A research-backed statistics report on marketplace payout timing, seller cash flow, fees, reserves, refunds, chargebacks, cross-border settlement, embedded finance, and the metrics that decide whether marketplace growth turns into usable seller liquidity.

Marketplace seller payments are the financial layer that determines whether marketplace growth actually works for sellers. A platform can generate orders, traffic, and gross merchandise value, but sellers still need predictable payouts, clear fees, refund visibility, dispute evidence, currency support, and working-capital access. When payouts are slow or unclear, the issue becomes more than a finance problem. It affects inventory planning, seller trust, marketplace retention, and the seller’s ability to keep accepting demand.

That is why seller payment statistics should be read as operating signals rather than isolated platform facts. A seller does not experience marketplace scale as headline GMV. The seller experiences it as net proceeds after commissions, payment processing, advertising, fulfillment, refunds, reserves, chargebacks, currency conversion, tax withholding, and payout timing. The difference between gross sales and usable cash can decide whether a seller can restock inventory, pay suppliers, invest in ads, or continue selling on the platform.

The goal is to show which numbers help marketplace, payments, finance, risk, and seller-success teams understand where seller cash flow is strengthened, delayed, or weakened.

Executive Marketplace Seller Payment Benchmarks

These headline numbers show the scale of marketplace selling, the importance of independent sellers, the role of cross-border transactions, and the payment risks that sit behind every seller payout.

The numbers that define marketplace seller payments

• Amazon says more than 60% of sales in its store come from independent sellers, most of which are small and medium-sized businesses.

• Amazon reported that independent U.S. sellers averaged more than $375,000 in annual sales in 2025.

• Amazon says more than 75,000 independent sellers surpassed $1 million in annual sales, showing that marketplace payouts must support serious operating businesses, not only casual sellers.

• Reuters reported Walmart Marketplace had more than 100,000 sellers and more than 700 million items while marketplace sales grew 40% in a recent fourth quarter.

• Walmart partnered with JPMorgan to speed payments and cash-flow tools for online sellers, a signal that seller liquidity has become a competitive marketplace feature.

• eBay reported $74.7 billion in 2024 gross merchandise volume and $10.3 billion in full-year revenue.

• eBay said 49% of 2024 GMV was generated outside the United States, making currency, payout rail, and cross-border settlement important seller-payment issues.

• Etsy sellers generated $12.6 billion in 2024 gross merchandise sales across Etsy, Reverb, and Depop.

• The Etsy marketplace generated $10.9 billion in 2024 GMS, equal to 86.4% of total company GMS.

• Reverb represented 7.3% of Etsy Inc. GMS and Depop represented 6.3%, showing how multi-marketplace payment reporting must support different seller communities.

• Etsy’s marketplace revenue sources include transaction fees, payments processing, listing fees, and offsite advertising, which means seller payouts are affected by several deductions before cash is released.

• Seller-payment providers commonly describe standard marketplace payout waits of 10 to 30 days in some contexts, while accelerated payout products aim to shorten that cash-flow gap.

• Fraudulent chargebacks are a major seller-payment risk: Mastercard-sponsored research cited in business coverage estimated businesses could lose $15 billion to fraudulent chargebacks in 2025.

• Chargeback value was projected in the same coverage to rise from $33.79 billion to $41.69 billion by 2028.

• Juniper Research forecast online payment fraud losses above $362 billion globally across 2023 to 2028, making payment risk part of seller payout design.

• Worldpay reported digital payment value across ecommerce and in-person commerce grew from $1.7 trillion in 2014 to $18.7 trillion in 2024, showing why marketplace payouts sit inside a much larger payment transformation.

• Cross-border sellers face more than payout timing. They also face FX conversion, bank rails, local currency support, tax verification, and dispute evidence across regions.

• Embedded finance, instant payout, and working-capital products are expanding because sellers need cash before the standard payout cycle catches up with demand.

Executive readout The headline statistics point to one conclusion: seller payments are a trust system. Large marketplaces create demand, but sellers evaluate the platform through usable cash. A seller with strong gross sales can still experience weak cash flow if payout timing is slow, fees are unclear, reserves are unpredictable, or cross-border deductions are hard to reconcile.

Executive readout

The headline pattern is clear: marketplace payment performance should be judged by usable seller cash, not only by buyer order volume. Amazon, Walmart, eBay, and Etsy show enormous seller ecosystems, but every seller ultimately sees the marketplace through payout timing, fee deductions, refund exposure, reserve rules, tax holds, and dispute outcomes.

A stronger marketplace payment scorecard therefore separates gross platform scale from seller liquidity. A platform can report billions in GMV or GMS, but a seller needs to know how much of each order becomes net proceeds, when it arrives, which deductions were applied, and whether a dispute or return can change the balance later.

Why Seller Payments Are a Marketplace Trust System

A marketplace payment system does more than transfer money after a sale. It decides when sellers receive cash, what deductions are visible, which orders are held for refund or dispute risk, how currency is converted, and how the seller can reconcile the payout against orders, fees, taxes, and returns. That makes seller payments a practical measure of marketplace trust.

For sellers, trust is not created only by traffic or buyer demand. Trust is built when the seller can predict payout timing, understand fees, respond to disputes, and match every deposit to the original order. A platform can be large and still create frustration if sellers cannot explain why funds were delayed, why a fee was deducted, or why a refund reduced a later payout.

| Seller payment layer | What it controls | What can break |

|---|---|---|

| Payout timing | When sellers receive usable cash | Inventory and supplier-payment stress |

| Fee deduction | What the seller keeps after platform costs | Margin confusion and pricing mistakes |

| Refund reserve | Whether returned orders can be covered | Locked cash or negative seller balances |

| Chargeback handling | Who absorbs disputed payment risk | Seller losses and platform risk exposure |

| Cross-border payout | Currency, FX, bank rails, and settlement speed | Lower net proceeds or slower liquidity |

| Tax and compliance hold | Seller verification and reporting | Delayed or blocked payouts |

| Payment reporting | Reconciliation and bookkeeping evidence | Cash-flow blind spots |

Trust readout A seller payment system should answer four basic questions clearly: what sold, what was deducted, what is being held, and when the remaining cash will arrive. If any of those answers are unclear, payout speed alone will not create seller confidence.

Marketplace Scale: Sellers, GMV, GMS, and Platform Dependence

Marketplace scale matters because seller-payment systems must support very different seller models at the same time: high-volume retail sellers, small creative sellers, resellers, brands, exporters, local merchants, subscription businesses, and occasional sellers. A single payout rule can create very different cash-flow effects across those groups.

Major marketplace scale benchmarks

• Amazon’s independent sellers account for more than 60% of sales in the Amazon store.

• Independent U.S. sellers on Amazon averaged more than $375,000 in annual sales in 2025.

• Amazon reported 75,000+ independent sellers above $1 million in annual sales, making payout predictability important for inventory-heavy businesses.

