Invoice financing lets companies borrow against unpaid invoices without necessarily selling the receivable outright. It sits between everyday collections management and broader working-capital finance. For many small and mid-sized firms, the product is attractive because it links available funding to actual customer invoices rather than only to collateral or historic profitability. The statistics around invoice financing are useful because they separate market enthusiasm from operating reality. A category can grow quickly in revenue while many companies are still managing the underlying work through spreadsheets, email, manual approvals, and fragmented systems. The gap between market forecasts and day-to-day maturity is where the most useful business insight usually sits.

This report looks at invoice financing through a practical finance and operations lens. Market-size estimates show how much capital, vendor activity, and customer demand are moving into the category. Adoption metrics show whether teams are changing their real workflows. Operating benchmarks show whether the tools are improving speed, accuracy, visibility, compliance, and cash outcomes rather than simply adding another software layer.

The numbers should be read with care because publishers define these markets differently. Some estimates include only software revenue. Others include services, implementation, transaction volume, platform fees, financing balances, or related workflow categories. That is why directional movement, segment differences, and operational interpretation matter more than treating any single dollar estimate as final. The strongest use of these statistics is to understand what businesses are actually trying to fix and which measurements prove progress.

Headline Statistics and Benchmarks

The operational reality of invoice financing is defined by macro-market projections, systemic funding gaps, and granular workflow performance. When evaluating these numbers, the focus shifts away from software hype toward the measurable trends shaping corporate liquidity.

Here are the critical statistics and operational benchmarks that outline the current state of invoice financing:

Global Market Size & Institutional Projections

-

The $5.9 Trillion Horizon: The global invoice factoring market is projected to reach an estimated valuation of $5,955.38 billion by 2030, expanding at a compound annual growth rate (CAGR) of 11.4 percent.

-

The $3.4 Trillion Market Baseline: Market research from Strategic Market Research pinned the global invoice factoring market’s immediate aggregate footprints at $3.4 trillion.

-

The $5.2 Trillion Intermediate Target: Projections from the same group indicate that the global factoring market will climb to $5.2 trillion by 2030, reflecting accelerating enterprise adoption of flexible funding vehicles.

-

Traditional Market Footprint: Beyond software revenue and transaction fees alone, the “traditional” global invoice trading ecosystem commands a massive structural baseline valued at roughly $3 trillion USD (Boutemine, n.d.).

-

Alternative Financing Catalysts: Analysis from Grand View Research shows that the strong expansion of factoring services is overwhelmingly propelled by intense demand for alternative financing instruments among small and medium-sized enterprises (SMEs) looking to bypass rigid traditional banking restrictions.

-

Bank Credit Integration: Highlighting its prevalence in corporate finance, invoice discounting products alone make up approximately 10 percent of all credit extended by banking institutions worldwide, serving as an essential pillar of global working capital (Esteva et al., 2023).

Core Operational Metrics & Performance Benchmarks

-

Maximum Liquidity Advances: Under highly optimized invoice discounting structures, funding providers frequently advance up to 90 percent of the underlying invoice value immediately upon verification (Boutemine, n.d.).

-

Standard Upfront Advance Floors: Across mainstream private commercial finance platforms, initial funding programs typically provide an upfront cash injection ranging between a 70 percent and 80 percent advance rate of total receivables at agreement inception (Irungu, n.d.).

-

Target Payment Backlog Windows: Operational data indicates that invoice discounting delivers the highest balance-sheet efficiency when targeting late payments trapped in a 1 to 3-month (30 to 90 days) collection cycle (Esteva et al., 2023).

-

Residual Capital Flow Settlement: The remaining 10 percent to 30 percent reserve balance of the receivable is held by the provider and transferred back to the supplier (minus interest and administrative facility fees) only after the debtor settles the invoice in full (Boutemine, n.d.; Irungu, n.d.).

-

Funding Speed and Velocity: The true dividing line between mature financial setups and legacy setups is funding speed. Transitioning from fragmented manual oversight (spreadsheets and emails) to connected digital workflows compresses verification, risk checks, and capital deployment from several weeks down to hours.

-

Eligible Invoice Share Optimization: High-performing teams continuously track the percentage of total corporate receivables that qualify for automated funding, looking to maximize this ratio to establish a highly predictable source of day-to-day capital.

-

Approval Rate Stability: Maintaining high approval rates requires tightly integrated credit risk models. Systems that automatically cross-reference historical payer behavior can approve transactions smoothly without expanding the platform’s overall risk exposure.

Macroeconomic Pressures & The SME Funding Gap

-

Global SME Scale: Small and medium enterprises act as the foundational anchor of the market, representing 90 percent of all businesses and accounting for more than 50 percent of total employment worldwide (Sharma et al., 2023).

-

GDP Contribution Benchmarks: These resource-constrained firms generate nearly 50 percent of the total world GDP, meaning systemic payment backlogs and cash flow bottlenecks carry macroeconomic consequences (Sharma et al., 2023).

-

US Domestic Job Footprint: Within advanced economic ecosystems like the United States, small firms account for roughly half of all private-sector jobs and nearly 44 percent of the country’s gross domestic product (Sharma et al., 2023).

-

The Overdue Invoice Penalty: When denied streamlined invoice financing, small firms experiencing cash flow shocks from overdue invoices turn to costly stop-gaps; under these pressures, monthly small business credit card repayments have spiked up to three times higher than traditional loan payments (Akcigit, n.d.).

-

Receivables as Collateral: Because a vast majority of small business owners and small farmers lack the real estate or fixed assets required to clear traditional commercial loan parameters, invoice factoring provides an essential lifeline by treating the invoice itself as the underlying collateral (Geurs, 2020).

-

Credit Card Supply Contractions: Recent market tightening demonstrates that when banks reduce credit availability, small businesses suffer an immediate 15.75% drop in credit card balances, which triggers an associated 10% decline in revenue growth (Akcigit, n.d.).

-

The Employment Growth Multiplier: Securing reliable working capital yield tangible operational growth; firms that maintain consistent access to receivable or working capital finance exhibit long-term employment growth rates 1 to 3 percentage points larger than unfinanced competitors (Esteva et al., 2023).

High-Value Use Cases & Sector-Specific Applications

-

Workflow Clustering: The highest-value use cases heavily concentrate around distinct, repeatable structures—namely invoice discounting, selective invoice finance, and confidential invoice finance—where high transaction volumes justify the cost of automation.

-

The Power of Confidentiality: A major benchmark driving the choice of invoice discounting over standard factoring is customer exposure; under modern discounting frameworks, the end buyer (debtor) remains completely unaware that the invoice has been financed, protecting critical B2B relationship dynamics (Esteva et al., 2023).

