Invoice reminders look simple from the outside: an invoice is sent, the due date arrives, and someone follows up if the money does not come in. In practice, reminders are part of the invoice-to-cash system. They touch payment terms, customer relationships, cash application, disputes, payment links, credit control, and the way a business protects cash without turning every late invoice into a collections conflict.

The strongest reminder statistics show why this topic deserves more than a template email. Chaser found that businesses are typically paid late at a rate of 87%, while QuickBooks reported that 56% of surveyed U.S. small businesses were owed money from unpaid invoices. In the U.K., official research estimated GBP 26 billion in late payments outstanding at any given time, with affected firms spending an average of 86 hours per year chasing money that should already have arrived.

Reminder data works best as a management guide, not a list of isolated percentages. The numbers are most useful when they answer the questions a business actually faces: when should reminders start, which channel works, when should a reminder become an escalation, how do countries differ, and how can automation reduce the human cost of chasing without making customers feel harassed?

Executive Invoice Reminder Benchmarks

The headline numbers show the scale of the reminder problem before any workflow is designed. Late invoices are not occasional exceptions for many businesses; they are a recurring operating condition that affects cash planning, hiring, pricing, and customer management.

The numbers that frame the reminder problem

• Chaser’s late-payment research found businesses were typically paid late at a rate of 87%, which means reminder workflows should be treated as normal AR infrastructure rather than an emergency task.

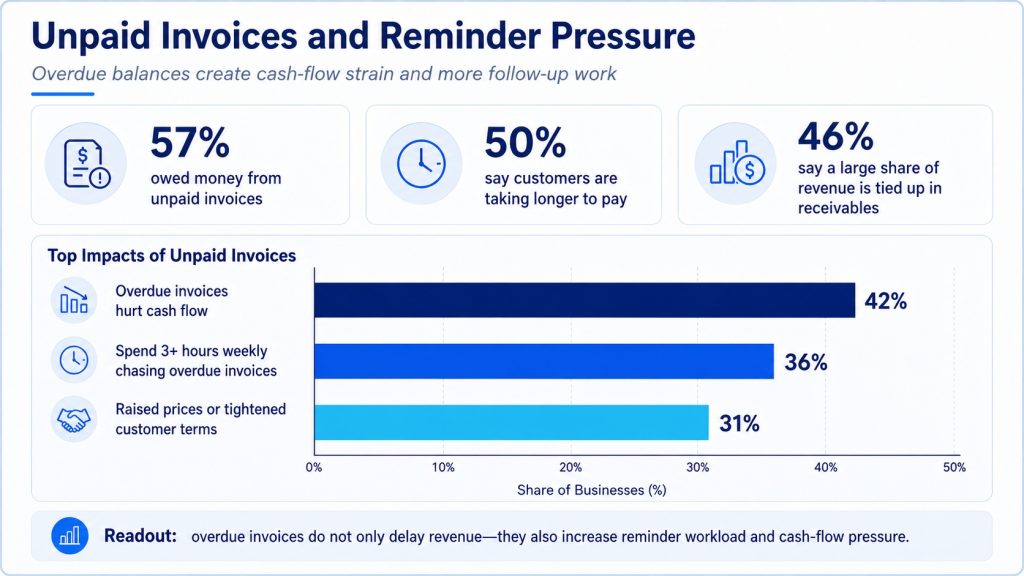

• QuickBooks reported that 56% of surveyed U.S. small businesses were owed money from unpaid invoices, giving reminder work a direct link to working-capital pressure.

• Among affected U.S. firms in the QuickBooks research, the average unpaid invoice exposure reached $17,500, a level that can be material for payroll, materials, tax planning, or owner draws.

• The overdue tail is not minor: QuickBooks found 47% of U.S. small businesses had some invoices more than 30 days overdue, while the average share of invoices past that point was 10%.

• In the U.K., the Office of the Small Business Commissioner estimated GBP 26 billion in late payments outstanding at any given time and 1.5 million businesses affected each year.

• The same U.K. research estimated that late payments cost the economy GBP 11 billion annually and were associated with 14,000 business closures each year.

• Reminder work also consumes time: affected U.K. businesses spend an average of 86 hours per year chasing late invoices, equal to more than 10 full eight-hour workdays.

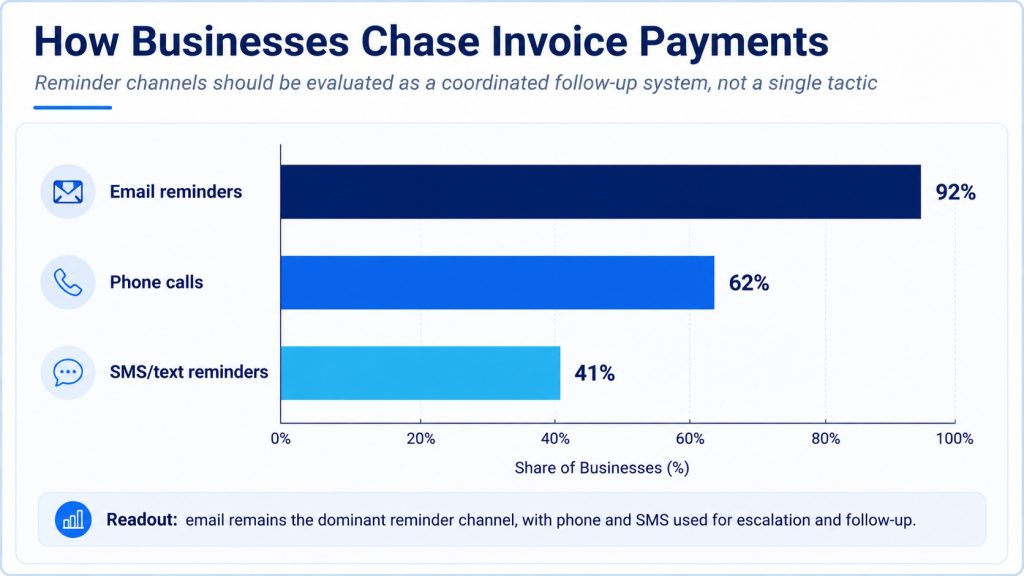

• Email remains the default follow-up channel, with Chaser reporting usage of 93.8%, but phone calls still appeared in 60% of reminder activity.