• Walmart Marketplace had 100,000+ sellers in the Reuters seller-payments coverage.

• Walmart Marketplace also had 700 million+ listed items, which increases the importance of automated seller reporting and payout reconciliation.

• Walmart marketplace sales grew 40% in a recent Q4 period, showing rapid scaling pressure on seller operations.

• eBay produced $74.7 billion in 2024 GMV, giving seller-payment flows large global scale even without Amazon-sized order volume.

• eBay revenue reached $10.3 billion in 2024, showing that seller activity supports a multi-billion-dollar marketplace business model.

• eBay’s international GMV share of 49% means nearly half of marketplace volume involved sellers or buyers outside the U.S. revenue center.

• Etsy Inc. generated $12.6 billion in 2024 GMS across its marketplace portfolio.

• The core Etsy marketplace generated $10.9 billion of that GMS.

• Etsy marketplace GMS represented 86.4% of company GMS, while Reverb and Depop represented 7.3% and 6.3%.

• Etsy’s filing describes revenue from marketplace transaction fees, payments processing, listing fees, and advertising, meaning seller cash flow is shaped by several platform monetization layers.

• Large marketplaces often process payouts for sellers who vary widely in category, country, risk, return rate, and shipping proof quality.

• Seller payout systems therefore need rules for both high-volume professional merchants and smaller sellers who may rely on the marketplace as their main business channel.

Scale readout Marketplace scale is a payment problem because every sale has to be transformed into a seller-facing cash record. GMV is not enough. Marketplaces need payout logic, fee transparency, refund handling, dispute records, tax treatment, FX support, and seller reporting that can scale with seller volume.

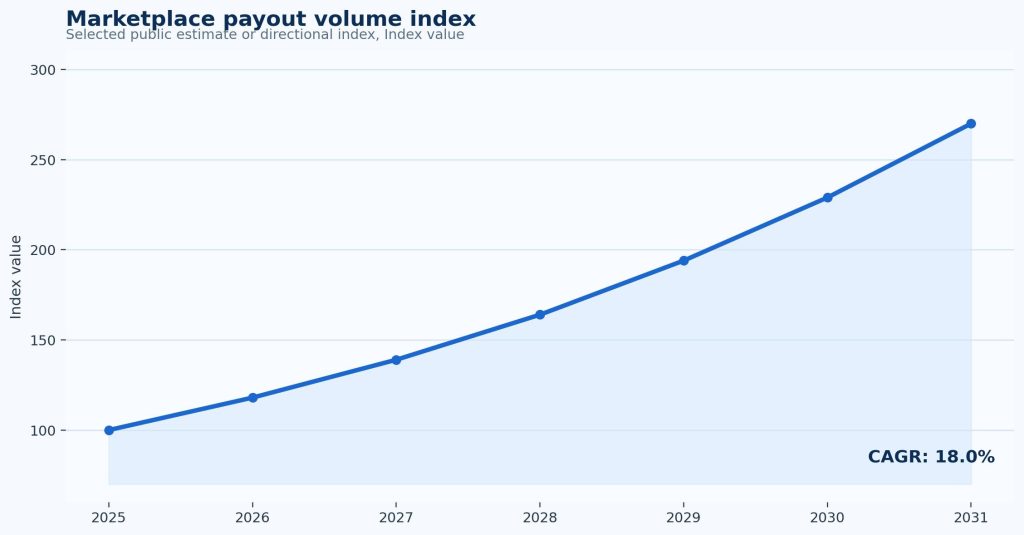

Figure 1. Marketplace seller payments should be read against GMV, seller scale, payout timing, and net proceeds because sellers experience platform growth through cash flow, not headline transaction volume.

Scale interpretation for seller-payment teams

• A marketplace where more than 60% of sales come from independent sellers needs payout controls that work for professional sellers, not only casual storefronts.

• An average seller-sales benchmark above $375,000 suggests that payout delays can affect inventory buying, supplier payment, payroll timing, and advertising budgets.

• A seller crossing $1 million in annual sales is managing an average run rate above $83,000 per month before fees, refunds, advertising, inventory, and tax are considered.

• If 49% of a marketplace’s GMV is international, nearly half of the platform’s seller-payment logic may need to support currency, banking, compliance, or cross-border reporting questions.

• A marketplace portfolio where one core marketplace contributes 86.4% of GMS still needs payment reporting that can explain smaller specialist marketplaces with different seller behavior.

The important operating lesson is that seller-payment design must scale in two directions. It must support large seller volume, but it must also support different seller types. A global reseller, an Etsy craft seller, an eBay cross-border merchant, and a Walmart retail supplier do not experience payout risk in the same way.

Seller Payout Timing and Cash-Flow Pressure

Payout timing is one of the clearest ways sellers experience marketplace quality. A seller may receive an order today, ship tomorrow, and still wait days or weeks before the cash becomes usable. That gap affects inventory purchases, ad spend, supplier payments, payroll, and the seller’s ability to respond to demand spikes.

Payout timing and cash-flow benchmarks

• Seller-payment providers commonly describe standard marketplace payout waits of 10 to 30 days in some contexts.

• A 10-day payout delay on $30,000 in monthly sales can leave roughly $10,000 of gross monthly sales waiting at any one time before fees, refunds, or reserves.

• A 30-day delay can keep nearly a full month of sales outside the seller’s usable cash balance.

• A seller with $100,000 in monthly gross sales and a 15-day average payout delay can have about $50,000 in sales value waiting before payout.

• If that seller’s net payout after fees is 82%, the delayed usable cash is still about $41,000.

• A seller carrying 30% cost of goods sold may need replacement inventory funding before the marketplace payout arrives.

• Same-day payout products reduce the cash-flow gap most for sellers with fast inventory cycles or supplier payment deadlines.

• Accelerated payout fees should be evaluated against the seller’s margin, because faster cash can still reduce profit if the transfer cost is high.

• New sellers often face more conservative payout timing because platforms need fraud, delivery, and buyer-satisfaction evidence before releasing funds.

• High-return categories may experience longer effective payout exposure because refund risk can extend beyond the original payout date.

• Weekend, holiday, and bank-processing schedules can create practical delays even when the marketplace payout cycle is technically short.

• Cross-border seller payouts can add extra settlement time when intermediary banks, local receiving accounts, or currency conversion steps are involved.

• A seller paid every 14 days receives about 26 payout events per year; a seller paid weekly receives about 52.

• A seller moving from a 14-day to a 2-day payout model receives cash roughly 12 days faster per cycle.

• For seasonal sellers, payout timing matters most during inventory build periods, when demand rises before supplier bills are fully paid.

| Payout delay issue | Seller impact | Metric to track |

|---|---|---|

| 10-30 day payout wait | Inventory restocking slows | Average days to payout |

| Reserve hold | Cash tied up after sale | Reserve balance as % of sales |

| Refund window | Cash may be withheld for return risk | Refund exposure by category |

| Cross-border bank delay | Settlement takes longer | Country-level payout time |

| New-seller hold | Early growth becomes harder | Hold duration and release rate |

| Dispute hold | Cash locked during investigation | Dispute resolution time |

Payout readout The best payout metric is not just fastest possible transfer. Marketplaces should separate trusted-seller payout speed, new-seller hold logic, refund reserve rules, dispute holds, and cross-border settlement. Sellers need speed, but they also need predictable reasons when speed is limited.