-

Target Sector Capital Efficiency: Asset-heavy and long-cycle fields like B2B services, manufacturing, wholesale distribution, and transportation experience the most rapid drops in Days Sales Outstanding (DSO) when moving away from fragmented invoicing systems.

-

Connected Workflow Migration: The modern category benchmark is moving away from basic digitization toward fully connected operating systems. True efficiency is proven when data ingestion, compliance verification, automated risk profiling, and instant performance reporting live on a single, unified architecture.

How to Read These Statistics Correctly

The first step in reading invoice financing statistics is separating market revenue from workflow performance. Market revenue shows how much businesses and platforms are spending. Workflow performance shows whether users are saving time, reducing errors, accelerating cash, or improving compliance. A market can be growing because vendors are selling more seats or processing more transactions even if the average buyer is still early in operational maturity.

A second distinction is between adoption and maturity. A company may count as an adopter after adding a digital intake form, connecting an API, or deploying a basic workflow. That does not mean the process is fully automated, governed, or optimized. Mature adoption usually means the team has clear rules, good data quality, exception handling, audit trails, and management metrics that are reviewed regularly.

A third distinction is between volume and value. Higher volumes are helpful for proving that a system is being used, but value comes from the quality of outcomes. A workflow that handles thousands of transactions but still requires manual correction may be less valuable than a smaller workflow with high accuracy and strong controls. The best statistics combine volume, cycle time, cost, accuracy, and risk indicators.

Market Size and Growth Outlook

The global market for invoice financing is experiencing a structural shift, moving from a fragmented collection of manual workflows to unified, tech-enabled operating systems. This growth is driven by a fundamental change in buyer behavior: corporate finance and operations teams are no longer just looking for modern software dashboards. They are investing heavily to solve concrete operational problems, targeting faster cash deployment, higher approval rates, reduced manual errors, and more predictable working capital.

When a financing platform directly links accounting systems, payment rails, risk checks, and supplier data, it evolves from a basic productivity tool into a critical mechanism for financial control. For mid-sized firms, cloud-based delivery models eliminate the need for costly enterprise implementations, while for large organizations, these automated solutions eliminate compliance and control gaps at scale.

To evaluate this space accurately, the market must be split into two layers: the specialized digital software platforms driving automation, and the massive underlying global financed volume being traded across industries.

Market and Adoption Statistics to Know

Global Market Scale & Future Projections

-

The $5.9 Trillion Benchmark: The global invoice factoring market is projected to expand to an estimated $5,955.38 billion by 2030, sustained by an 11.4% compound annual growth rate (CAGR).

-

The Baseline Footprint: Alternative estimates valued the global invoice factoring market at $3.4 trillion in 2024, on track to hit $5.2 trillion by 2030.

-

Financed Volume Expansion: Expanded industry projections indicate that broader factoring services reached $4.56 trillion in 2026, with long-term trajectories pointing toward $7.31 trillion by 2034.

-

The Digital Platform Surge: The specialized software layer—encompassing digital and tech-enabled invoice financing platforms—is growing at an exponential 21.1% CAGR, rising from $15.46 billion in 2025 to $18.72 billion in 2026.

-

Long-Term Tech Valuation: Driven by the integration of automated underwriting and cloud-driven API processing, the global invoice financing platform market is projected to reach $129.89 billion by 2035, maintaining a robust 20.50% CAGR.

Segment & Provider Breakdown

-

Product Composition: Digital invoice factoring holds the dominant share of the platform market at 72%, though automated invoice discounting is currently expanding at the fastest growth rate.

-

Recourse vs. Non-Recourse: The recourse segment (where the seller retains default risk) commands the highest market share at approximately 65%. However, non-recourse setups are growing rapidly at a 13.0% CAGR as companies look to transfer credit risk during uncertain economic cycles.

-

Domestic Dominance: Converting domestic accounts receivable into cash represents the foundation of the market, controlling between 73.06% and 75.5% of total volume (valued at $2.9 trillion).

-

International Velocity: Cross-border and international factoring activities are outpacing domestic growth with a 9.33% CAGR, as integrated digital platforms simplify complex cross-border documentation.

-

Institutional Domination: Traditional banking institutions lead the market with a share between 64.59% and 87.37% due to their existing corporate relationships and low cost of funds.

-

Fintech & Non-Bank Expansion: Non-banking financial companies (NBFCs) and agile fintech platforms are expanding their market share at an 8.92% CAGR, capitalizing on flexible lending terms and automated onboarding.

Macroeconomic Triggers & The SME Funding Gap

-

The $5 Trillion Credit Deficit: Small and medium enterprises (SMEs) act as the primary engine for alternative finance, yet the global SME financing gap exceeds $5 trillion annually in unmet working capital needs.

-

SME Capital Reliance: Resource-constrained firms represent 90% of all global businesses and generate 50% of world GDP, making them highly sensitive to payment backlogs.

-

Market Share Ownership: Due to strict collateral requirements from traditional banks, SMEs have turned to alternative lenders, accounting for 68.42% of the total global factoring market share.

-

Emerging Market Access: Over 60% of SMEs in emerging economies report insufficient access to stable daily working capital, causing short-term financing demand in these areas to grow at an 8% to 10% annual clip.

-

Regulatory Compliance Headwinds: Operating across international borders introduces deep operational friction; navigating different cross-border regulations can increase compliance costs for global funding providers by up to 15%.

Target Sectors & Operational Benchmarks

-

Manufacturing Supply Chains: The manufacturing sector is the largest single consumer of invoice financing, contributing 24% to 29.62% of the global market share due to its long supply chains, high inventory costs, and delayed buyer payments.

-

High-Velocity Industries: Beyond manufacturing, automated liquidity adoption is clustered heavily across transportation, logistics, wholesale distribution, and B2B services, where cash timing directly dictates daily capacity.

-

Healthcare Acceleration: The healthcare services sector has emerged as the fastest-growing end-use industry segment, driven by complex payer reimbursement cycles.

-

The Core Performance Dashboard: Operational success is measured by a unified dashboard rather than isolated metrics. Advanced management platforms aim to optimize four core benchmarks simultaneously:

-

Advance Rate: Upfront liquidity deployment targeted between 70% and 90% of invoice value.

-

Funding Speed: Compressing the capital deployment cycle from weeks down to hours via API automated verification.

-

Eligible Invoice Share: Maximizing the percentage of the ledger that passes automated risk clearance.

-

Approval Rate: Sustaining high approval rates through real-time, automated analysis of historical B2B payer behavior.