• Multichannel follow-up matters because Chaser found that text plus email reminders increased the chance of payment within one week of the due date by 56%.

• Country timing data shows why reminder windows should vary by market: Xero reported average late-payment time of 9.0 days in the U.S., 6.9 days in Australia, and 11.6 days in Canada.

• A five-country Xero comparison placed Canada at 10.7 days late on average and Australia at 5.5 days, creating a 5.2-day range across markets.

• Coface’s 2025 comparison found late-payment incidence of 90% in the U.K., 85% in France, 81% in Germany, and 60% in Poland, showing that reminder pressure differs sharply by country.

Editorial readout Invoice reminders should be measured as a cash-flow process, not a courtesy email. The data points to four connected problems: invoices are often unpaid, many payments are meaningfully late, chasing takes real staff time, and the right reminder timing depends on customer behavior, country, channel, and invoice age.

Why Invoice Reminders Matter Before An Invoice Is Late

The best reminder process begins before the due date. A late-payment email can recover some invoices, but the larger opportunity is preventing avoidable delay: missing purchase order numbers, unclear terms, poor payment instructions, disputes that surface too late, and customers who simply do not have the invoice in their payment run.

That is why reminder timing should begin with the invoice itself. Terms need to be visible, payment links should work, the customer should know who to contact, and the invoice should be easy to match to an order, project, subscription, or delivery. If those details are missing, the reminder becomes a repair tool rather than a payment prompt.

Early reminder signals worth tracking

• When QuickBooks found 60% of U.S. firms with longer payment terms reporting cash-flow problems, it showed why pre-due reminders matter most for businesses that already wait weeks for payment.

• Even firms with immediate terms are not immune; QuickBooks reported cash-flow problems among 40% of those businesses, which means reminder quality still matters when the official due date is short.

• Xero’s U.S. timing data, with invoices paid in 28.8 days on average and 9.0 days late, suggests many reminders should begin well before the 30-day mark.

• For Australian small businesses in Xero’s data, an average payment time of 24.1 days and average lateness of 6.9 days creates a shorter but still meaningful reminder window.

• Canada’s average late-payment time of 11.6 days makes a single post-due reminder too weak for many firms, especially where invoice volumes are high.

• The EU Payment Observatory’s finding that only 50% of commercial payments are paid on time reinforces the need for pre-due nudges in markets where delayed payment is common.

• Coface reported average U.K. payment delays of 32 days, which means some customers need more than a friendly overdue note; they need earlier confirmation that the invoice is approved and scheduled.

• For customers on 30-day terms, a reminder sent only at day 31 may arrive after the customer’s payment run has already closed, which can push the invoice into the next cycle even if the customer is willing to pay.

A professional-services firm might send a project invoice with 30-day terms, then wait until day 35 to follow up. If the customer needs a missing purchase order or the invoice was routed to the wrong approver, that reminder is already late. A better process checks status before the due date, confirms receipt, gives the customer a payment path, and reserves the firmer escalation language for invoices that are truly drifting.

Reminder Channels: Email Is The Base, Not The Whole Strategy

Email dominates invoice follow-up because it is documented, low-cost, and easy to automate. But email also gets ignored, filtered, forwarded, or buried in a shared inbox. The channel data shows why the most effective reminder programs usually combine low-friction automation with selective human escalation.

Channel and payment-method benchmarks

• Chaser found email used in 93.8% of late-payment follow-up, making it the default channel for invoice reminders.

• Phone calls still played a role in 60% of reminder activity, which is important for high-value accounts, repeat offenders, disputed invoices, and relationship-sensitive customers.

• A smaller but meaningful group of businesses used SMS, post, WhatsApp, or other reminder methods, with Chaser reporting that broader channel set at 25%.

• When text and email were combined, Chaser reported a 56% higher chance of payment within one week of the due date, suggesting that reminders work better when they reach the customer in more than one place.

• The same reminder research found businesses using SMS plus email were paid within two weeks of the due date at a reported 100% rate, a figure that should be treated carefully but still points to the power of channel reinforcement.

• Bank transfer remained the most common collection method in Chaser’s data at 60%, which affects reminder copy because customers may need banking details, references, or remittance instructions.

• Direct debit appeared as a common collection method for 16.2% of businesses, while card payments were cited by 14.6%.

• Open banking or instant payments accounted for only 2.5% of typical collection methods in the Chaser sample, showing how much room remains for more modern payment options in reminder workflows.

• AR software users were reported as 3 times more likely to be paid before the due date, which links reminders to workflow design rather than message wording alone.

Figure 1. Reminder channels should be evaluated as a coordinated follow-up system, not as a single email template.

Channel readout The practical lesson is not that every invoice needs a phone call or text message. Email should handle routine reminders, while higher-friction channels should be reserved for invoices that are large, old, disputed, relationship-sensitive, or repeatedly missed. The best programs define that escalation logic before an invoice becomes a crisis.

The Late-Payment Burden Behind Reminder Work

Reminder statistics matter because late invoices are not only a communications problem. They become borrowing, pricing, hiring, and supplier-payment problems when cash does not arrive on time. A reminder workflow that saves a few hours is useful; one that improves cash timing can change how a small business operates.

