type, department, location, project, payment method, aging bucket, transaction type, and exception reason. That level of detail helps leaders see where the process is truly strong and where the headline average is hiding work.

Industry Differences & Use-Case Patterns – practical statistics and checkpoints

- The most relevant industries include retail shops, contractors, restaurants, professional service firms, ecommerce sellers, and local service businesses.

- Industry workflows change the meaning of the same metric; a normal billing cycle in project work may be slow for retail transactions.

- Useful breakdowns include customer, vendor, project, department, location, service line, payment status, and aging bucket.

- A good comparison uses workflow similarity, not only industry labels.

- A practical review rhythm is 30 days for baseline cleanup, 60 days for adoption review, and 90 days for confirmed process improvement.

Controls, Compliance, and Audit Readiness

Controls are one of the main reasons bookkeeping services matters beyond productivity. A fast process is not enough if it cannot show who approved a transaction, what evidence supported it, whether policy was followed, and how exceptions were resolved. Finance teams need records that can stand up to review, not only records that move quickly.

Audit readiness depends on completeness. Documents, approvals, comments, payment status, reconciliation evidence, and changes to key data should be easy to retrieve. When evidence is scattered across inboxes and spreadsheets, audit work becomes a reconstruction exercise and finance staff lose time answering questions that a clean workflow should answer automatically.

Compliance needs vary by topic. Expense management may focus on policy limits and receipt evidence. Project billing may focus on client approval and contract terms. Business banking may focus on authorized users and account controls. Cloud accounting may focus on permissions, bank reconciliation, and tax records. The common requirement is a complete trail.

Automation can strengthen controls when rules are configured carefully. Approval thresholds, role-based access, duplicate checks, exception queues, and review logs reduce reliance on informal follow-up. Poorly configured automation, however, can move bad data faster, so control design should be part of implementation from the beginning.

The strongest control metric is not simply whether an item was processed. It is whether the organization can explain the item after the fact. If a manager, auditor, lender, tax preparer, or customer asks for the record, the system should show the evidence, approval, timing, and resolution without a long search.

Controls, Compliance, & Audit Readiness – practical statistics and checkpoints

- Control quality depends on evidence, role clarity, approval thresholds, audit trails, and exception ownership.

- Key risks include misclassified transactions, missing receipts, unreconciled bank feeds, late payroll support, and tax-season cleanup work.

- The strongest systems record who acted, when the action happened, what changed, and which evidence supported the decision.

- Audit readiness improves when records are complete before the auditor, tax preparer, lender, or manager asks for them.

- A practical review rhythm is 30 days for baseline cleanup, 60 days for adoption review, and 90 days for confirmed process improvement.