-

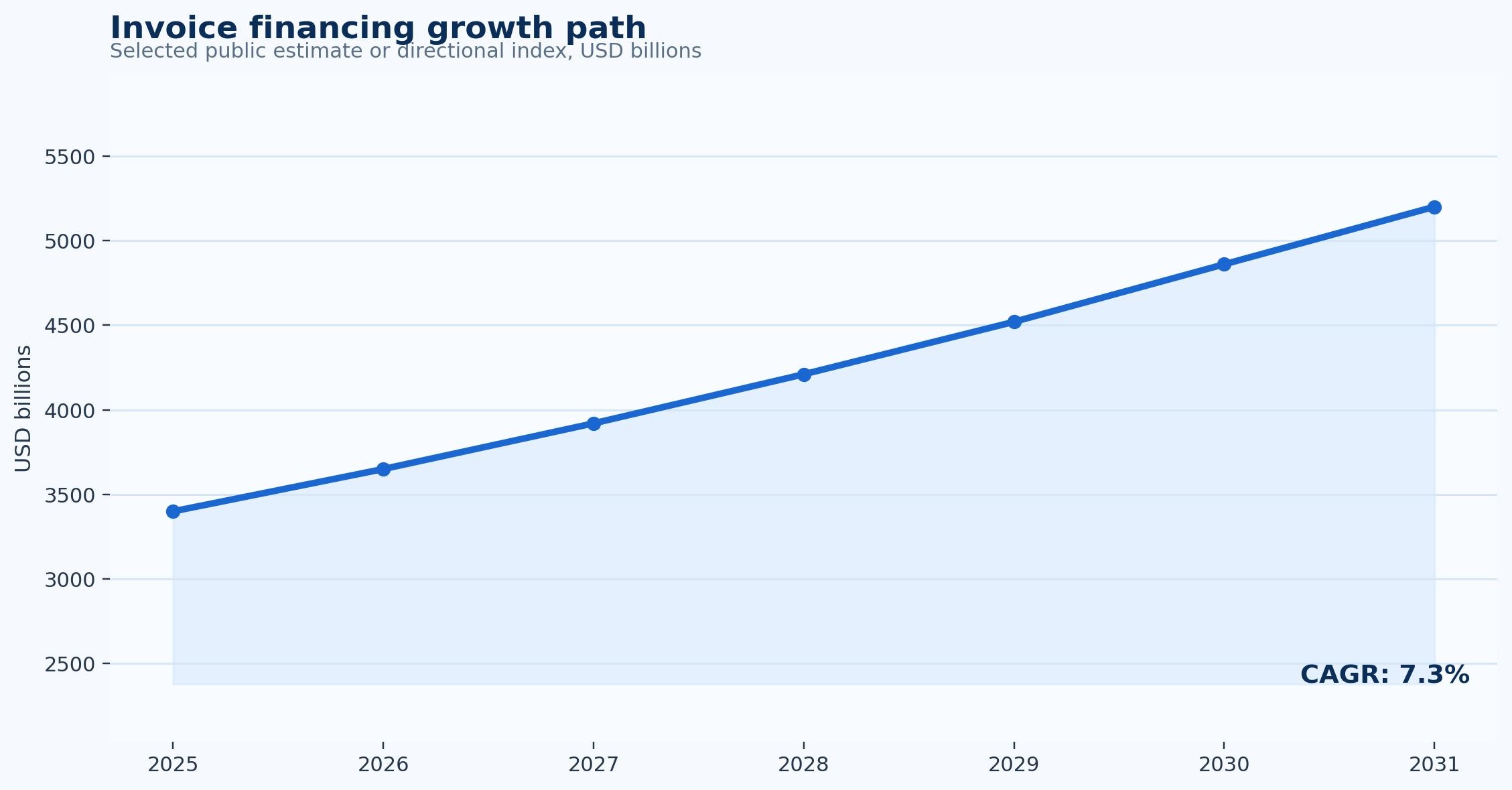

Figure 1. Invoice financing growth path shows the direction of category growth and should be interpreted as a market signal rather than a single operating benchmark.

Why the Workflow Matters Operationally

The operational case for invoice financing begins with work that repeats often enough to create measurable friction. Repetition does not always look dramatic. It can be a manager checking the same spreadsheet every morning, a finance clerk re-entering data, a sales team rebuilding similar estimates, or a lender requesting the same documents from every applicant. Each touch may be small, but the combined workload becomes material when volume grows.

Technology only helps when the workflow is clear. If approval rules are inconsistent, source data is incomplete, or teams disagree about ownership, software can make the confusion faster but not necessarily better. Strong programs usually define the intake channel, required data fields, routing logic, exception categories, approval thresholds, and reporting cadence before scaling automation. That process discipline is often the difference between a successful deployment and a stalled project.

The most useful operational statistics are the ones that point to a decision. A cycle-time metric should tell leaders where work is waiting. An error metric should show whether the problem comes from data capture, policy gaps, missing information, or user behavior. A cost metric should identify whether savings come from fewer touches, less rework, faster approval, better cash timing, or reduced risk exposure.

In practice, teams should treat invoice financing as a workflow redesign project rather than a single technology purchase. The system should make common work easier, route unusual work to the right person, and generate enough data for leaders to see whether the process is improving. When those three outcomes are present, the statistics become management tools rather than marketing claims.

Operational statistics and signals

- A baseline should capture current volume, current cycle time, and the amount of manual work involved before the first workflow change is made.

- Teams should separate normal-path work from exceptions because the exception queue usually explains why averages do not improve as expected.

- A practical pilot should start with a high-volume and relatively repeatable workflow before expanding into unusual or high-risk cases.

- The best evidence of progress is an improvement in advance rate, eligible invoice share, and cost of funds without creating weaker controls.

- Workflow visibility is often valuable even before full automation because it reveals where work waits and who needs to act next.

Adoption Maturity and Segment Differences

Segment differences matter because invoice financing rarely delivers value the same way for every buyer. Smaller companies often care about simplicity, speed, cost, and avoiding administrative overload. Mid-market companies usually care about standardization across teams, locations, or customer groups. Enterprise buyers focus more heavily on integration, controls, reporting, auditability, security, and governance.

Industry differences are just as important. In B2B services and manufacturing, the workflow may be tied to high transaction volume and customer experience. In wholesale distribution and transportation, the same category may be more closely tied to operational accuracy, project control, compliance, or working-capital visibility. This is why a generic adoption percentage can be misleading without context.

The business model also changes the metric set. A company with recurring revenue may measure retention, renewals, and payment reliability. A project-based company may focus on margin protection, estimate accuracy, milestone billing, and revenue recognition. A finance-heavy buyer may focus on cash timing, credit risk, audit trails, and compliance. Useful reporting should reflect the way the business actually makes money and manages risk.