Cash-flow and financing pressure

• QuickBooks reported that 50% of U.S. firms with higher overdue invoice volume faced cash-flow problems, compared with 34% among firms with lower overdue volume.

• Longer terms were also associated with stress, with cash-flow problems affecting 60% of firms using longer terms versus 40% using immediate terms.

• Pricing is one downstream effect: 30% of firms more affected by late payments had raised prices, compared with 21% of less affected firms.

• Among those raising prices, the average increase was 16% for firms more affected by late payments and 10% for those less affected.

• Loan usage was also higher among businesses more affected by late payments, at 21% versus 11% for the less affected group.

• Line-of-credit use followed the same pattern, with 31% of more affected firms using lines of credit compared with 21% of less affected firms.

• Business credit-card use reached 54% among firms more affected by late payments, compared with 46% among those less affected.

• A stronger reliance trend is visible too: 30% of more affected businesses became more reliant on credit cards over the prior year, while the less affected group was at 17%.

• Payment terms affect spending behavior as well; QuickBooks found businesses with 90-day terms charged 40% of monthly expenses to credit cards, compared with 33% for businesses with immediate terms.

• Hiring can be affected before a business feels distressed: 47% of firms with significant payment delays reported hiring skilled workers as a problem, and that share rose to 55% among firms with longer payment terms.

A contractor waiting on milestone payments may not describe the problem as “invoice reminders.” The owner may talk about payroll timing, supplier deposits, credit-card balances, or whether the next job can start. The reminder process is the visible front end of that cash-flow chain. If reminder timing is weak, the business absorbs the cost somewhere else.

Figure 2. Late invoices affect cash flow, borrowing, pricing, hiring, and day-to-day operating flexibility.

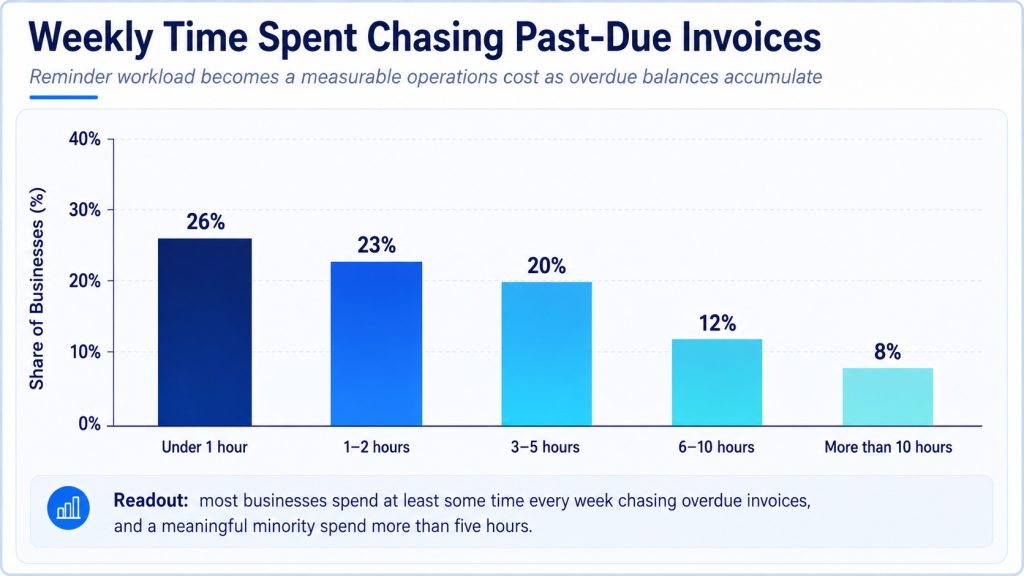

How Much Time Businesses Spend Chasing Invoices

The time cost of reminders is easy to underestimate because chasing is scattered across small tasks. Someone checks the ledger, searches an inbox, asks the account manager whether the customer disputed the invoice, sends an email, waits, calls, updates a note, and repeats the cycle the following week. None of that appears on the invoice, but it is real labor.

Chasing-time benchmarks

• The U.K. Small Business Commissioner estimated 133 million hours of staff time spent chasing late payments across the economy.

• Among affected U.K. businesses, the average time spent chasing late payment was 86 hours per year.

• The same research found 22% of surveyed businesses spending staff time chasing late payments.

• Clockify’s summary found 5% of SMBs spending more than 10 hours per week chasing past-due invoices.

• Another 9% spent 5-10 hours per week, while 20% spent 1-4 hours chasing overdue invoices.

• A larger group, 27%, spent less than one hour per week, which suggests that low-volume chasing still adds recurring interruption even when it is not a dedicated role.

• The fact that 38% reported no time following up on past-due invoices may not mean the problem is absent; it may mean some businesses lack a formal follow-up routine.

• A separate GoCardless U.K. figure found 39% of SMEs spending up to four hours a week chasing late payers.

• The same U.K. GoCardless source reported 12% of SMEs employing someone specifically to pursue outstanding invoices.

• If one affected business spends 86 hours a year chasing, that equals 10.75 eight-hour workdays that could have been spent on sales, delivery, support, bookkeeping, or owner planning.

Figure 3. The operational cost of reminders appears in staff time long before it appears as bad debt.

Workload interpretation Reminder automation should not be judged only by whether it sends emails. The larger question is how much manual lookup, customer-status checking, dispute handling, and rework it removes from each overdue invoice. A reminder sent from poor data still creates work when the customer replies with a question the team cannot answer quickly.