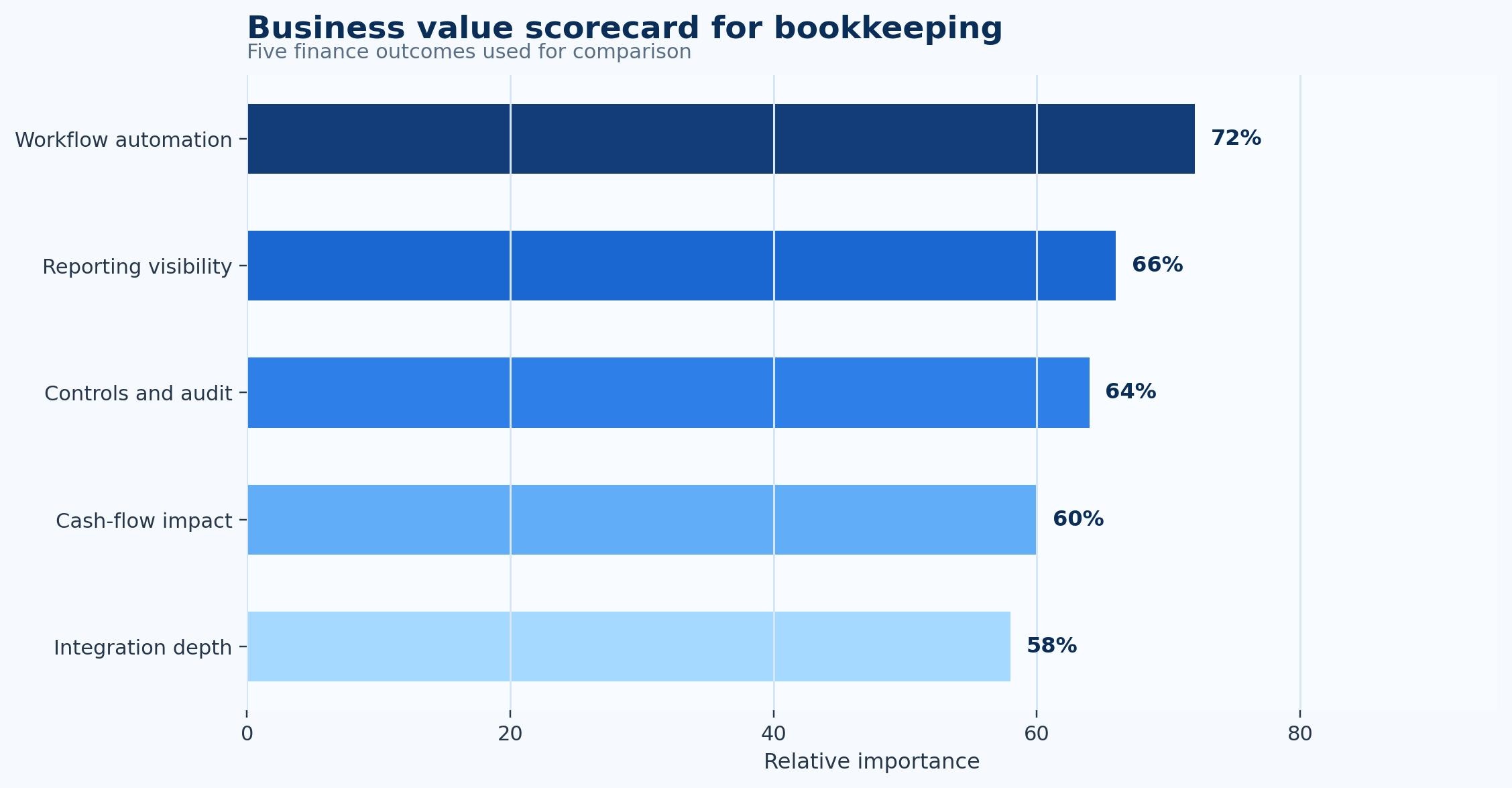

Figure 3. The value of bookkeeping services is spread across workflow automation, reporting, controls, cash-flow visibility, and integrations.

Implementation Barriers and Change Management

Implementation problems often come from process design, not technology alone. Teams may buy a tool while leaving old habits intact: invoices sent to personal inboxes, receipts stored on phones, approvals made in chat, and reports rebuilt in spreadsheets. The system then becomes another layer rather than a replacement for manual work.

Data quality is a major barrier. Supplier names, customer records, product codes, project references, employee details, and bank rules must be clean enough for automation to work. If the reference data is poor, the system will create exceptions that users must resolve manually, reducing confidence in the new process.

Change management is equally important. Users need to know why the workflow is changing, what the new status rules mean, when approval is required, and how exceptions should be handled. Without that clarity, employees may route work around the system because the informal path feels faster.

Integration also determines whether the project succeeds. Bookkeeping Services often needs to connect with accounting software, bank feeds, payment processors, payroll tools, project systems, customer records, document storage, or ERP modules. Weak integration can create duplicate work even when one part of the process improves.

A practical rollout starts with a narrow, high-impact workflow. The team should measure the baseline, clean the key data, define ownership, configure rules, train users, and review exceptions after launch. That approach builds confidence before expanding the system across more processes.