The practical takeaway is that leaders should benchmark against similar workflows rather than only similar company sizes. A small company with complex transactions may need stronger controls than a larger company with simpler repeatable work. A high-growth firm may value speed more than cost reduction. A regulated firm may value documentation and auditability even when the direct labor savings look modest.

Segment statistics and interpretation points

- Small businesses usually prioritize fast setup, simple workflows, and direct savings because administrative capacity is limited.

- Mid-market teams often need stronger standardization across departments, locations, customer groups, or business units.

- Enterprise buyers usually require audit logs, permissions, reporting, data governance, and deeper integration with existing systems.

- Industry use cases differ: B2B services and manufacturing may focus on volume, while wholesale distribution and transportation may focus on accuracy or control.

- The right benchmark should compare workflows that share similar volume, complexity, and risk rather than only comparing companies of similar size.

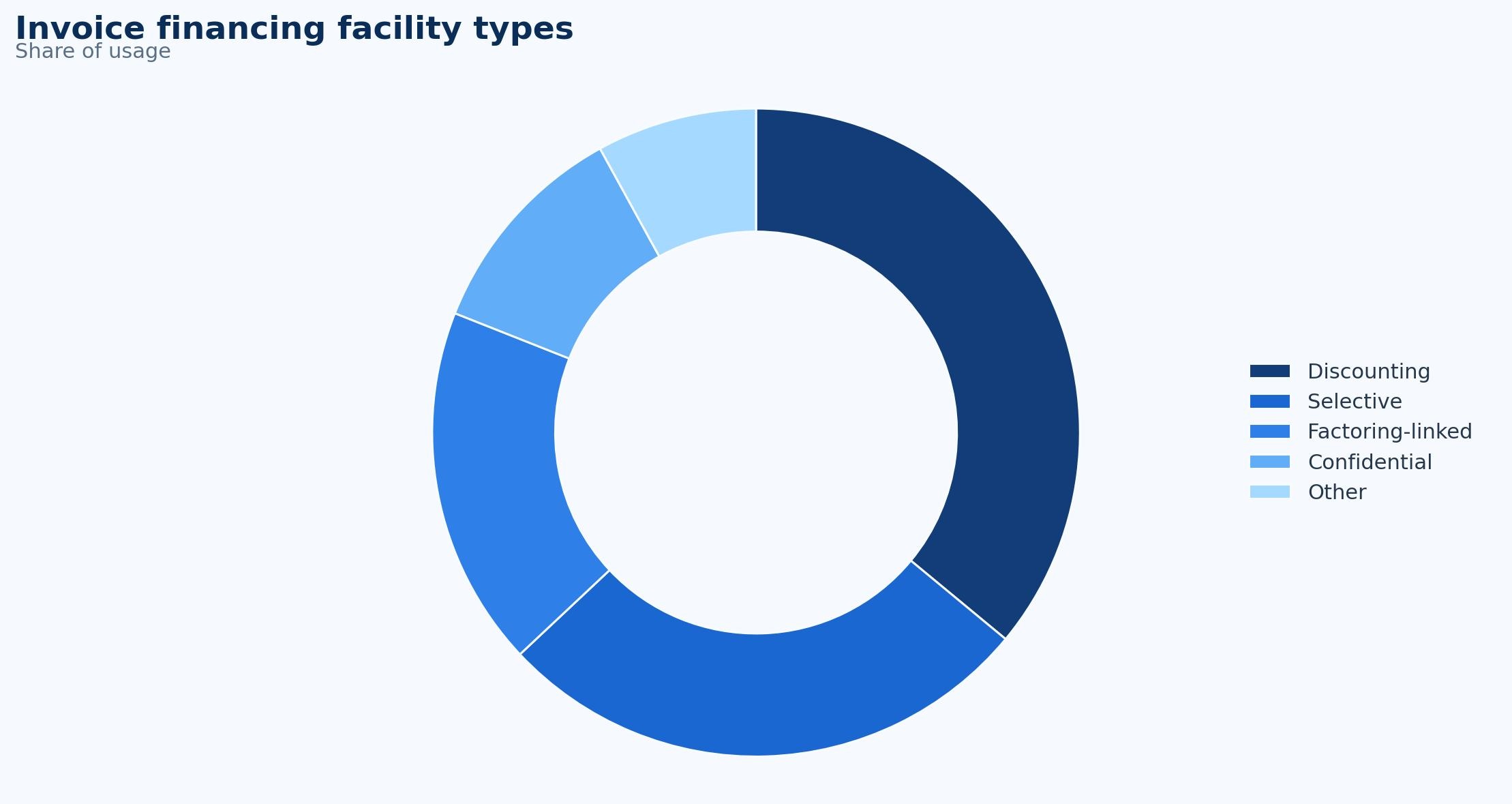

Figure 2. Invoice financing facility types gives a practical segment view of where activity is concentrated across the category.

Technology, AI, and Integration Trends

Technology in this category is moving toward connected data rather than isolated task automation. The most valuable systems pull information from source documents, customer records, bank feeds, payment rails, accounting platforms, workflow tools, and user actions. They then use that data to route work, surface exceptions, calculate risk, and update dashboards without forcing teams to rebuild the same dataset manually.

AI and machine learning are becoming more common, but their role should be understood carefully. In most business workflows, AI is most useful when it helps classify data, detect patterns, recommend next actions, flag anomalies, and reduce repetitive review. It should not remove accountability from financial, credit, compliance, or customer-facing decisions. The strongest deployments combine automation with clear human review points.

Integration is often the limiting factor. A tool that works well by itself may create extra effort if data must still be copied into accounting, CRM, ERP, document storage, payment, or reporting systems. Integration quality affects adoption because users quickly reject workflows that make the first step easier but create reconciliation work later. A strong integration plan should include data ownership, field mapping, exception handling, and backup procedures.

Security and governance are also part of the technology story. The more a system touches payments, customer data, financial records, documents, or approvals, the more important permissions, audit logs, retention rules, encryption, and access controls become. Buyers should ask not only what the system automates, but how it proves what happened after the work is complete.

Technology and integration statistics to watch

- AI is most useful when it improves classification, recommendations, anomaly detection, or data extraction without hiding accountability.

- Integration depth should be measured by how much data moves automatically into accounting, CRM, ERP, payment, reporting, or document systems.

- Poor data quality can create more exceptions after automation, so master data cleanup is often part of the implementation work.

- Permission design matters because more automated workflows can also move sensitive financial, customer, or operational data faster.

- A system should make review easier by showing why an item was routed, approved, rejected, funded, matched, or escalated.