Seller Liquidity Scenarios and Inventory Planning

Payout timing becomes more meaningful when it is translated into inventory and working-capital scenarios. A seller can be profitable on paper and still run short of cash if payout timing does not match restocking cycles, supplier payment dates, advertising spend, and refund exposure.

Cash-flow scenarios sellers should model

• At $25,000 in monthly marketplace sales, a 10-day payout delay can leave roughly $8,300 of gross sales waiting before the seller sees usable cash.

• At the same sales volume, a 30-day delay can keep nearly $25,000 outside the seller’s operating balance before fees and refunds are considered.

• At $75,000 in monthly sales, a 15-day payout delay can place about $37,500 of gross order value in a waiting state.

• If marketplace deductions equal 15% of gross sales, a seller with $75,000 in monthly GMV may receive about $63,750 before advertising, inventory, freight, and tax effects.

• If reserves hold another 10% of sales during a risk window, the same seller could see $7,500 temporarily unavailable even after the sale is complete.

• If refund exposure reaches 8% of monthly sales, a $75,000 seller may need to plan for $6,000 in potential refund deductions before treating the payout as fully spendable.

• A seller that restocks every 14 days needs a different payout strategy than a seller that restocks every 60 days because the cash-conversion cycle is shorter.

• An advertising-heavy seller may spend cash before payout arrives, which means payout timing and ad efficiency should be reviewed together.

The practical point is not that every seller needs instant payout. The point is that payout timing should match the seller’s operating cycle. Inventory-heavy sellers, seasonal sellers, and high-growth sellers often need faster or more predictable cash than low-volume sellers with long restocking windows.

Fees, Take Rate, and Net Seller Proceeds

Seller payment quality depends on net proceeds, not gross order value. A seller may see strong sales in the marketplace dashboard while the bank deposit is much lower after commissions, payment processing, advertising, fulfillment, storage, refunds, taxes, and currency conversion. A mature seller payment report shows the full bridge from gross sale to usable cash.

Fee and net-proceeds benchmarks

• Etsy’s marketplace revenue categories include transaction fees, payments processing, listing fees, and offsite advertising, showing that multiple deductions can affect seller proceeds.

• eBay’s $10.3 billion in 2024 revenue against $74.7 billion in GMV illustrates how platform revenue is connected to seller transaction volume.

• A seller with a $100 order and a 15% commission keeps $85 before processing, ads, shipping, refund risk, and taxes.

• If payment processing adds 3%, the same $100 order falls to $82 before other costs.

• If advertising costs equal 10% of the order value, net proceeds before fulfillment fall to about $72.

• If the seller also pays $12 for fulfillment or shipping support, the usable amount becomes $60 before inventory cost.

• A 5% currency conversion or FX spread on a cross-border payout reduces an $82 net payout by about $4.10.

• A seller earning 20% product margin can lose a quarter of profit if fees rise by 5 percentage points without a price increase.

• A marketplace fee that looks small per order can become material at volume: $1 of extra fees across 50,000 annual orders equals $50,000.

• Listing fees matter most for sellers with low sell-through because the cost is incurred before the sale is guaranteed.

• Advertising fees matter most when sellers depend on marketplace visibility to maintain order volume.

• Fulfillment and storage fees matter most for bulky, seasonal, or slow-moving inventory.

• Refund fees matter most in categories where return rates are structurally high.

• Chargeback fees matter most when disputes are frequent or evidence quality is weak.

• Effective take rate should include commission, payment processing, required services, advertising dependency, refunds, FX, and dispute costs rather than only the published referral fee.

| Fee type | Where it appears | Why it matters |

|---|---|---|

| Commission/referral fee | Deducted from sale | Reduces gross margin |

| Payment processing fee | Card, wallet, or marketplace payment handling | Changes net payout |

| Listing fee | Charged per listing or before sale | Affects low-volume sellers |

| Advertising fee | Paid for visibility inside marketplace | Can reduce profitable growth |

| Fulfillment/storage fee | Logistics and inventory services | Affects category economics |

| Currency conversion | Cross-border payout | Reduces foreign seller proceeds |

| Chargeback fee | Dispute or fraud case | Adds risk cost |

Net proceeds readout The seller payment dashboard should not stop at payout amount. It should explain how gross order value became net proceeds. Without that bridge, sellers cannot price correctly, choose advertising budgets, evaluate fulfillment options, or compare one marketplace with another.

Net-proceeds controls marketplace teams should not hide

• A seller’s gross sale, platform commission, processing fee, advertising deduction, tax collection, refund adjustment, reserve hold, and final payout should be traceable to the same order record.

• A 5% fee misclassification on $40,000 in monthly sales can create $2,000 of confusion between seller accounting and platform payout reporting.

• A 2 percentage-point change in effective take rate on $100,000 of monthly sales changes seller net proceeds by $2,000 before inventory and advertising costs.

• A seller with 500 monthly orders needs fee reporting by order, not only by weekly deposit, because blended payout totals make margin analysis difficult.

• If advertising deductions are mixed with platform fees, sellers may understate customer-acquisition cost and overstate product margin.

• If currency conversion is reported only at payout level, cross-border sellers may struggle to match order-level revenue to bank-level deposits.

Fee transparency is therefore a trust feature. Sellers usually accept that marketplaces need commissions, payment processing, fulfillment, and advertising economics. What weakens trust is when the seller cannot explain the gap between the order total and the deposit amount.

Refunds, Reserves, Holds, and Marketplace Risk Controls

Marketplaces have to protect buyers and platforms from fraud, refunds, and chargebacks that may appear after a seller has already received cash. Reserves and holds are therefore part of seller-payment design. The issue is not whether reserves exist; it is whether they are transparent, proportional, and tied to a clear release path.

Reserve, refund, and hold benchmarks

• A 10% rolling reserve on $100,000 in monthly sales locks $10,000 of gross sales until release.

• A 20% reserve locks $20,000 on the same monthly volume, which can materially affect inventory purchases.

• If a seller’s net payout rate is 80%, a 10% reserve on gross sales can represent 12.5% of the seller’s expected net cash.

• A seller with 15% return exposure should not be evaluated the same way as a seller with 3% return exposure.

• New sellers may face payout holds until platforms see delivery confirmation, buyer satisfaction, or chargeback patterns.

• High-ticket categories can require tighter holds because one dispute can exceed the value of many ordinary orders.

• Cross-border sellers may face longer holds when tax, identity, customs, or local banking verification is incomplete.

• Return-window timing matters because a marketplace may be exposed to refunds after the initial seller payout.