Why Customers Pay Late: Reminder Copy Is Only Part Of The Answer

A stronger invoice reminder program starts by separating intent from friction. Some customers genuinely cannot pay yet. Others are slow because their approval process is broken, the invoice is disputed, the seller invoiced late, or the payment method is inconvenient. The reminder message should reflect the likely reason for delay.

Reasons and frictions behind late payment

• Customer cash-flow issues were cited as a delayed-payment reason by 42% in the Clockify late-invoice summary.

• Customer payment-process delays were close behind at 36%, which means the reminder may need to help the customer route, approve, or schedule the invoice rather than simply ask for payment.

• Late invoicing by the seller appeared as a reason in 33% of delayed-payment cases, showing that the business sending the reminder may have contributed to the delay.

• Invoice disputes accounted for 27% of delayed-payment reasons, a signal that reminders need a dispute path, not just a payment request.

• Large U.K. business invoices were reported as not paid on time at a rate of 25.2%, which matters because smaller suppliers may hesitate to escalate with larger customers.

• UK small businesses dealing with overdue invoices were reported at 62% in the same late-invoice summary, reinforcing that reminder pressure is broad, not limited to a few sectors.

• QuickBooks found 47% of U.S. small businesses had some invoices more than 30 days overdue, which is often where reminder tone needs to shift from helpful nudge to clear escalation.

• When the average share of 30-day-overdue invoices is 10%, a business with high invoice volume needs aging rules, not one-off follow-up decisions.

• If a customer’s approval delay is the issue, a reminder that includes invoice date, PO number, amount, payment link, and contact person is more useful than a generic ‘please pay’ message.

• If a dispute is the issue, the most important reminder may be a resolution request, because another payment link does not remove the reason the invoice is stuck.

| Likely cause | What the reminder should do | Useful signal |

|---|---|---|

| Cash-flow pressure | Offer a clear payment date request, partial-payment option, or escalation path. | Customer replies with timing but not a dispute. |

| Approval delay | Restate PO, job, invoice number, due date, and approver contact. | Customer says the invoice is waiting for internal approval. |

| Invoice dispute | Move quickly to issue resolution, not repeated payment requests. | Customer questions amount, scope, delivery, or tax. |

| Payment friction | Add payment link, bank details, remittance reference, and card/ACH options. | Customer asks how or where to pay. |

| Habitual delay | Use account-level rules and earlier pre-due confirmation. | Customer repeatedly pays after the same aging bucket. |

Reminder Timing: From Pre-Due Nudge To Escalation

A reminder program works best when timing is deliberate. Sending a gentle note before the due date is different from sending a day-30 notice, a day-60 escalation, or a final collections warning. The right sequence depends on invoice value, customer history, country norms, payment terms, and whether the invoice is disputed.

Timing and aging benchmarks

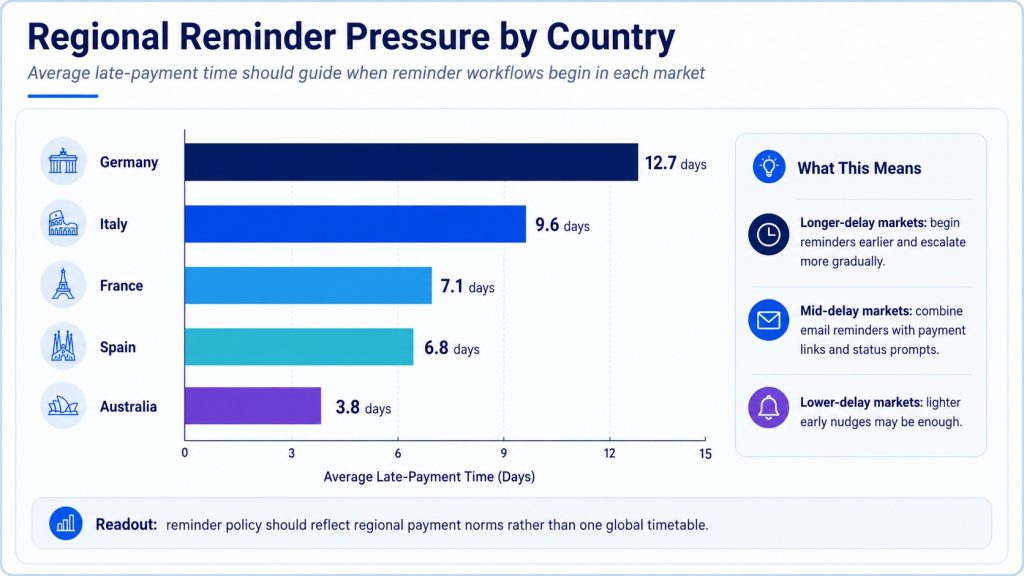

• Xero’s five-country comparison found average late-payment time ranging from 5.5 days in Australia to 10.7 days in Canada, which supports market-specific reminder calendars.

• In the same comparison, U.S. invoices were 8.8 days late on average, while U.K. invoices were 6.6 days late and New Zealand invoices were 7.1 days late.

• Canada’s average time to be paid reached 29.8 days, while the U.S. average was 28.5 days and Australia’s was 23.6 days.

• Xero’s more recent U.S. update showed average time to be paid at 28.8 days, with the late-payment measure increasing by 0.6 days from the prior quarter.

• Australia’s Xero update showed average time to be paid at 24.1 days, with average lateness at 6.9 days.

• Canada’s average late-payment time rose from 10.5 days to 11.6 days across the reported periods, making earlier confirmation especially useful for Canadian receivables.

• Coface reported average U.K. payment delay at 32 days, which means a day-30 reminder can already be late in practical terms for many invoices.

• The EU Payment Observatory noted that average payment periods exceeded 60 days in B2B transactions and also exceeded 60 days in G2B transactions, a reminder that some markets need long-cycle collection discipline.