ROI, Cost Savings, and Business Impact

The ROI case for invoice financing should not rely on a single headline saving. A narrow model might count only hours saved. A stronger model also includes lower error correction, faster cycle time, reduced exception queues, fewer customer or supplier inquiries, better cash timing, avoided hiring, fewer compliance issues, and stronger management visibility. These benefits appear in different parts of the organization, so the business case needs to look beyond the immediate user team.

A useful ROI model starts with baseline metrics. Leaders should measure the current volume, manual touch count, average processing time, exception rate, approval delay, error rate, and downstream rework before implementation. Without a baseline, the team may still feel improvement but struggle to prove it. The baseline also helps prioritize which workflow should be automated first.

Hard savings and soft savings should be separated but not treated as unrelated. Hard savings may include fewer manual hours, lower processing cost, reduced outside service spend, or avoided penalties. Soft savings may include better customer experience, stronger employee morale, improved control, and faster access to information. In many operational systems, the strongest value comes from the combination rather than one category alone.

The payback period depends on complexity. A lightweight workflow for a small business may show value quickly because setup is simple. A larger deployment may require process redesign, system integration, data cleanup, training, and governance work. That does not weaken the business case; it means leaders should set expectations around phased rollout, measurable milestones, and operating ownership after launch.

ROI statistics and calculations

- ROI should include hard savings, avoided hiring, lower rework, faster cycle time, reduced error handling, and improved management visibility.

- A one-minute saving across 100,000 annual transactions equals more than 1,600 hours of process capacity before considering error reduction.

- A 10 percent improvement in advance rate can matter more than a larger improvement in a low-volume metric that does not affect cash, customers, or controls.

- The strongest business cases connect cost of funds to a financial or operating outcome rather than describing it only as a dashboard metric.

- Payback depends on implementation complexity, but staged deployments reduce risk by proving the workflow before scaling it across all teams.

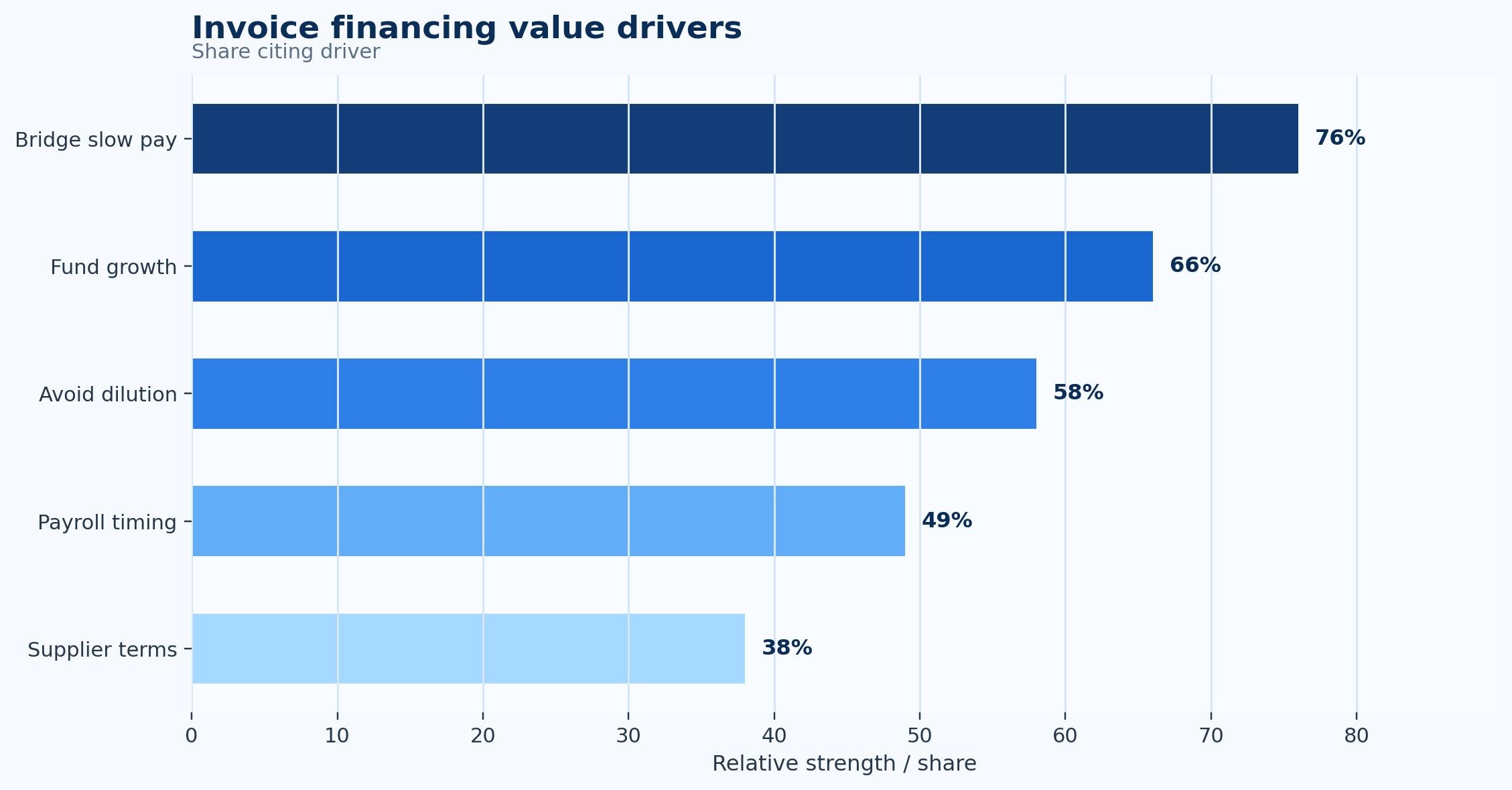

Figure 3. Invoice financing value drivers highlights the business reasons that commonly move the category from experimentation to budgeted adoption.

Controls, Risk, and Governance

The main implementation risk is automating a weak process before fixing the process design. If data is inconsistent, approvals are unclear, or accountability is spread across too many teams, automation may simply move the bottleneck to another place. A well-designed project should identify where decisions are made, what information is required, how exceptions are escalated, and who owns final outcomes.

A second risk is over-automation. Not every transaction, document, application, estimate, or approval should move without review. High-value, unusual, first-time, disputed, regulated, or risky items often need stronger human oversight. The goal is not to remove judgment; it is to reserve judgment for the cases where it matters most.

A third risk is poor measurement after rollout. Many teams measure go-live completion but not operating performance. A system can be technically live while users still route work around it through email, spreadsheets, messaging apps, or offline approvals. Post-launch measurement should track adoption, exceptions, cycle time, accuracy, and user behavior to confirm that the workflow is truly changing.