• Negative seller balances can appear when refunds or chargebacks exceed the seller’s current payable amount.

• A hold without a release date creates more seller frustration than a hold with a clear reason and measurable release condition.

• Reserve release time should be tracked in days, not just as an outstanding balance.

• Refund deduction reports should connect each refund to the original order, original payout, fee reversal, and return reason.

• Marketplaces should separate fraud-related holds from routine refund reserves because sellers need different actions to resolve them.

• High seller-support ticket volume around holds is a signal that the payment policy is not being communicated clearly.

• A reserve system that protects the platform but blocks healthy sellers from restocking can damage marketplace supply over time.

Reserve readout Reserves are not automatically bad. They protect buyers and marketplaces when refunds, fraud, or chargebacks appear after payout. The problem is poor transparency. Sellers need to know why funds are held, how much is held, what evidence can release them, and when the money will become available.

Figure 2. Seller payout timing and reserve exposure should be evaluated together because faster payouts can still leave sellers cash-constrained if reserves, refunds, or disputes hold too much value.

Chargebacks, Fraud, and Dispute Evidence

Chargebacks and disputes are where seller payments become risk management. A marketplace has to protect buyers, but sellers also need a fair process that recognizes shipping proof, product evidence, buyer communication, and return behavior. When dispute evidence is weak, the payout system becomes vulnerable to refund abuse and friendly fraud.

Fraud and dispute benchmarks

• Mastercard-sponsored research cited in business coverage estimated $15 billion in fraudulent chargeback losses for businesses in 2025.

• Chargeback value was projected to rise from $33.79 billion to $41.69 billion by 2028 in the same cited coverage.

• Juniper Research forecast online payment fraud losses above $362 billion globally from 2023 through 2028.

• Juniper also forecast $91 billion in online payment fraud losses in 2028 alone.

• A seller with a 1% chargeback rate on 10,000 annual orders faces 100 disputed orders before considering refunds or ordinary returns.

• If the average order value is $75, those 100 chargebacks represent $7,500 of disputed merchandise value before fees and labor.

• A dispute that takes 30 days to resolve can delay seller cash longer than the original payout cycle.

• Item-not-received disputes require tracking, delivery confirmation, and sometimes carrier evidence.

• Item-not-as-described disputes require product photos, listing details, buyer messages, and return-condition evidence.

• Unauthorized payment disputes require payment-risk evidence that may sit with the marketplace or payment processor, not only the seller.

• Refund abuse patterns are easier to detect when the marketplace connects buyer history, item category, return reason, and seller evidence.

• Digital goods and services create harder dispute evidence because delivery may be access-based rather than shipment-based.

• Cross-border disputes can take longer when language, customs, shipping, and local buyer-protection expectations differ.

• Seller dispute win rate should be tracked by category, region, and evidence type rather than as one blended percentage.

• A low seller win rate may show weak seller behavior, but it may also reveal weak marketplace evidence collection.

| Dispute type | Evidence sellers need | Payment risk |

|---|---|---|

| Item not received | Tracking and delivery confirmation | Refund or chargeback loss |

| Item not as described | Photos, listing copy, buyer messages | Forced refund or return |

| Unauthorized payment | Fraud signals and processor evidence | Chargeback and fees |

| Refund abuse | Order history and return pattern | Margin loss |

| Cross-border dispute | Shipping proof and customs record | Delayed resolution |

| Digital product dispute | Access logs and delivery evidence | Harder proof burden |

Dispute readout A marketplace dispute process is only as strong as its evidence chain. Seller payouts should not be reversed without clear order, shipping, communication, and refund records. At the same time, platforms need enough fraud control to protect buyers and maintain payment-network trust.

Dispute evidence and seller-protection benchmarks

• A seller dispute process should separate item-not-received claims, item-not-as-described claims, unauthorized-payment claims, return abuse, and refund-delay complaints because each requires different evidence.

• A chargeback rate that looks small at 0.5% can still create 50 disputes for a seller processing 10,000 orders.

• At $80 average order value, those 50 disputed orders represent $4,000 in gross sales before fees, shipping, labor, and chargeback costs.

• If 20% of disputes lack shipment or delivery evidence, the seller-protection problem may be documentation quality rather than fraud screening alone.

• If dispute resolution takes 30 days, cash is not only at risk; it is unavailable for one full monthly inventory cycle for many sellers.

• A seller win rate should be reviewed by dispute reason, category, carrier, country, and evidence type, not only as one blended percentage.

The payment system becomes more credible when sellers know which evidence protects them. Tracking numbers, delivery confirmation, buyer messages, listing details, serial numbers, photos, return inspection notes, and customs records all help turn payment disputes from guesswork into reviewable cases.

Cross-Border Seller Payments and FX

Cross-border seller payments are not simply international transfers. Sellers need to know which currency they will receive, what exchange rate applies, how long settlement takes, whether local bank rails are available, and whether tax or identity checks can hold funds. A seller can make sales globally and still lose margin if payout infrastructure is weak.

Cross-border payout and currency benchmarks

• eBay said 49% of 2024 GMV was generated outside the United States, making cross-border seller payment design central to its marketplace model.

• A seller receiving $10,000 in foreign-currency sales loses $200 if FX and conversion costs total 2%.

• The same seller loses $500 if FX and conversion costs reach 5%.

• A 3-day extra settlement delay on cross-border payouts can matter for sellers buying inventory weekly.

• A seller with monthly international gross sales of $50,000 and a 4% FX cost gives up $2,000 before other fees.

• Local receiving accounts can reduce friction when sellers need to accept marketplace sales in one currency and pay suppliers in another.

• Currency conversion should be shown by order or payout batch because blended exchange rates make reconciliation difficult.

• Cross-border tax verification can hold payouts even when the buyer payment has already cleared.

• International sellers may need VAT, GST, withholding, or marketplace facilitator reporting details to reconcile net payouts.

• Bank account validation failures create failed payouts even when the seller has completed orders successfully.

• Cross-border dispute resolution can lock cash longer when shipping evidence or customs tracking is incomplete.

• Seller support should track failed payout rates by country and bank rail, not only total failed payouts.

• Platforms operating in multiple regions need payout calendars that account for local bank holidays and settlement days.

• Currency volatility can change seller margin between order date and payout date when conversion timing is unclear.

• Cross-border sellers need payout reporting that separates platform fee, payment processing, FX conversion, tax withholding, refund, and final deposit.

Cross-border readout Cross-border seller payments require localization on the payout side, not only on the buyer checkout side. Payment teams should measure country-level payout time, FX cost, failed payout rate, tax hold rate, and dispute resolution time because these are the numbers sellers feel after the sale.

Cross-border payout scenarios that change seller margin

• A 1% FX spread on $50,000 in monthly cross-border payouts costs $500 before bank fees, platform fees, or payment-processing deductions.

• A 2.5% FX spread on the same payout volume costs $1,250, enough to change whether low-margin inventory remains profitable.