Implementation Barriers & Change Management – practical statistics and checkpoints

- A strong implementation starts with one workflow where bookkeeping creates measurable friction.

- The baseline should include volume, cycle time, backlog, error rate, exception reasons, and owner response time.

- Data cleanup is usually as important as software setup because poor master data creates avoidable exceptions.

- Training should explain which tasks are being automated and which judgment-based responsibilities remain human-led.

- A practical review rhythm is 30 days for baseline cleanup, 60 days for adoption review, and 90 days for confirmed process improvement.

A Practical Example of Better Workflow Design

Consider a growing contractor that has bank transactions in one system, receipts in employee phones, subcontractor payments in email, and tax questions arriving after the month is already closed. The company does not necessarily have a technology shortage. It has a status problem. People know their individual pieces of work, but no one has a reliable view of the full workflow, the missing evidence, the aging items, and the next action needed to move each record forward.

The first improvement is to map the workflow in plain language. What starts the process? Which record is created? Which evidence is required? Who approves it? What happens if information is missing? Which system becomes the source of truth? That map usually reveals repeated delays that were previously treated as isolated problems.

The second improvement is to define status categories. For bookkeeping, those categories may include received, incomplete, pending approval, disputed, ready to bill, paid, reconciled, closed, or exception review. The exact labels differ, but the principle is the same: every item should have a visible state and owner.

The third improvement is to connect reporting to daily work. A dashboard should not be a decorative summary. It should show the items that need attention, the reason they are delayed, the owner responsible, and the business impact. That connection turns data into workflow management.

The final improvement is to review the scorecard after implementation. If close timeliness, uncategorized transactions, reconciliation aging, receipt completeness, payroll handoff quality, and review-ready reporting improve, the workflow change is producing value. If the metrics do not improve, the team should look for the next constraint rather than assuming the software failed.

A Practical Example of Better Workflow Design – practical statistics and checkpoints

- A useful workflow baseline should list every manual handoff in bank reconciliation, receipt capture, payroll records, sales categorization, month-end review, and tax-ready file preparation.

- The most common risk areas are misclassified transactions, missing receipts, unreconciled bank feeds, late payroll support, and tax-season cleanup work.

- A practical process map should show who owns the item, what evidence is missing, the current status, and the next action.

- A strong bookkeeping workflow reduces repeated status questions because managers can see progress without asking finance to reconstruct it.

- A practical review rhythm is 30 days for baseline cleanup, 60 days for adoption review, and 90 days for confirmed process improvement.

Benchmarking and Scorecard Design

Benchmarking works best when it starts with the company’s own process. Public statistics provide context, but the real baseline comes from internal volume, aging, backlog, errors, exceptions, and cash impact. A company should know how many items enter the workflow, how long they wait, why they get stuck, and what happens when they are late.

A balanced scorecard for bookkeeping services should include speed, quality, control, cash, and capacity. Speed shows whether work is moving. Quality shows whether records are correct. Control shows whether approvals and evidence are complete. Cash shows whether the timing affects liquidity. Capacity shows whether the team can scale without proportional manual effort.

Scorecards should avoid vanity metrics. A high number of processed records can look positive while hiding a growing exception backlog. A low average cycle time can hide a few very old problem items. A large market forecast can look impressive while saying nothing about whether a company’s workflow is healthy.

The best benchmark is one that leads to an action. If exception aging rises, the team investigates owners and causes. If cash forecast variance widens, the team reviews payment timing and collection status. If receipt completeness falls, the team changes employee reminders or card controls.

For bookkeeping, the most valuable benchmark usually combines a headline KPI with a cause breakdown. A number such as approval cycle time becomes much more useful when it is split by department, amount, customer, project, vendor, or exception reason.

Benchmarking & Scorecard Design – practical statistics and checkpoints

- Core metrics for bookkeeping: close timeliness, uncategorized transactions, reconciliation aging, receipt completeness, payroll handoff quality, and review-ready reporting.