• EU Observatory analysis also found that only 50% of commercial payments were paid on time, making due-date-only reminders insufficient in many cross-border or public-sector contexts.

Figure 4. Reminder timing should reflect country payment behavior, not only the invoice due date printed on the document.

| Invoice stage | Reminder goal | Best tone |

|---|---|---|

| Before due date | Confirm receipt, approval status, and payment path. | Helpful and preventive. |

| Due date | Make payment easy and remove last friction. | Clear and service-oriented. |

| 7-14 days overdue | Ask for payment date and identify blockers. | Firm but relationship-safe. |

| 30+ days overdue | Escalate ownership, document history, and request commitment. | Direct and documented. |

| 60-90+ days overdue | Move to credit hold, formal escalation, payment plan, or collections review. | Controlled and policy-based. |

Regional Reminder Pressure: Country Context Matters

Invoice reminders are shaped by local payment culture, legal expectations, business size, public policy, and payment infrastructure. A global business should not assume that a reminder cadence built for one market will work everywhere. The regional statistics show large differences in late-payment frequency, average delay, and the business cost of chasing.

Regional and country benchmarks

• QuickBooks’ U.K. late-payment report found 62% of surveyed small businesses owed money from unpaid invoices, compared with 56% in the U.S. report.

• The U.K. report also found 54% of small businesses had invoices more than 30 days overdue, while the U.S. figure was 47%.

• Coface reported that 90% of U.K. companies experienced late payments in the past year and 44% said delays were more frequent than before.

• France also showed high late-payment incidence in the Coface comparison at 85%, while Germany was at 81% and Poland at 60%.

• The same Coface comparison placed Asia at 49% and Latin America at 51%, showing that regional comparisons depend heavily on the sample and market definition.

• For U.K. business size, Coface reported average payment terms of 46 days among micro and small companies and 56 days among large companies.

• More frequent delays were reported by 50% of micro and small U.K. enterprises, compared with 39% of mid-sized companies and 42% of large companies.

• Micro and small U.K. businesses expecting better cash flow from reforms reached 68.5%, showing why policy discussions and reminder practice often overlap.

• In Australia and New Zealand, GoCardless reported 48% of Australian businesses and 51% of New Zealand businesses waiting longer for payments than 12 months earlier.

• Australian businesses paid late by larger customers appeared at 53% in EU Observatory non-EU analysis, reinforcing the small-supplier power imbalance.

• The annual cost of late payments to Australian small businesses was reported at EUR 620 million in the EU Observatory non-EU review.

• The same review noted that 80% of late payments in Australia were less than 30 days late, which makes early reminders and fast payment paths especially relevant.

• For the EU, 52% of companies reported difficulties due to late payments, and the on-time commercial payment share was only 50%.

• Selected non-EU countries saw 53% of businesses increasing time, costs, and resources to chase overdue invoices, a direct reminder of the operational burden.

Regional readout Regional data matters because it helps a business choose timing, tone, and escalation. In a market where many invoices are only a week late, reminders should be early and friction-removing. In markets with long payment periods or frequent delays, reminders need account ownership, documented escalation, and credit-policy support.

Australia And New Zealand: Reminder Stress, Pricing, And Growth Trade-Offs

Australia and New Zealand are useful reminder markets because the data connects late payment to behavior, not only invoice aging. The issue is not simply that invoices arrive late. Many businesses change pricing, avoid difficult customer conversations, consider refusing future work, or delay investment because reminders are uncomfortable and cash remains uncertain.

ANZ reminder and cash-flow signals

• GoCardless reported that 68% of Australia/New Zealand respondents agreed late payment is an inevitable cost of doing business, which can normalize weak reminder habits.

• Businesses more likely to discuss late payments with customers than last year reached 56%, suggesting that payment conversations are becoming more explicit.

• Australian businesses considering adjusted pricing to offset delays stood at 34%, compared with 29% in New Zealand.

• Australian businesses considering refusing future work from chronic late payers reached 34%, while the New Zealand figure was 28%.

• A serious pressure signal appeared in the 10% of respondents considering business closure because of late payment pressure.

• If paid on time, 24% of Australian businesses said they would invest in expansion, while the New Zealand share was 32%.

• Hiring was also affected, with 17% of Australian businesses and 14% of New Zealand businesses saying they would hire more people if paid on time.

• Avoiding money conversations was linked with stress: 38% of Australian respondents and 43% of New Zealand respondents reported increased work stress.

• The personal-stress numbers were even sharper in New Zealand at 48%, compared with 36% in Australia.

• The gap between New Zealand and Australia in businesses waiting longer for payment was 3 percentage points, with New Zealand at 51% and Australia at 48%.

This is where reminder design becomes a customer-relationship issue. A polite reminder sent early may protect the relationship better than a frustrated phone call after the invoice is already a month overdue. In markets where payment conversations create stress, reminders should be clear, calm, and predictable enough that customers know the rules before emotion enters the exchange.

Industry Reminder Pressure Is Not Evenly Distributed

Industry differences change how reminders should be written. A construction firm working around milestone approvals needs different escalation from a subscription business, a marketing agency, or an education provider. The industry data does not provide a complete reminder playbook, but it does show which sectors are more likely to need earlier, firmer, or more automated follow-up.

Industry patterns worth watching

• Chaser reported marketing and advertising businesses in its sample as having 100% of payments late, with 60% paid at least 15 days after the due date.

• Construction also appeared at 100% typically paid late, with 36% of payments usually arriving at least 15 days after the due date.

• IT businesses were paid late at a rate of 81%, and 31% were paid more than 30 days after the due date.

• Financial services firms were typically paid late at 85%, with 23% usually paid at least 15 days late.