• A seller receiving payouts in the wrong currency may face two conversions: one at the marketplace or payment provider and another at the seller’s bank.

• If international GMV represents 49% of a marketplace’s volume, currency and settlement quality are not edge cases; they are core marketplace payment infrastructure.

• Cross-border sellers need payout reports that show source currency, conversion rate, converted amount, date, fees, and receiving account.

• Local receiving accounts can reduce friction, but they also require compliance checks, tax records, and bank-account ownership validation.

Cross-border payment quality should be judged by net proceeds after currency conversion, not only by whether the seller eventually receives funds. The seller needs to understand the route from buyer payment to marketplace balance to local payout.

Embedded Finance, Same-Day Payouts, and Seller Working Capital

Embedded finance is expanding because marketplace sellers often need cash before the standard payout cycle finishes. Faster payout, seller wallets, working-capital advances, inventory finance, and marketplace banking can help sellers restock faster, but they also introduce fees, dependency, and repayment pressure.

Seller liquidity and embedded finance benchmarks

• Walmart’s partnership with JPMorgan to speed seller payments shows that seller cash flow has become a platform-level competitive issue.

• Storfund and Mangopay positioned same-day seller payouts as a way to reduce standard marketplace waits that can run 10 to 30 days.

• A seller turning inventory every 14 days may need payout speed closer to the inventory cycle to keep growth from stalling.

• A seller with $200,000 in monthly gross marketplace sales and a 14-day payout delay can have roughly $93,000 of gross sales waiting before payout.

• If that seller’s fee and refund deductions total 18%, the delayed net proceeds are still about $76,000.

• An instant payout fee of 1% on $50,000 of accelerated payouts costs $500.

• If faster cash lets the seller restock $20,000 of profitable inventory sooner, the fee may be worthwhile; if not, it becomes margin leakage.

• Working-capital advances should be evaluated against sales volatility because repayment often depends on future marketplace proceeds.

• Seller wallets can keep money inside the platform ecosystem and reduce transfer delays, but they may increase platform dependence.

• Local receiving accounts can help exporters reduce FX friction when sales and supplier costs use different currencies.

• Inventory financing is most useful when sellers have repeatable sell-through data and predictable payout history.

• Faster payouts should be segmented by risk level; mature sellers with strong delivery and low dispute rates may justify faster release than new high-risk sellers.

• Embedded finance should be measured by seller retention, inventory availability, payout complaints, fee cost, and default risk, not only adoption.

• Seller liquidity products can improve supply depth if they help sellers keep inventory in stock during demand spikes.

• Overuse of advances can weaken sellers if repayment absorbs too much future payout cash.

| Embedded finance tool | Seller benefit | Risk to monitor |

|---|---|---|

| Same-day payout | Faster restocking | Fees may reduce margin |

| Payout advance | Inventory funding | Repayment pressure |

| Seller wallet | Faster platform-native money movement | Platform dependence |

| Marketplace loan | Growth capital | Debt tied to sales volatility |

| Local receiving account | Better cross-border payout | FX and compliance complexity |

| Instant transfer | Faster cash availability | Transfer fees |

Liquidity readout Faster payout is most valuable when it solves a real operating constraint: inventory, supplier payment, advertising cash, or working capital. Marketplace teams should avoid treating instant payout as a cosmetic feature. The useful question is whether faster cash improves seller health after fees and risk controls are included.

Embedded finance readout

• Same-day payout is most valuable when the seller has repeatable demand, fast inventory turnover, and enough margin to justify any faster-transfer cost.

• A payout advance can help a seller buy inventory before the next payout cycle, but repayment should be modeled against refund risk and seasonal demand.

• A seller with 20% gross margin has much less room for payout-advance fees than a seller with 50% gross margin.

• If a seller’s ads, fulfillment fees, and marketplace commission already consume 25% of revenue, additional financing costs can turn growth into cash-flow pressure.

• Embedded finance should therefore be tied to order history, refund rate, dispute rate, payout reliability, and inventory velocity rather than offered only as a generic loan feature.

The best marketplace finance products help sellers close a timing gap, not hide weak unit economics. Faster cash is valuable when it supports profitable restocking. It is risky when it simply accelerates spending into categories with high refunds, high fees, or unstable demand.

Regional Marketplace Seller Payment Intelligence

Seller-payment design varies by region because marketplaces, bank rails, tax rules, payment habits, and cross-border trade patterns differ sharply. A seller in the United States may prioritize payout speed and chargeback evidence. A European seller may need VAT reporting and local currency clarity. An exporter in Asia-Pacific may focus on FX, local receiving accounts, and platform wallet flows. A Latin American seller may care about instant payment rails and settlement trust.

Regional seller-payment signals

• North America is central to Amazon, Walmart, eBay, and Etsy seller-payment scale because these platforms have large U.S. seller and buyer bases.

• Amazon independent U.S. sellers averaged more than $375,000 in annual sales in 2025, making seller payouts a material cash-flow issue for many U.S. merchants.

• Walmart Marketplace had 100,000+ sellers and 700 million+ items in the Reuters coverage, which gives U.S. seller payment systems large catalog and payout complexity.

• eBay’s 49% international GMV share shows that mature marketplaces cannot treat seller payments as one-country bank transfers.

• Europe and the UK require marketplace payment systems to support VAT, consumer protection, cross-border settlement, and local reporting expectations.

• European sellers often need payout reports that separate marketplace fees, VAT treatment, refunds, and advertising deductions.

• Asia-Pacific marketplace exporters often manage sales in one currency, supplier costs in another, and payouts through local banking or payment partners.

• China and APAC marketplace ecosystems often combine commerce, wallets, logistics, and seller services more tightly than simple payout systems.

• India’s marketplace seller base is tied to small-business digitization, UPI-era payment behavior, and faster movement toward digital settlement rails.

• Latin American marketplaces must account for local payment methods, installment culture, FX, and seller trust in payout reliability.

• Brazil’s Pix-driven payment environment shows why local instant rails can change buyer payment behavior and seller cash expectations.

• Mexico and other Latin American markets require seller payment programs that consider local bank coverage, tax records, and cross-border platform participation.

• Cross-border sellers need region-level payout metrics because the same platform can feel fast in one country and slow in another.

• Country-level payout failure rates can expose weak bank onboarding, identity verification gaps, or local transfer limitations.

• Regional seller support tickets should be categorized by payout delay, bank failure, currency conversion, tax hold, reserve hold, and dispute deduction.

| Region | Seller payment priority |

|---|---|

| North America | Payout speed, fee clarity, chargebacks, seller financing |

| Europe / UK | VAT, cross-border settlement, local currency, compliance |

| China / APAC | Platform wallets, export sellers, mobile commerce ecosystems |

| India | Small-seller digitization and instant-payment infrastructure |

| Latin America | Local payouts, installments, FX, marketplace trust |

| Cross-border sellers | Currency, bank rails, tax, payout timing |

Regional readout Regional payout intelligence should be operational, not decorative. Marketplaces should compare payout speed, failed payout rate, FX cost, dispute hold duration, seller-support tickets, and tax-hold frequency by country because those are the differences sellers feel most directly.