Governance should also evolve as the workflow matures. Early rules may work for a pilot but break when more teams, regions, products, or transaction types are added. Leaders should review thresholds, permissions, integration logs, exception reasons, and metric definitions periodically. This keeps automation aligned with how the business actually operates.

Risk and control metrics

- High-risk items should keep human review even when low-risk items move through a mostly automated workflow.

- Audit trails should record who changed the data, who approved the action, when it happened, and what rule or evidence supported the decision.

- Exception categories should be tracked over time because they often reveal recurring data, policy, training, or integration problems.

- Governance should include role-based permissions, approval thresholds, review queues, and periodic audits of unusual activity.

- A mature process treats automation as controlled speed, not speed at the expense of accountability.

Metrics Leaders Should Track

The best scorecard for invoice financing should include both activity and outcome metrics. Activity metrics show whether the workflow is being used. Outcome metrics show whether the workflow is producing better results. For example, adoption rate and transaction volume matter, but they should be paired with cycle time, accuracy, cost, conversion, funding, or cash-flow outcomes depending on the topic.

Leaders should track advance rate, funding speed, eligible invoice share, and approval rate as early operating indicators. These metrics usually reveal whether the process is faster and more visible. They should then add cost of funds, DSO change, customer payment risk, and facility utilization to understand quality, risk, and business impact.

The scorecard should also separate averages from exceptions. Average performance can look healthy while a small share of cases create most of the risk or rework. Exception aging, rejected items, manual overrides, late approvals, or high-risk transactions often reveal more about workflow health than a single average number.

Finally, the scorecard needs ownership. A dashboard without an owner becomes background noise. Each metric should have a person or team responsible for investigating movement, explaining variance, and deciding what changes next. This turns statistics into management action.

Scorecard statistics

- Advance rate should be tracked by segment so leaders can see whether improvement is broad or concentrated in one area.

- Funding speed helps reveal whether adoption is expanding or whether users are staying inside old workarounds.

- Eligible invoice share and approval rate show whether the process is becoming faster and more reliable.

- Cost of funds and DSO change connect the workflow to financial value or operating quality.

- Customer payment risk and facility utilization are important for understanding risk, scale, and long-term maturity.

Implementation Priorities

Implementation should begin with a narrow but meaningful use case. Teams often get better results by automating a repeatable workflow with clear rules than by trying to redesign every process at once. The first use case should be large enough to measure, simple enough to stabilize, and important enough for leadership to care about the results.

Data preparation is usually more important than expected. The team should review field definitions, source systems, duplicate records, approval rules, customer or supplier records, historical exceptions, and reporting requirements before rollout. This work can feel slower than software configuration, but it prevents avoidable problems later.

Training should focus on new responsibilities, not only new screens. Users need to understand what the system will do automatically, what they must still review, how to handle exceptions, and which metrics will be used after launch. This reduces resistance because people can see how the workflow will change their daily work.

After launch, leaders should hold a short operating review every month. The review should cover adoption, exceptions, cycle time, errors, user feedback, integration issues, and metric movement. This turns the system into a continuous improvement tool rather than a one-time deployment.

Implementation statistics and checkpoints

- Start with the workflow where advance rate, eligible invoice share, or cost of funds is most visibly underperforming.

- Create a baseline before launch so improvement can be measured without relying on anecdotes.

- Document exception reasons during the pilot because they show where process design needs more work.

- Assign ownership for the post-launch scorecard before the system goes live.

- Expand only after users trust the workflow and the data is clean enough to support decisions.

Future Outlook

The future of invoice financing is likely to be more embedded, more intelligent, and more connected to adjacent workflows. Buyers are increasingly unwilling to accept tools that solve only one step while leaving the rest of the process manual. They want systems that capture data, move work, apply rules, surface exceptions, and report outcomes from one coherent workflow.

AI will likely expand first in areas where the risk is manageable and the pattern recognition value is high. That includes classification, data extraction, anomaly detection, routing recommendations, forecasting, and user guidance. More sensitive decisions will still need governance, audit trails, and human accountability. The companies that benefit most will be those that pair AI with strong process ownership rather than treating it as a shortcut.

Data quality will become a bigger differentiator. As more workflows become automated, poor master data, inconsistent field definitions, duplicate records, and weak integration will become more visible. Companies that invest in clean data foundations will be able to automate more confidently and interpret their metrics more accurately.

The practical outlook is positive but not automatic. Market growth shows that demand is real, but operating improvement depends on implementation quality. Businesses that define the workflow, choose metrics carefully, and review results over time will get more value than those that only adopt the newest tool.

Outlook statistics and watch points

- The category is likely to keep moving toward connected workflows that combine data capture, approvals, analytics, and automation.

- AI will add value where pattern recognition, classification, and recommendation quality can be measured and governed.

- The strongest vendors will likely compete on integration quality, data reliability, workflow configurability, security, and measurable outcomes.

- Buyers will increasingly expect tools to support both daily operations and management reporting.

- Long-term value will depend on whether adoption improves actual business metrics rather than only increasing software usage.

Editorial Interpretation and Decision Quality

The final editorial lens for invoice financing is practical decision quality. A statistic is useful only when it helps a business choose a better workflow, set a better target, or avoid a costly blind spot. For example, a market CAGR explains growth momentum, but it does not tell a finance leader which process to fix first. A cycle-time statistic is more actionable when it is tied to a specific bottleneck, owner, and improvement target.

This is why the best report structure combines market data with operating interpretation. Market data explains why the category is expanding. Workflow analysis explains where value is created. Segment analysis explains why different buyers need different roadmaps. Risk analysis explains what should not be automated blindly. Together, these layers make the statistics useful for planning rather than simply interesting to read.

Decision-quality statistics

- Every statistic should answer 1 of 4 questions: scale, adoption, performance, or risk.

- A strong dashboard should show at least 5 operating indicators before leadership relies on it for planning.

- A meaningful improvement target should be time-bound, such as 30, 60, or 90 days after implementation.

- The best benchmark compares before-and-after performance inside the same workflow, not only external averages.

- A useful report should connect market growth to operational choices, not leave market statistics isolated at the top.

Benchmark planning statistics

- Set a 30-day baseline window before launch so volume, cycle time, exceptions, and rework can be compared after rollout.

- Use a 60-day stabilization window after launch before making broad conclusions about ROI or adoption quality.

- Review the top 10 recurring exception reasons and assign owners for the 3 highest-volume causes.

- Track at least 5 operating metrics and 3 business-impact metrics so the scorecard does not become too narrow.

- Compare results across 3 company-size bands and 5 workflow categories before setting long-term targets.

- A mature process should show improvement in at least 2 outcome metrics without increasing risk exceptions by more than 1 review period.

- For high-volume teams, even a 2 percent reduction in rework can matter if the workflow touches thousands of cases per month.