- Each metric should have an owner, a measurement period, a threshold, and an action when the number moves outside the target range.

- A useful scorecard separates volume, aging, quality, control, and cash impact.

- The best metric is one that changes a management decision, not one that only looks impressive in a dashboard.

- A practical review rhythm is 30 days for baseline cleanup, 60 days for adoption review, and 90 days for confirmed process improvement.

Metrics Leaders Should Track

Finance leaders should track a focused set of metrics rather than trying to measure everything. For this topic, the core measures include close timeliness, uncategorized transactions, reconciliation aging, receipt completeness, payroll handoff quality, and review-ready reporting. Those metrics show whether the process is becoming faster, cleaner, easier to manage, and more useful for decision-making.

Cycle-time metrics are important because they reveal delay. The relevant cycle might run from invoice issue to payment, receipt submission to reimbursement, time entry to client billing, bank transaction to reconciliation, or document capture to month-end close. The exact start and end points should match the workflow being improved.

Quality metrics show whether speed is reliable. A process that moves quickly but creates rework is not healthy. Leaders should monitor error rate, missing evidence, exception reason, duplicate records, incorrect coding, dispute rate, and reversal or adjustment activity.

Control metrics show whether the process is safe. Useful examples include approval completion, policy exception rate, audit evidence completeness, user permission review, segregation of duties, and overdue exception resolution. These metrics are especially important as automation increases.

Cash and management metrics show whether the workflow supports the business. Depending on the topic, those may include DSO, aging, forecast variance, reimbursement backlog, unbilled work, outstanding balances, supplier payment timing, or working-capital impact. The goal is to connect finance operations to decisions that managers make every week.

Metrics Leaders Should Track – practical statistics and checkpoints

- Core metrics for bookkeeping: close timeliness, uncategorized transactions, reconciliation aging, receipt completeness, payroll handoff quality, and review-ready reporting.

- Each metric should have an owner, a measurement period, a threshold, and an action when the number moves outside the target range.

- A useful scorecard separates volume, aging, quality, control, and cash impact.

- The best metric is one that changes a management decision, not one that only looks impressive in a dashboard.

- A practical review rhythm is 30 days for baseline cleanup, 60 days for adoption review, and 90 days for confirmed process improvement.

Data Quality and Integration Requirements

Data quality determines whether bookkeeping services becomes easier to manage or simply more digital. Automation depends on reliable customers, vendors, employees, projects, chart-of-account rules, payment references, and document evidence. If those inputs are incomplete, the system will create queues of exceptions that people still have to resolve manually.

Integration is the second requirement. Bookkeeping Services may touch accounting systems, bank feeds, payment processors, payroll tools, project systems, card programs, document storage, CRM records, or ERP modules. A tool that works well in isolation can still fail operationally if users must export and rekey information every week.

The practical test is whether the data moves with enough context. A transaction amount alone is not enough; finance teams often need customer or vendor identity, project code, approval owner, payment status, document evidence, tax treatment, and reconciliation status. Missing context creates delays even when the basic transaction has been captured.

A good implementation includes a cleanup phase. Teams should review duplicate customer or vendor names, old categories, inconsistent project codes, missing receipt rules, unresolved bank-feed matches, and open items that no longer have an owner. That work may feel less exciting than software configuration, but it is usually what determines whether automation is trusted.

Data governance should continue after launch. The team needs a regular review of exception reasons, fields that users override, integrations that fail, and records that require manual correction. Those patterns show where training, policy, or system rules need to improve.

Data Quality & Integration Requirements – practical statistics and checkpoints

- At least one owner should be assigned to master data, transaction status, evidence quality, and exception categories.

- A 30-day cleanup window can reveal recurring issues such as duplicate names, missing project codes, stale customer records, and unsupported transactions.

- Data quality should be measured before and after implementation so automation does not simply accelerate bad records.

- Integration should be judged by whether users stop exporting, rekeying, and reconciling the same data manually.