Figure 3. Regional seller payment strategy should combine marketplace scale, cross-border exposure, payout timing, FX friction, and local payment infrastructure rather than relying on one global payout policy.

Seller Payment Data Quality and Reconciliation

Seller-payment trust depends heavily on data quality. A deposit in a seller’s bank account is not enough if the seller cannot connect it back to orders, refunds, fees, taxes, reserves, advertising, chargebacks, and currency conversion. Poor payout reporting turns bookkeeping into detective work.

Reconciliation and payment data benchmarks

• A seller with 1,000 monthly orders needs payout reporting that can connect every order to fee, tax, refund, reserve, and payout status.

• If 2% of those orders have unclear deductions, the seller has 20 reconciliation issues per month.

• If each issue takes 10 minutes to investigate, that creates more than 3 hours of monthly admin work.

• At 10,000 monthly orders, the same 2% issue rate creates 200 monthly reconciliation exceptions.

• A gross/net payout mismatch should show commission, payment processing, advertising, shipping, tax, reserve, refund, FX, and final deposit separately.

• Refund-to-order matching helps sellers distinguish ordinary returns from errors or repeated refund abuse.

• Fee classification accuracy matters because advertising, fulfillment, listing, processing, and commission costs affect different management decisions.

• Reserve release timing should appear in payout reports so sellers can forecast when held cash becomes usable.

• Chargeback reports should show dispute reason, evidence deadline, amount, fee, and outcome.

• FX reports should show source currency, payout currency, exchange rate, conversion fee, and settlement date.

• Advertising deductions should be connected to campaign or order attribution where possible.

• Seller support teams should track payout-confusion tickets as a data-quality signal, not just a service burden.

• Failed payout events should be tracked by seller country, bank account issue, verification issue, and platform processing issue.

• A complete seller payment record should let a seller reconcile bank deposits without exporting multiple disconnected reports.

• Strong seller-payment data reduces tax-time friction because sellers can separate sales, fees, refunds, taxes, and net cash more easily.

| Reconciliation issue | What sellers need to see |

|---|---|

| Gross/net mismatch | Sale, fee, refund, tax, reserve, payout breakdown |

| Refund mismatch | Original order, refund date, refunded amount |

| Fee confusion | Fee category, rate, order ID |

| Reserve hold | Hold reason, amount, release date |

| FX difference | Source currency, exchange rate, payout currency |

| Chargeback | Dispute reason, evidence, outcome |

| Advertising deduction | Campaign or order attribution |

Data quality readout Seller payment data quality is a retention issue. Sellers are more likely to trust the marketplace when deductions are understandable, reserves are traceable, and deposits can be reconciled without manual reconstruction. Better reporting does not only help accounting; it reduces seller frustration.

How Seller Payment Risks Change by Business Model

Marketplace sellers do not all experience payouts the same way. A reseller with thin margins, a handmade seller with long production time, a cross-border exporter, and a high-volume brand have different cash-flow risks.

Business-model payment patterns

• High-volume retail sellers usually care most about payout speed, inventory restocking, advertising deductions, and chargeback evidence.

• Handmade and custom sellers often care about production deposits, cancellation timing, buyer messages, and dispute proof.

• Cross-border exporters care about FX, settlement time, local receiving accounts, customs evidence, and tax reporting.

• Brand sellers often care about advertising spend, fulfillment fees, marketplace commissions, and channel-level margin.

• Low-volume sellers are more sensitive to listing fees, payout thresholds, and bank transfer minimums.

• New sellers are more likely to face verification and hold rules, so payout transparency matters during onboarding.

• High-return categories need better reserve logic because refunds can arrive after payout.

• High-ticket sellers need stronger dispute evidence because one claim can lock a large amount of cash.

• Digital product sellers need access-log and delivery evidence because shipping proof does not exist.

• International sellers may need payout reporting that supports multiple tax systems and currencies.

• Sellers using marketplace advertising should track net payout after ad spend, not only sales growth.

• Sellers using embedded finance should track repayment share of future payout to avoid cash-flow compression.

Business-model readout The strongest seller-payment programs segment policy by seller model, risk, and maturity. A blanket payout rule may be easy to administer, but it can over-hold trusted sellers, under-protect high-risk categories, or confuse cross-border sellers with unclear deductions.

Payout Policy Maturity and Seller Segmentation

A strong marketplace payment program usually does not use one payout policy for every seller. Seller age, category, delivery evidence, refund history, dispute rate, bank verification, country, and order value all change payout risk. Segmentation allows marketplaces to release cash faster for trusted sellers while keeping enough control for high-risk accounts.

Seller segmentation and payout-policy benchmarks

• A seller active for 24 months with a low dispute rate should not be risk-scored the same way as a seller active for 24 days.

• A new seller hold period can be useful during the first 30 to 90 days, but it should have clear release criteria based on delivery, refunds, and account verification.

• A seller with a 0.3% chargeback rate has a different payout profile from a seller with a 3.0% chargeback rate.

• A seller shipping 1,000 orders per month with reliable tracking data gives the platform more evidence than a seller shipping 20 high-value orders without consistent proof.

• A high-ticket seller with $500 average order value can create more reserve exposure from 10 disputes than a low-ticket seller creates from 100 smaller disputes.

• A category with 20% return exposure may justify different reserve logic from a category with 3% return exposure.

• Sellers with verified bank accounts, tax records, and delivery integrations should move through payout holds faster than sellers with incomplete records.

• A platform can segment sellers by tenure, GMV, refund rate, dispute rate, fulfillment method, verification status, and country risk.

• If 5% of sellers generate 50% of payment-support tickets, payment friction is concentrated and should be solved by segment, not averaged across the platform.

• If 10% of seller payouts fail because of bank-account or verification issues, onboarding quality is a payment-performance problem, not only a seller-support problem.

• A seller with $1 million in annual marketplace sales may need account-management level payout transparency because small delays affect large working-capital decisions.

• Independent sellers above $1 million in annual sales, such as the 75,000+ Amazon benchmark, are closer to operating businesses than casual sellers.

• Payout segmentation should also consider fulfillment method because platform-fulfilled orders often create stronger delivery and return evidence than self-fulfilled orders.

• Policy maturity improves when the platform can explain exactly why one seller receives accelerated payouts while another remains under reserve.

• A mature program tracks seller upgrade rates: how many sellers move from new-seller hold to standard payout, then from standard payout to faster payout.

Segmentation readout Seller segmentation helps marketplaces avoid two mistakes: over-holding trustworthy sellers and under-protecting high-risk accounts. The best policy is not universally fast or universally conservative. It is evidence-based, transparent, and adjustable as the seller builds a stronger record.