Regional and Company-Size Planning

Regional planning adds another layer to invoice financing because business infrastructure, payment behavior, regulation, bank connectivity, cloud adoption, and customer expectations are not the same everywhere. A workflow that depends on instant bank data, automated approvals, or digital document exchange may scale quickly in one market and require more manual fallback steps in another. This is why regional statistics should be interpreted alongside infrastructure readiness, not only buyer interest.

Company size changes the roadmap as well. Microbusinesses and smaller firms often want one practical improvement: faster estimates, better funding access, cleaner documents, easier cash visibility, or fewer manual follow-ups. Mid-market companies need repeatability across teams and locations. Large enterprises usually need policy enforcement, audit trails, identity controls, system integration, and reporting consistency across many entities.

A sensible rollout therefore uses different maturity targets by segment. A small company may be successful when 60 percent of a workflow is standardized and visible. A larger organization may need 85 percent or more of routine work to move through controlled rules before the process feels scalable. Highly regulated workflows may need lower automation thresholds but stronger evidence for every exception.

This segment view prevents the article’s statistics from becoming abstract. Market growth explains the category. Company-size and regional planning explain implementation. A business that connects both views can choose a realistic first target, measure progress, and decide when the workflow is ready for wider rollout.

Regional and segment planning statistics

- A small-business target might be 60 percent workflow visibility within the first 90 days rather than full automation from day one.

- A mid-market target might be 75 percent standardized intake across teams before advanced analytics are introduced.

- An enterprise target might be 85 percent routine-path coverage with documented exception queues and monthly governance review.

- A regulated workflow may intentionally keep 10 percent to 20 percent of cases under human review even after automation matures.

- Regional readiness should be scored across 5 areas: digital data availability, payment infrastructure, regulation, integration options, and user adoption.

- A quarterly review should compare at least 3 segments: small accounts, mid-sized operations, and complex enterprise workflows.

- The implementation plan should avoid using a single benchmark when the business operates across multiple regions or customer segments.

- A practical expansion gate is 2 consecutive review periods with stable cycle time, lower exception volume, and no increase in control issues.

Research Depth and Methodology Notes

A deeper research view of invoice financing starts by asking what economic pressure creates demand. In some categories the pressure is liquidity, in others it is labor cost, error risk, compliance exposure, customer experience, or revenue leakage. The same market-size number means different things depending on which pressure is strongest. A buyer that is trying to reduce a two-day approval delay evaluates the category differently from a buyer trying to reduce funding gaps or improve data extraction accuracy.

The second research question is whether the category changes a decision or only changes a task. A task-level tool helps a user complete work faster. A decision-level system changes how the business prices, approves, funds, routes, forecasts, or controls an outcome. Categories that reach decision-level impact usually justify stronger investment because they affect margin, liquidity, customer retention, audit quality, or risk exposure.

A third question is how much of the workflow is measurable after implementation. Better systems leave a data trail around intake, routing, timing, exceptions, approvals, and outcomes. That trail matters because it lets leaders compare teams, identify bottlenecks, and run continuous improvement instead of relying on anecdotal user feedback.

The research also needs to separate durable trends from temporary buying waves. A temporary wave may come from budget cycles, vendor hype, or a narrow regulatory deadline. A durable trend appears when several independent forces point in the same direction: volume growth, buyer pain, measurable ROI, easier integration, stronger data availability, and greater need for control.

Methodology statistics and interpretation rules

- Market estimates should be treated as directional when one source includes services or transaction value and another includes only software revenue.

- Adoption percentages should be read together with maturity indicators such as straight-through processing, exception rate, and integration depth.

- Survey results can overstate maturity when respondents count partial digitization as full workflow automation.

- Operational benchmarks should be normalized for volume because a low-volume process can show different economics from a high-volume process.

- Regional comparisons should account for regulation, banking infrastructure, cloud adoption, and local business-payment behavior.

- Internal baselines should be captured before implementation; otherwise teams may not know whether a 10 percent or 30 percent improvement is realistic.

- A reliable benchmark combines at least 2 external references with the company’s own baseline operating data.

Industry and Use-Case Deep Dive

Industry context fundamentally reshapes how invoice financing platforms perform. In high-velocity sectors like B2B services or staffing, systems are judged by throughput speed and their ability to bridge immediate payroll demands. Conversely, in capital-intensive sectors like manufacturing or wholesale distribution, the exact same software layer is evaluated on margin preservation, multi-way data matching, and supply chain continuity.

A standard, one-size-fits-all industry benchmark offers little practical value. True operational excellence requires evaluating the specific transaction volumes, data structures, and client behaviors unique to each vertical.

Industry-Specific Statistics and Signals

B2B Services: Speed, Throughput, and Cash Continuity

-

The Survival Threshold: Small B2B service firms (under $50 million in revenue) must operate within a tight 15 to 30-day DSO range because they lack the revolving bank facilities needed to absorb late-paying enterprise clients.

-

Mid-Market Bottlenecks: As service firms scale into the mid-market ($50M–$500M), average collections drag out to 30 to 45 days, as manual accounts receivable workflows fail to keep pace with growing client portfolios.

-

The Late-Payment Penalty: When service firms face unexpected cash shocks from overdue invoices, they often turn to credit cards. This can cause monthly interest repayments to spike up to three times higher than traditional working capital facilities.

-

Growth Compression: B2B service firms that maintain predictable working capital access through integrated receivable platforms achieve long-term employment and operational growth rates 1 to 3 percentage points higher than unfinanced competitors.

Manufacturing: Margin Control and Long Supply Chains

-

Market Share Dominance: Manufacturing represents the single largest consumer of invoice financing, capturing 29.22% of the global market share due to its heavy reliance on upfront raw materials.

-

Extended Collection Realities: Enterprise-level manufacturing networks managing multi-entity accounts frequently deal with a baseline DSO stretching to 45 or 60+ days.

-

Inventory Preservation: Integrating automated invoice verification with digital inventory tracking allows manufacturers to identify and close financing gaps early, reducing costly stock-out incidents by more than 20%.

-

Risk Mitigation Preference: Because manufacturers face substantial exposure to economic shifts, non-recourse factoring setups (where the funding provider assumes the credit risk) are growing at a rapid 13.0% CAGR.

Wholesale Distribution: High-Volume Data and Account Fragmentation

-

Automation Software Boom: To handle massive invoice volumes, the global invoice automation software market is expanding at a 13.96% CAGR, on track to reach $12.29 billion by 2033.

-

Eliminating Manual Drudgery: Legacy manual entry takes an average of 5 to 15 minutes per invoice. Modern AI-driven optical character recognition (OCR) platforms extract line-item details in seconds with up to 99% data accuracy.

