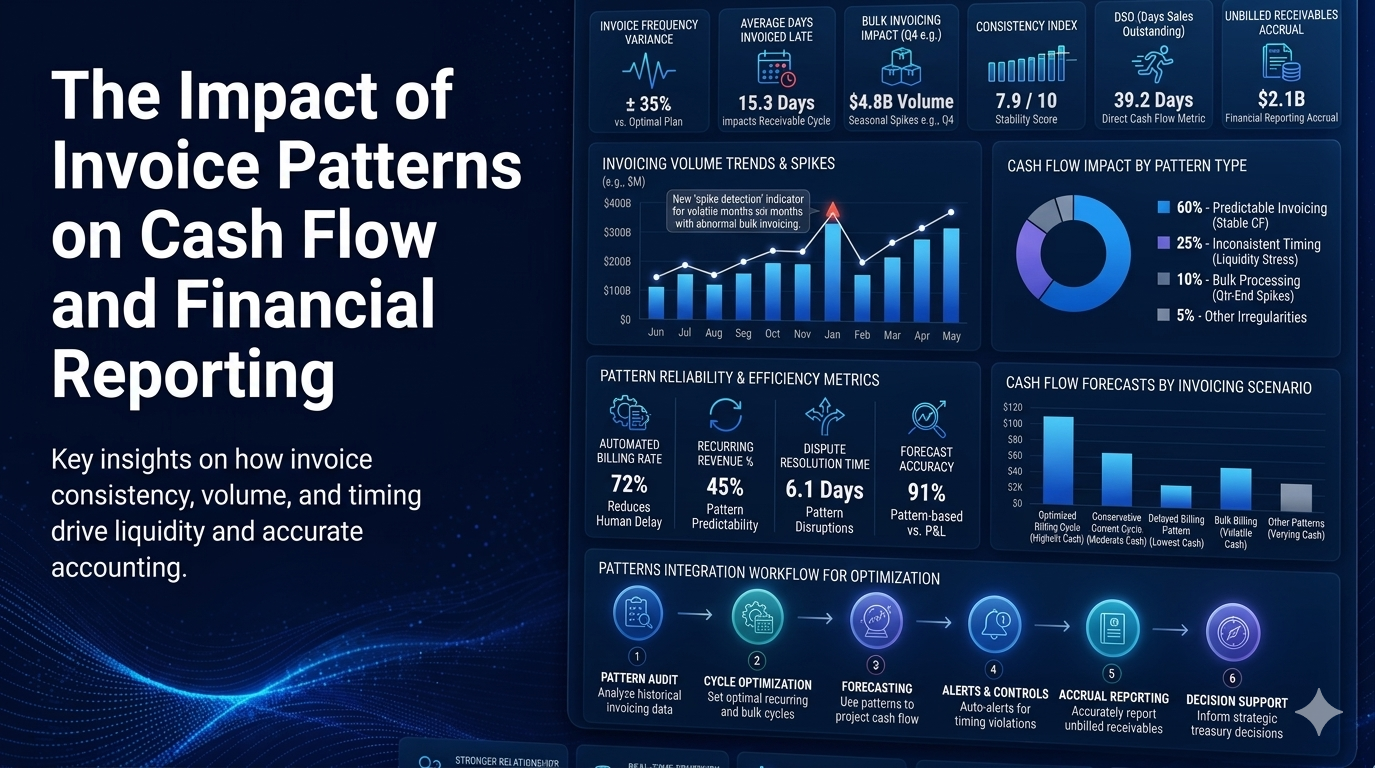

In any business, understanding invoice patterns and their impact on cash flow is crucial for successful financial management. This involves understanding the timing of invoice issuance, the payment terms associated with each invoice, and the actual payment habits of customers.

These factors combined can significantly influence a company’s cash flow and overall financial reporting. In this document, we will explore the intersection of invoice patterns and financial reporting, shedding light on how businesses can streamline their invoicing processes for optimal financial health.

Invoice Timing

Invoice timing refers to the schedule of when a business issues its invoices to its customers. The timing can significantly affect a company’s cash flow, particularly in periods of high sales volume or seasonal business fluctuations. If invoices are issued too early, it could lead to increased debtor days, and if issued too late, there could be a delay in receipt of funds, both of which could result in cash flow issues. Optimizing invoice timing involves strategically issuing invoices at the most appropriate moments to maximize cash inflows while maintaining customer satisfaction and adhering to contractual obligations. This approach ensures that funds are received when needed, supporting stronger financial reporting and overall business stability. In many industries, tools like a photoGraphy invoice template can help standardize billing processes, making it easier to manage timing and improve consistency in invoicing workflows.

Payment Terms

Payment terms are the conditions under which a seller will complete a sale. They outline how, when, and where the buyer is to pay the seller. Common payment terms include net 30, net 60, and net 90, which refer to the number of days that a buyer has to pay a seller after receiving an invoice. These terms are crucial to a company’s cash flow as they can significantly impact the timing and amount of cash inflows.

A shorter payment term (e.g., net 30) can lead to faster cash inflows and improved cash flow. However, it may also put pressure on the customers, possibly affecting customer relationships or even leading to late payments. Conversely, a longer payment term (e.g., net 90) gives customers more time to settle their dues, potentially fostering better relationships, but it can also result in slower cash inflows, potentially affecting the seller’s cash flow and financial reporting. Hence, businesses must carefully consider their payment terms, balancing the need for timely cash inflows with maintaining healthy customer relationships.

Customer Payment Habits

Customer payment habits, or how and when customers typically settle their invoices, can greatly influence a company’s cash flow and financial reporting. Some customers may consistently pay on time, providing a reliable source of cash inflows, while others may habitually pay late, causing uncertainty and potential cash flow issues. In some cases, customers may take advantage of longer payment terms, paying just before the due date, which can delay cash inflows.

Understanding these patterns can help a business predict its cash inflows and manage its cash flow more effectively. Regular review of customer payment habits can also identify potential issues early, such as habitual late payments, allowing the business to take proactive action. This action could include changing payment terms, offering early payment incentives, or implementing stricter follow-up procedures for late payments. By effectively managing customer payment habits, a business can optimize its cash flow and ensure more accurate and reliable financial reporting.

Strategies for Streamlining Invoice Processes

Electronic Invoicing: Electronic invoicing, also known as e-invoicing, replaces traditional paper-based invoicing, making the invoicing process faster and more efficient. This method ensures that invoices reach the customer immediately upon issuance, eliminating the delays associated with postal delivery. Additionally, e-invoices are easier to track and manage, reducing the risk of lost or misplaced invoices and helping to maintain accurate financial records.

Automated Invoice Reminders: Implementing automated invoice reminders is another effective strategy for streamlining invoice processes. These reminders, sent to customers before the invoice due date, help to prompt timely payments. They can be tailored to each customer and set to deliver at specific intervals, like one week before the due date, the due date, and a certain number of days past due. This system helps to reduce the administrative burden of chasing late payments and improves the reliability of cash inflows.

Conclusion

In conclusion, understanding and managing invoice patterns play a pivotal role in the financial health of a business. Optimizing invoice timing, strategically setting payment terms, and efficiently managing customer payment habits are key to ensuring a steady and predictable cash flow. Leveraging technology through electronic invoicing and automated invoice reminders can significantly enhance the efficiency of the invoicing process, fostering prompt payments, minimizing late payments, reducing administrative burdens, and ultimately contributing to improved financial reporting. By being aware of trends in invoicing patterns and taking preventive measures, businesses can ensure that timely cash inflows are maintained and that their financial