• Accounting firms were paid late at 81%, while 43% were typically paid at least 15 days late.

• Education businesses showed a different pattern: 20% were paid before the due date, 60% within one week of the due date, and 20% within two weeks.

• Accounting firms also appeared in the AR workload data, where 11% spent at least 7 hours managing AR tasks.

• For agencies and professional services firms, a reminder can often reference project stage, retainer period, or approval history, while construction reminders usually need milestone, change-order, and site documentation details.

| Industry situation | Reminder implication | What to include |

|---|---|---|

| Project work | Confirm approval before the due date. | Milestone, scope, PO, delivery evidence. |

| Recurring service | Use predictable reminders and account history. | Subscription period, renewal term, payment link. |

| Construction | Separate dispute, retention, and milestone timing. | Project stage, invoice schedule, change orders. |

| Professional services | Protect relationship while documenting follow-up. | Engagement name, approver, prior correspondence. |

| Education/nonprofit | Keep tone helpful and administrative. | Term/session reference, payment plan instructions. |

Payment Links, Automation, And The Reminder Experience

A reminder should not only ask for payment; it should make payment easier. If a customer has to search for bank details, re-enter invoice numbers, request a copy invoice, or ask where to send remittance information, the reminder has failed as a payment experience. Payment links, self-service portals, direct debit, and AR automation can reduce that friction, but only if the invoice data is clean.

Automation and payment-experience stats

• Chaser’s finding that AR software users were 3 times more likely to be paid before due date suggests that timing and workflow automation can change payment behavior.

• The same research showed bank transfer still dominant at 60%, which means reminders often need to include clear remittance references, not just a ‘pay now’ button.

• Direct debit’s 16.2% collection-method share points to recurring-payment opportunity for customers with predictable invoices.

• Card payments at 14.6% matter for smaller invoices and service businesses where convenience may outweigh processing fees.

• Open banking or instant payments at 2.5% show that the newest payment methods still have room to expand in reminder workflows.

• For U.S. firms with higher overdue volume, business credit-card usage reached 54%, which shows how unpaid invoices can push expenses onto more expensive working-capital tools.

• A payment-link reminder is most useful when it removes friction at the exact moment the customer is ready to pay; otherwise it becomes another line in an email.

• For recurring customers, direct debit or automatic payment authorization can reduce reminders entirely, but only when onboarding, consent, and invoice review are handled carefully.

• For B2B invoices, the payment experience still needs remittance data because fast funds without clean posting can leave the invoice open in the ledger.

A SaaS company may discover that its reminder problem is not the reminder text. Customers may be willing to pay, but the invoice goes to an old billing contact or the payment link expires before the AP run. In that case, a reminder workflow should update billing contacts, trigger pre-due confirmation, and include a live payment path. The more payment friction is removed, the less emotional the follow-up becomes.

When Reminders Should Become Escalation

A reminder is not the same as a collections notice. The earlier stages should make payment easy, confirm approval, and resolve confusion. Escalation is needed when the invoice is old, the customer is silent, payment promises are missed, or the account shows repeat behavior. The data helps define where that shift belongs.

Escalation signals and customer-risk markers

• When 47% of U.S. small businesses have invoices more than 30 days overdue, day-30 should be treated as a policy threshold, not just another reminder date.

• The U.K. figure was even higher in QuickBooks’ regional data, with 54% of small businesses reporting invoices overdue by more than 30 days.

• Coface found only 3% of U.K. companies refusing to grant credit to buyers, even though 90% experienced late payments in the past year.

• The same Coface data showed 37% of U.K. companies using 1-30 day payment terms, which means many reminders should be active well before a 60-day escalation point.

• Micro and small U.K. companies had average payment terms of 46 days, while large companies averaged 56 days, creating different expectations for reminder cadence.

• UK businesses believing late payments are a deliberate free-finance strategy reached 18% in EU Observatory non-EU analysis, which supports firmer language for repeat late payers.

• UK SMEs negatively affected by late invoices reached 73% in the same non-EU review, while the average late-payment amount owed was reported at EUR 32,000.

• Australian businesses considering refusing future work from chronic late payers reached 34%, a signal that escalation can eventually become a sales and credit decision.

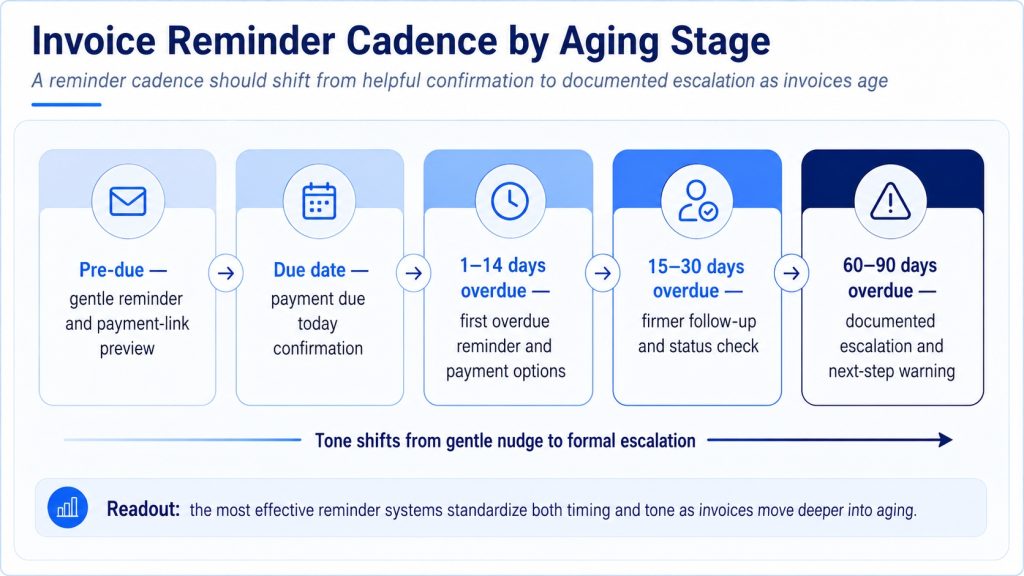

Figure 5. A reminder cadence should shift from helpful confirmation to documented escalation as invoice age and customer risk increase.