- A monthly data-quality review should track the top 5 exception reasons and the team or process owner responsible for each one.

ROI and Operating Economics

The return on bookkeeping services improvement should be measured through operating economics, not only subscription cost. A finance workflow consumes time when staff enter data, search for evidence, chase approvals, answer status questions, correct errors, reconcile differences, and explain variances during close. Those activities are real costs even when they do not appear on a separate invoice.

A useful ROI model starts with volume. How many transactions, invoices, receipts, payments, time entries, approvals, or records move through the workflow each month? Then it measures time per item, exception rate, rework rate, and downstream impact. A small time saving can become meaningful when volume is high and the work repeats every month.

The model should also include avoided cost. A company may not reduce headcount after improving bookkeeping, but it may avoid overtime, reduce temporary help, delay a hire, close faster, reduce audit preparation, or prevent cash leakage. These avoided costs are often more realistic than assuming immediate payroll savings.

Cash impact should be included when the workflow affects billing, collections, reimbursements, supplier payments, or bank visibility. Faster status can support better customer follow-up, fewer missed charges, more accurate payment timing, or earlier awareness of cash gaps. These benefits may matter more to management than the processing cost of any single transaction.

The strongest business case compares the old baseline with the new workflow over time. A 30-day comparison can show adoption problems, a 60-day comparison can show process stabilization, and a 90-day comparison can show whether behavior has actually changed. That timeline prevents teams from declaring success based only on go-live completion.

ROI & Operating Economics – practical statistics and checkpoints

- A practical ROI model should include at least 3 cost groups: labor time, error or rework cost, and cash-flow or control impact.

- A 10-minute reduction on 1,000 monthly transactions equals more than 166 hours of process capacity each month.

- Even a 1 percent improvement in collection timing, reimbursement leakage, missed billing, or avoidable rework can be material when transaction volume is high.

- ROI should compare baseline and post-launch metrics over 30, 60, and 90 days rather than relying on a one-time software business case.

- The most credible ROI evidence combines hard numbers with fewer escalations, cleaner close work, and less manual status chasing.

Future Outlook

The future of bookkeeping services is likely to be more connected and more predictive. Businesses will expect finance systems to show not only what happened, but what is waiting, what is late, what is risky, and what action should happen next. That shift turns reporting into operating guidance.

AI will play a larger role, especially in classification, anomaly detection, workflow summaries, reminder timing, and exception prioritization. The near-term value will be assistive rather than fully autonomous. Finance teams still need accountability, controls, and human review for decisions that affect cash, customers, suppliers, tax, or compliance.

Integration will also become more important. Bookkeeping Services cannot deliver its full value if it sits apart from payments, banking, accounting, customer records, project systems, document storage, or reporting. The next stage of maturity will connect these systems more naturally so teams do not rebuild the same picture manually.

For small businesses, the future will emphasize simpler tools that reduce admin without requiring finance transformation. For larger companies, the focus will be stronger controls, configurable workflows, analytics, and multi-entity visibility. Both paths point toward less manual reconstruction and more usable status data.

The companies that benefit most will be the ones that measure before they automate. They will know their baseline, choose the workflow with the highest practical impact, and use the technology to strengthen process discipline. That approach turns bookkeeping from a software purchase into a measurable operating improvement.

Future Outlook – Practical Statistics and Checkpoints

-

The Shift to Predictive Financial Guidance: Bookkeeping is rapidly transitioning from a backward-looking historical record to a forward-looking operational asset. Industry forecasts indicate that by 2028, over 75% of mid-market organizations will evaluate their bookkeeping functions based on predictive capabilities—such as real-time cash runway warnings and automated cash-flow risk modeling—rather than just the speed of the month-end close.

-

The Scale of AI Co-Pilot Assistance: While fully autonomous, hands-off finance departments remain a long-term concept, assistive AI will dominate the near-term landscape. Machine learning models are projected to handle up to 95% of routine data categorization and transactional anomaly triage, reducing human intervention to an oversight role focused purely on high-risk compliance, strategic tax planning, and edge-case exceptions.