-

The 80/20 Relationship Rule: In distribution, the top 20% of wholesale accounts typically drive the vast majority of total corporate revenue, making automated prioritization essential so teams don’t waste time chasing small balances.

-

Plugging Revenue Leakage: Automated platforms eliminate manual calculation errors by dynamically tracking early payment discounts across thousands of accounts, flagging unauthorized discounts taken outside agreed windows.

Transportation & Logistics: Fleet Continuity and Asset Velocity

-

Massive Dedicated Ecosystem: The global freight factoring market is on track to rise from $200.76 billion in 2026 to $437.4 billion by 2035, maintaining a steady 8.1% CAGR.

-

The Operational Cost Balance: Shippers typically demand 30- to 90-day payment terms, while carriers must cover immediate fuel, maintenance, and driver payroll costs. This structural gap makes invoice financing vital to fleet survival.

-

The Cost of Liquidity: Freight factoring fees generally range from 1% to 5% of the gross invoice value, depending entirely on the carrier’s volume and the debtor’s credit profile.

-

Cross-Border Multipliers: Driven by global trade diversification, international factoring workflows are growing at a 9.33% CAGR, outperforming domestic alternatives through automated multi-currency processing.

Staffing Agencies: Overcoming the Cash Flow Paradox

-

The Negative Cash Cycle: Staffing agencies operate in an inherently stressful cash cycle—contract workers must be paid weekly or bi-weekly, but corporate clients frequently take 30, 45, or 60+ days to settle invoices.

-

The Growth Trap: In staffing, winning a major new corporate contract actually accelerates short-term cash burn, requiring substantial capital reserves before the first invoice is ever collected.

-

Immediate Funding Lifelines: Specialized payroll funding platforms regularly step in to advance between 80% and 90% of total invoice values within 24 hours of timesheet verification.

-

Fintech Adoption Velocity: Driven by the need for quick capital, small-to-mid-sized staffing agencies are fueling an 8.92% growth rate among non-bank fintech platforms that offer flexible onboarding and automated credit checks.

Operating Example and Practical Business Case

Consider a company that handles 8,000 relevant workflow items each month and still depends on spreadsheet tracking, email approvals, and manual status updates. If each item requires only 4 minutes of avoidable handling, the business is spending more than 530 hours a month on work that does not create additional strategic value. That example is intentionally simple, but it shows why small time savings become meaningful when volume repeats.

Now add quality problems. If 3 percent of those items require rework, 240 cases a month need extra attention. If each rework case takes 20 minutes to investigate, the team loses another 80 hours. If some of those errors affect customers, suppliers, financing decisions, estimates, documents, or compliance evidence, the cost is not only internal labor. It also becomes delay, trust loss, cash uncertainty, or risk exposure.

The same example explains why leaders should not measure only license cost. If a system reduces average handling by 90 seconds, cuts rework from 3 percent to 1.5 percent, and makes exceptions visible earlier, the value may show up across multiple departments. Finance may see cleaner records. Operations may see faster decisions. Sales or service teams may see better customer follow-up. Leadership may see more reliable reporting.

This type of operating example is more useful than a generic ROI claim because it converts statistics into a local baseline. Every organization can replace the volume, time, rework, and cost assumptions with its own numbers. The result is a business case that is grounded in actual workflow economics rather than broad market averages.

Practical operating calculations

- If a team processes 8,000 items per month, every 1 minute of avoidable handling equals about 133 hours of monthly capacity.

- A 3 percent exception rate on 8,000 monthly items creates 240 cases that require investigation before the process can be considered stable.

- Reducing average cycle time by 20 percent can be more valuable than reducing software cost by 5 percent when the workflow affects cash, customers, or compliance.

- A useful target is to review the top 5 exception reasons every month and remove at least 1 recurring root cause each quarter.

- Management dashboards should compare at least 3 views: total volume, exception volume, and business outcome movement.

- For invoice financing, the scorecard should connect advance rate with cost of funds so leaders can see whether activity translates into value.

- Teams should segment results by at least 4 dimensions: business unit, workflow type, company size, and risk level.

Frequently Asked Questions

What does invoice financing measure?

Invoice Financing statistics measure market growth, adoption, workflow volume, operating performance, and business impact. The most useful numbers are not only market-size figures. They also show how teams use the tools, where manual work remains, which segments are growing fastest, and which metrics prove that the process is improving.

Why do published invoice financing estimates differ?

Estimates differ because research firms define the market differently. Some include only software revenue. Others include services, transaction value, financing volume, implementation, platform fees, or adjacent workflow tools. The best approach is to compare direction, assumptions, and operational relevance rather than treating every estimate as directly interchangeable.

Which metrics matter most for invoice financing?

The strongest scorecard includes advance rate, funding speed, eligible invoice share, approval rate. More mature teams also track cost of funds, DSO change, customer payment risk, facility utilization. This combination shows speed, quality, value, and risk rather than only showing whether a tool has been deployed.

How should small businesses use these statistics?

Small businesses should use these statistics as a way to prioritize practical improvements. The goal is not to copy enterprise benchmarks. It is to identify where manual work, payment timing, data quality, approval delays, or customer experience problems are creating avoidable pressure.

How should enterprises use these statistics?

Enterprises should use the statistics to compare process maturity across teams, countries, business units, and systems. At scale, the value often comes from standardization, integration, auditability, and exception management rather than only from time saved by individual users.

What is the most common implementation mistake?

The most common mistake is buying technology before clarifying the workflow. Teams need to define data requirements, approval rules, exception handling, ownership, integrations, and success metrics before expecting the tool to produce consistent results.

How does AI affect invoice financing?

AI can improve classification, data extraction, recommendations, anomaly detection, and workflow guidance. It should still operate inside clear controls, especially when the process affects payments, credit decisions, customer data, financial reporting, or contractual commitments.

What should leaders do before investing?

Leaders should document the current baseline: volume, cycle time, cost, error rate, manual touch count, exception reasons, and downstream rework. That baseline makes it easier to choose the right first use case and prove whether the investment actually improves the business.

Final Takeaway

Invoice Financing Statistics show a category shaped by the same forces affecting modern finance and operations: demand for faster workflows, better data, stronger controls, and clearer visibility. The market numbers show investment momentum, but the more useful story is operational. Businesses want tools that reduce friction, improve decisions, and make work easier to manage as volume and complexity grow.

The most important lesson is that statistics should lead to better questions. Which workflow is slowest? Which errors create the most rework? Which metric would change a customer, supplier, lender, finance, or operations outcome? Which process can be improved first without weakening control? Companies that answer those questions carefully will get more value from invoice financing than companies that only follow market growth headlines.