Escalation rule A good escalation policy removes guesswork. It should define who owns each aging bucket, when account managers are involved, when service or credit hold is considered, when payment plans are allowed, and when a legal or collections pathway is appropriate. Without those rules, reminders become inconsistent and easier for customers to ignore.

How To Write Reminder Messages That Still Feel Human

The best reminder copy is specific, short, and calm. It should not sound like a generic template pasted into every customer thread. At the same time, it should not be so soft that the due date disappears. Strong reminders combine clarity with a payment path and a reason to respond.

Reminder writing principles backed by the data

• Because email appears in 93.8% of reminder follow-up, the first improvement is often better subject lines, invoice identifiers, and concise copy rather than a new communication channel.

• Phone follow-up at 60% shows that a human conversation still matters when invoices are large, disputed, or repeatedly ignored.

• Since 27% of delayed payments can involve invoice disputes, reminder copy should make it easy for the customer to raise an issue instead of silently delaying.

• Because customer payment-process delays appear at 36%, reminders should ask whether the invoice is approved or scheduled, not only whether payment has been made.

• When customer cash-flow issues appear at 42%, a reminder may need a committed date or payment-plan conversation rather than repeated polite nudges.

• For businesses where sellers themselves invoice late, the 33% late-invoicing cause is a reminder that internal discipline comes before customer blame.

• Since text plus email can increase one-week payment likelihood by 56%, reminder programs should test channel reinforcement for accounts that ignore email.

• Because reminders can create stress, especially where 38% of Australian and 43% of New Zealand respondents reported avoiding money conversations and increased work stress, tone matters as much as cadence.

A natural reminder might say: “Hi Maya, I wanted to confirm invoice 1047 is with the right approver before Friday’s due date. The payment link is included below, and I can resend the purchase-order details if needed.” That message is specific, early, and useful. It does more than ask for money; it reduces the work the customer has to do to pay.

Reminder Metrics Every Business Should Track

Invoice reminder performance should be measured in a simple scorecard. The goal is not to create a complex dashboard for its own sake. The goal is to know whether reminders are reducing overdue exposure, staff chasing time, dispute delays, and cash-flow stress.

| Metric | Why it matters | Useful benchmark context |

|---|---|---|

| Invoices paid before due date | Shows whether pre-due confirmation and payment options are working. | AR software users were reported as 3 times more likely to be paid before due date. |

| Average days late | Shows how long cash is drifting after the due date. | Xero reported 9.0 days late in the U.S. and 11.6 in Canada. |

| 30+ day overdue share | Separates mild delay from aging risk. | QuickBooks reported 47% of U.S. firms with some 30+ day overdue invoices. |

| Reminder response rate | Shows whether customers engage before escalation. | Use separate tracking for email, phone, SMS, and portal notes. |

| Dispute-related delays | Prevents repeated payment requests when the invoice is blocked. | Invoice disputes appeared in 27% of delayed-payment reasons. |

| Chasing hours | Captures the hidden cost of manual reminders. | Affected UK businesses averaged 86 hours per year chasing late payment. |

| Payment method after reminder | Shows whether reminders are also improving payment convenience. | Bank transfer, direct debit, cards, and instant methods create different posting needs. |

Scorecard stats to watch

• Aging risk should be reviewed weekly when the business has meaningful exposure beyond 30 days overdue.

• Chasing workload deserves its own metric when even 1-4 hours per week becomes recurring AR labor.

• Customer response time should be tracked separately from payment time because a quick reply may still reveal a dispute, approval delay, or cash-flow constraint.

• Payment method after reminder is useful because a customer who pays by bank transfer may still leave the AR team waiting for remittance detail.

• Country-level days-late data should influence reminder calendars because a 5.2-day late-payment range across five countries is large enough to change timing.

• Account-level history matters because a customer that repeatedly pays at day 45 should not receive the same reminder sequence as a first-time late payer.

A 90-Day Invoice Reminder Improvement Plan

Statistics become useful when they lead to a process change. A 90-day reminder plan can improve cash timing without overwhelming the finance team. The key is to make the first month diagnostic, the second month operational, and the third month measurable.

| Timing | What to do | Expected output |

|---|---|---|

| Days 1-30 | Build the baseline: average days late, 30+ day overdue exposure, reminder channels, dispute causes, and chasing hours. | A clear map of where reminders are late, manual, or ineffective. |

| Days 31-60 | Rewrite reminder templates, add pre-due confirmation, add payment links where appropriate, and create escalation rules by aging bucket. | A repeatable reminder cadence that separates routine follow-up from risk escalation. |

| Days 61-90 | Measure payment timing, response rate, dispute resolution, payment method after reminder, and staff time saved. | A reminder scorecard tied to cash flow rather than email volume. |

This plan should be adjusted by invoice value and customer type. A low-value recurring invoice may need automated reminders and a payment link. A high-value B2B invoice may need an account-manager call, approver confirmation, and a documented escalation path. A disputed invoice should move away from reminder volume and toward resolution speed.