-

The Cost of the “Integration Gap”: Modern bookkeeping cannot operate in an isolated silo. Siloed accounting tech stacks that fail to seamlessly connect payments, banking, CRM, and document storage drain significant resources, with businesses losing an average of $15,000 to $25,000 annually per employee entirely to manual data reconstruction, cross-platform reconciliation, and fixing broken API links.

-

The Small Business vs. Enterprise Divide: Future technology adoption paths will sharply diverge based on company scale:

-

For SMBs: The focus is on friction reduction, with 68% of small businesses prioritizing single-click administrative tools that require no technical configuration or formal finance transformation.

-

For Enterprises: The focus shifts to governance, where 84% of corporate finance leaders are prioritizing multi-entity visibility, granular role-based access controls, and highly configurable approval workflows.

-

-

The “Measure Before Automating” Advantage: Technology only accelerates existing processes; it does not fix structural flaws. Companies that systematically map their operational baselines, track error rates, and calculate labor hours before investing in new automation software achieve a 2.5x higher return on investment (ROI) and experience significantly smoother software adoption curves than peers who buy tools to fix ill-defined workflow problems.

Frequently Asked Questions

What is bookkeeping services?

Bookkeeping services refers to the tools, services, records, and workflows a business uses to manage bookkeeping services. In practice, it connects tasks such as bank reconciliation, receipt capture, payroll records, sales categorization, month-end review, and tax-ready file preparation so finance teams can reduce manual handling and make decisions with cleaner information.

Why do bookkeeping statistics vary by source?

The numbers vary because sources define the category differently. Some count only software revenue, while others include services, cloud subscriptions, implementation, adjacent payment tools, automation features, or industry-specific platforms. That is why the direction of growth and the operating benchmarks are usually more useful than a single market total.

Which bookkeeping metric matters most?

There is no single best metric for every company. A practical scorecard should include close timeliness, uncategorized transactions, reconciliation aging, receipt completeness, payroll handoff quality, and review-ready reporting. The most important metric is the one connected to the workflow constraint that creates the most delay, risk, or cash impact.

How can small businesses use these statistics?

Small businesses can use the statistics to compare their own workflow with broader patterns. They do not need enterprise complexity, but they do need clean status, reliable records, fewer missed steps, and less owner time spent on routine finance admin.

How should a company measure ROI from bookkeeping improvements?

ROI should begin with the current baseline: volume, time spent, backlog, exception rate, errors, rework, cash impact, and audit workload. The most credible ROI model uses the company’s own workflow data instead of relying only on generic industry averages.

What is the biggest implementation mistake?

The biggest mistake is buying a tool before defining the workflow. Teams should map the process, clean key data, assign ownership, define exceptions, and decide which outcomes they want to improve before configuring software or services.

How often should the scorecard be reviewed?

Operational metrics should be reviewed frequently enough to change behavior. Weekly reviews work well for aging, backlog, and exception queues, while monthly reviews are useful for trends, controls, close quality, and process improvement planning.

Where should a team start first?

The best starting point is the workflow with repeated follow-up or visible risk. For bookkeeping, that might be bank reconciliation, receipt capture, payroll records, sales categorization, month-end review, and tax-ready file preparation. A narrow start with clear metrics usually works better than trying to automate every process at once.

Final Takeaway

Bookkeeping Services Statistics shows a finance category where market demand and operating pressure are moving in the same direction. Public forecasts point to continued growth, but the more useful lesson is inside the workflow: businesses want fewer manual touches, cleaner records, faster status visibility, stronger controls, and better cash-flow confidence.

The best bookkeeping programs do not chase software for its own sake. They start with the process that slows finance down, measure the baseline, improve the workflow, and then use automation, services, or analytics to make the result repeatable. That is why the strongest statistics are not only market totals; they are the operating numbers that show whether finance work is becoming easier to manage, easier to audit, and easier to use in business decisions.