Tax Reporting, Compliance, and Verification Holds

Seller payments also depend on compliance. Marketplaces may need seller identity, tax details, legal entity records, bank ownership, address verification, VAT or GST information, and country-specific reporting before funds can move normally. These controls protect the marketplace, but they can also become payout friction when sellers do not understand what is missing.

Compliance and verification benchmarks

• A missing tax form can block payout even when the seller has shipped orders and the buyer has paid.

• A seller with $50,000 waiting in payable balance but incomplete verification experiences the hold as a cash-flow crisis, not an administrative step.

• Bank account mismatch should be treated as a high-risk event because a payout can be redirected to the wrong party.

• Identity verification should be measured by completion time, failure rate, resubmission rate, and seller-support ticket volume.

• If 15% of new sellers fail first-pass verification, payout onboarding should be improved before order volume scales.

• A marketplace operating across 10 countries may need different tax, banking, and reporting fields for each region.

• European seller payouts often require VAT-aware reporting, while U.S. sellers may focus on marketplace tax forms and bank deposit reconciliation.

• Cross-border sellers may need both marketplace-level tax reports and local bank statements to reconcile income in their home country.

• A seller with multi-currency payouts needs transaction date, conversion date, exchange rate, fee, and payout date for clean records.

• Compliance holds should have reason codes such as missing tax ID, bank mismatch, identity review, sanctions screening, document expiration, or suspicious activity.

• A hold that lacks a reason code creates avoidable support volume because the seller cannot fix the problem independently.

• Payout systems should track how many holds are seller-caused, platform-caused, bank-caused, or regulator/compliance-caused.

• If 30% of payout tickets relate to verification, the marketplace has a seller onboarding problem, not only a payments problem.

• Compliance controls are stronger when they are triggered before the seller reaches a large unpaid balance.

• Clear verification prompts can reduce the risk that sellers discover missing documents only after a payout is due.

Compliance readout Compliance holds are necessary, but they should not feel mysterious. Sellers need clear requirements, reason codes, and release paths. The best compliance design prevents payout surprises by collecting identity, tax, bank, and entity records before the seller has a large balance waiting.

Seller Support, Trust Signals, and Payment Service Levels

Seller-payment problems often appear first in support tickets. A marketplace may think its payout system is working because total payout volume is high, while sellers are still struggling with unclear fees, missing deposits, failed transfers, reserve holds, or refund deductions. Support data is therefore a payment benchmark.

Support and service-level benchmarks

• A payout support ticket rate of 2% across 100,000 monthly seller payouts still creates 2,000 payment-related contacts.

• If each support contact takes 12 minutes, those 2,000 tickets consume about 400 hours of support capacity.

• A failed payout rate of 1% across 50,000 monthly payout events creates 500 seller cash-flow interruptions.

• If the average failed payout is $800, those failures represent $400,000 of seller cash temporarily blocked.

• A reserve explanation that prevents even 10% of support tickets can save meaningful support capacity at large marketplace scale.

• Payment support should separate missing payout, delayed payout, unclear fee, reserve hold, refund deduction, chargeback, failed bank transfer, and FX complaint categories.

• A seller who contacts support 3 times about the same payout issue is experiencing a process failure, not only a single ticket.

• Resolution time should be tracked in hours for failed bank transfers and in days for disputes, reserves, and compliance holds.

• Payment service-level agreements should define how quickly sellers receive a reason for a hold, not only when the money is released.

• Payout status pages reduce support volume when they show pending, processing, failed, held, reserved, refunded, disputed, and paid statuses clearly.

• Seller trust improves when payout communication uses order IDs, amount, deduction reason, and expected date instead of generic status labels.

• High payout complaint rates after a policy change show that communication failed even if the policy itself is financially reasonable.

• A seller with 52 weekly payout cycles per year has many more opportunities to notice small mismatches than a seller paid monthly.

• Large sellers may reconcile daily, while small sellers may reconcile only at tax time; reports need to support both behaviors.

• Seller-success teams should treat payout complaints as retention signals because payment uncertainty can cause sellers to move inventory to another marketplace.

Support readout Seller support data turns payout pain into measurable operational evidence. If sellers repeatedly ask where the money is, why fees changed, or when reserves release, the payment system may need better reporting, clearer policy labels, or faster issue resolution.

Marketplace Payment Program Maturity

The strongest marketplace payment systems mature in layers. They start by paying sellers reliably, then add clearer fee reporting, reserve transparency, faster payout options, cross-border payout support, embedded finance, and automated reconciliation. The maturity path matters because paying faster without better data can simply move confusion and risk earlier in the cycle.

Payment maturity indicators

• Level 1 programs focus on basic payout execution: did the seller receive money after the marketplace sale?

• Level 2 programs add fee visibility: can the seller explain each deduction from gross sale to net payout?

• Level 3 programs add reserve and refund transparency: can the seller see what is held, why, and when it releases?

• Level 4 programs add cross-border localization: can sellers receive local currency payouts with clear FX and tax reporting?

• Level 5 programs add embedded finance: can trustworthy sellers access faster payouts, working capital, and seller wallet tools responsibly?

• A marketplace that cannot connect order, fee, refund, reserve, dispute, tax, FX, and payout data is still immature even if deposits arrive on time.

• Maturity should be measured by seller-visible outcomes such as fewer payout tickets, faster failed-payout correction, lower unresolved deduction rates, and higher reconciliation confidence.

• A useful payout maturity target is fewer manual investigations per 1,000 payouts, not only higher payout volume.

• Faster payout adoption should be tracked alongside fee cost, seller retention, inventory availability, and default or fraud outcomes.

• Reserve transparency should be measured by release predictability and seller understanding, not only by balance size.

• Cross-border maturity should be measured by payout time, FX cost, local-bank success, tax hold frequency, and seller complaint rate by country.

• Dispute maturity should be measured by evidence completeness, seller response time, win rate, resolution time, and repeat dispute patterns.

• Fee maturity should be measured by whether sellers can classify deductions into platform, payment, advertising, fulfillment, tax, refund, chargeback, and FX buckets.

• Payment reporting maturity should reduce the need for sellers to combine marketplace CSVs, bank statements, ad dashboards, and accounting exports manually.

• The best marketplaces turn seller payment data into a seller-health signal, because cash-flow stress often appears before seller churn becomes visible.

Maturity readout Marketplace payment maturity is not one feature. It is the ability to release cash predictably, explain deductions, manage risk fairly, support cross-border sellers, and give sellers records they can use without rebuilding the payout story themselves.

Leadership Decision Checkpoints for Seller Payments

A mature seller-payment review should end with a few decisions that leadership can actually make. More dashboards are not enough if no one decides which seller segments should receive faster payout, which fee labels need clarification, which reserve rules need better explanation, and which cross-border corridors are creating unnecessary cost.

Decision checkpoints

• Which seller segments create the lowest payment risk and should qualify for faster payout options?

• Which categories have the highest refund or dispute exposure and need clearer reserve rules?

• Which fee categories generate the most seller support tickets or reconciliation mismatches?

• Which countries show the longest payout times, highest FX cost, or most failed bank transfers?

• Which seller groups are using payout advances because of healthy growth, and which are using them because standard payout timing is too slow?

• Which dispute reasons have the lowest seller win rate, and is the problem fraud, evidence quality, shipping data, or policy design?

• Which compliance holds are preventable through better onboarding, tax data, bank verification, or seller education?

Marketplace payment teams should not only know the benchmark; they should know which operating decision the benchmark supports.

Marketplace Seller Payment Diagnostic Table

A useful seller-payment benchmark should show where the payment system is helping or hurting seller operations. The diagnostic model below connects seller payment problems to the metrics that reveal them.

| Problem area | Core signals to measure | Useful benchmark angle |

|---|---|---|

| Payout speed | Average days to payout, instant payout usage | Seller cash-flow gap |

| Fee clarity | Net proceeds and fee category visibility | Effective take rate |

| Reserves and holds | Held balance and release timing | Refund and dispute risk |

| Disputes | Chargeback rate and seller win rate | Fraud and chargeback exposure |

| Cross-border payout | FX cost and settlement time | International seller mix |

| Seller liquidity | Inventory restocking delay and advance usage | Working-capital need |

| Reconciliation | Payout mismatches and unresolved adjustments | Seller trust |

| Seller support | Payout tickets and payment complaints | Operational friction |

Every metric should answer a seller-payment question: are sellers paid fast enough, are fees understandable, are holds justified, are disputes fair, are cross-border payouts clean, and can sellers reconcile the cash they receive?

90-Day Seller Payment Benchmark Plan

Marketplace payment statistics become useful when they are converted into an operating plan. A practical seller-payment review can be run in a 90-day cycle rather than a vague payout modernization project.

| Timing | What to do | Output |

|---|---|---|

| Days 1-30 | Baseline payout timing, fee deductions, reserves, refunds, dispute holds, FX costs, failed payouts, and seller support tickets. | Seller payment performance map |

| Days 31-60 | Fix high-confidence issues: unclear fee labels, slow payout batches, missing reserve reasons, refund mismatch, payout-report gaps, and failed bank-account onboarding. | Controlled seller-payment improvements |

| Days 61-90 | Review seller complaints, payout speed, reserve release, dispute outcomes, cross-border settlement, and adoption of faster payout options. | Repeatable seller-payment scorecard |

Planning principle The goal is not simply to pay every seller faster in every case. The goal is to pay trustworthy sellers predictably, explain holds clearly, protect buyers and platforms from risk, and give sellers enough payment detail to manage cash flow.

Metrics Marketplace Teams Should Track

A seller-payment dashboard should focus on the metrics that truly impact sellers, including payment speed, transparency, risk management, customer support, and cross-border transaction performance, rather than measuring success only by total payout volume. Using organized financial tools such as a cash receipt template can also help marketplace teams maintain accurate payment records, improve tracking, and create a smoother experience for both sellers and buyers.

| Metric | Why it matters |

|---|---|

| Average days to payout | Shows seller cash-flow speed |

| Same-day or instant payout adoption | Shows demand for faster liquidity |

| Net proceeds per order | Shows seller take-home after fees |

| Effective take rate | Captures commission, processing, ads, and other deductions |

| Reserve balance as % of sales | Shows how much seller cash is held |

| Reserve release time | Shows transparency and liquidity |

| Refund deduction rate | Shows return exposure |

| Chargeback rate | Measures dispute and fraud pressure |

| Seller dispute win rate | Shows fairness and evidence quality |

| Failed payout rate | Captures bank or account issues |

| Cross-border payout time | Shows international settlement quality |

| FX cost per payout | Shows global seller margin impact |

| Payout support ticket rate | Shows seller confusion or payment friction |

| Seller churn after payout issue | Measures trust impact |

Scorecard readout The best seller-payment scorecard links financial operations to seller outcomes. A faster payout program is not successful if fees are unclear. A reserve program is not successful if healthy sellers cannot restock. A cross-border payout rail is not successful if FX, failed transfer, or tax-hold issues make seller cash unpredictable.

Marketplace Seller Payments FAQ

Common questions

• What are marketplace seller payments?

Marketplace seller payments are the payout, fee, refund, reserve, tax, dispute, and reporting systems that move buyer payments from a marketplace to sellers after orders are processed.

• Why do marketplace payout times matter?

Payout times matter because sellers use cash to buy inventory, pay suppliers, fund advertising, cover shipping, and keep operations running. A 10-30 day payout wait can create a material cash-flow gap for growing sellers.

• How do marketplace fees affect seller payouts?

Marketplace fees reduce gross sales into net proceeds. Sellers may see deductions for commission, payment processing, listing, advertising, fulfillment, refunds, FX, taxes, and chargebacks.

• Why do marketplaces hold seller funds?

Marketplaces hold funds to manage refund, fraud, chargeback, tax, verification, and new-seller risk. Holds are easier for sellers to accept when the reason, amount, and release date are clear.

• How do chargebacks affect marketplace sellers?

Chargebacks can reverse revenue, add fees, lock payout cash, and require evidence such as tracking, delivery proof, product details, and buyer messages. They are especially painful when sellers have already shipped inventory.

• What makes cross-border seller payments complex?

Cross-border payouts add currency conversion, local bank rails, tax verification, settlement timing, customs evidence, and international dispute handling to the normal marketplace payout process.

• How do same-day payouts help sellers?

Same-day payouts can help sellers restock faster, pay suppliers sooner, and keep advertising running. The benefit should be measured after transfer fees and risk controls, not only by speed.

• What seller payment metrics should marketplaces track?

Useful metrics include average days to payout, net proceeds per order, effective take rate, reserve balance, chargeback rate, failed payout rate, FX cost, payout support tickets, and seller churn after payment issues.

Final Takeaway

Marketplace seller payments are where platform growth becomes seller liquidity. GMV, item count, and seller signups are important, but sellers ultimately manage the marketplace through net proceeds: what was sold, what was deducted, what was held, what was refunded, what was disputed, what currency was converted, and when the cash became available.

The statistics show why this topic deserves a full scorecard. Large marketplaces depend on independent sellers, global seller activity, cross-border transactions, refund management, chargeback controls, and increasingly sophisticated seller-finance products. A payment system that cannot explain payout timing, fees, reserves, FX, and disputes will eventually weaken seller trust even if buyer demand remains strong.

The best marketplace payment programs are not simply the fastest. They are predictable, transparent, risk-aware, and localized. They release funds quickly when seller history and order risk support it, explain holds when buyer protection requires caution, show every deduction clearly, and give sellers the reporting needed to reconcile cash without rebuilding order history manually.

For marketplace leaders, the practical goal is a payment system that supports growth without hiding risk: faster payout options for low-risk sellers, clear reserve logic, stronger dispute evidence, cleaner fee reporting, better FX visibility, and metrics that separate gross marketplace scale from usable seller cash.