Customer Segmentation: Which Accounts Need A Different Reminder Path

A mature reminder process should not treat every account the same. A small one-time invoice, a repeat customer with a clean history, a national account with a formal AP run, and a chronically late buyer all need different timing. Segmentation keeps reminders from becoming either too soft for risky accounts or too aggressive for customers who simply need better payment instructions.

The data supports a segmented approach because late-payment exposure is not evenly distributed. Some customers create small administrative delays; others create financing pressure, staff workload, and policy questions. The practical goal is to decide which accounts can stay inside light automation and which ones require earlier human ownership.

Segmentation stats that should change reminder rules

• For businesses with higher overdue invoice volume, QuickBooks reported cash-flow problems at 50%, which makes overdue volume a strong trigger for earlier account review.

• The cash-flow problem rate was 34% among firms with lower overdue volume, showing that invoice aging concentration matters as much as total invoice count.

• Firms using longer payment terms reported cash-flow problems at 60%, which suggests that accounts on extended terms should receive pre-due confirmation rather than only post-due reminders.

• Immediate-term businesses still reported cash-flow problems at 40%, so short terms do not remove the need for clear follow-up and easy payment paths.

• When more affected firms showed loan usage at 21% versus 11% for less affected firms, the data connected overdue invoices to external financing pressure.

• Line-of-credit usage showed the same pattern at 31% versus 21%, making chronic late accounts a working-capital management issue.

• Business credit-card usage among more affected firms reached 54%, which means late invoices can push routine expenses onto higher-cost payment tools.

• A customer responsible for repeated day-30 balances should not receive the same reminder path as a customer with one small invoice delayed by a purchase-order correction.

• For accounts where payment-process delay is the recurring issue, the 36% process-delay figure supports reminders that ask about approval status and scheduled payment date.

• For accounts where disputes recur, the 27% dispute-related delay figure supports moving those reminders into a resolution workflow rather than sending more payment requests.

• For accounts with known customer cash-flow pressure, the 42% cash-flow-delay figure supports earlier conversations about payment timing, partial payment, or agreed payment plans.

• For customers who simply miss the invoice, channel reinforcement matters because text plus email was associated with a 56% higher chance of payment within a week of the due date.

| Account type | Reminder path | Why it works |

|---|---|---|

| Clean repeat payer | Light pre-due confirmation and automated due-date reminder. | Avoids unnecessary friction while protecting the due date. |

| Slow but responsive payer | Earlier status check and clear payment-date request. | Turns vague delay into a scheduled payment conversation. |

| Dispute-prone account | Route to issue owner before repeating reminder emails. | Prevents reminder volume from replacing problem resolution. |

| Large or strategic customer | Coordinate AR, account manager, and customer AP contact. | Protects the relationship while keeping payment visible. |

| Chronic late payer | Use documented escalation, credit review, and account-level rules. | Stops each invoice from being treated as a new surprise. |

Segmentation readout The best reminder workflows do not become more aggressive by default. They become more specific. A customer who needs a missing PO number should receive information. A customer who ignores three reminders should receive escalation. A customer with a legitimate dispute should receive resolution. Segmentation keeps those paths separate.

How More Statistics Should Change Reminder Policy

More statistics only help when they clarify reminder policy. The strongest reminder decisions are based on evidence from several parts of the payment cycle: timing, communication channel, country, customer type, cash-flow exposure, and staff workload. Each number should point to a decision.

Policy decisions supported by the reminder data

• Chaser’s 87% late-payment finding is high enough that reminder policy should be documented before invoices become overdue, not invented account by account.

• When half of businesses spend more than four hours per week on AR tasks, reminder work belongs in labor-cost and productivity discussions, not only in email-template reviews.

• A monthly AR-management struggle affecting 26% of businesses points to exception handling as a core problem: the reminder system should reduce manual follow-up, not create more of it.

• The U.K. late-payment stock of GBP 26 billion makes cash exposure a better prioritization metric than raw invoice count.

• Annual chasing time estimated at 133 million hours in the U.K. gives finance leaders a clear test for automation: is the system removing work or only sending messages faster?

• Australia’s estimated EUR 620 million annual small-business late-payment cost shows why reminder strategy also belongs in resilience and owner-planning discussions.

• In selected non-EU countries, 53% of businesses increased time, cost, and resources to chase overdue invoices, so process improvement has to cover staffing and workflow as well as wording.

• EU Observatory data showing 80% of Australian late payments below 30 days supports earlier reminders, because many invoices can be recovered before late-stage collections pressure is needed.

• A U.K. finding that 18% of businesses viewed late payment as a deliberate free-finance strategy suggests repeat late payers may need commercial-policy review rather than another polite nudge.

• Only 3% of U.K. companies in the Coface survey refused credit to buyers, which suggests many businesses may tolerate risky payment behavior longer than their cash position allows.

A finance team can turn those numbers into a simple policy: confirm receipt before due date, make the payment path easy on the due date, ask for a payment commitment after the first missed date, involve the account owner before the invoice becomes old, and move repeat offenders into credit review. That approach keeps reminders practical rather than emotional.

Invoice Reminder Statistics FAQ

Common questions

• What is the most common invoice reminder channel? Email is the dominant channel in Chaser’s data, appearing in 93.8% of late-payment follow-up. That does not mean email alone is enough; phone follow-up still appeared in 60% of reminder activity.

• How early should businesses send invoice reminders? The first reminder should usually happen before the due date when the invoice is high value, the customer has a history of late payment, or the business depends on timely cash. U.S. invoices in Xero’s data averaged 9.0 days late, while Canadian invoices averaged 11.6 days late, so waiting until the invoice is old can be costly.

• How common are unpaid invoices for small businesses? QuickBooks reported 56% of surveyed U.S. small businesses owed money from unpaid invoices, and its U.K. report placed the figure at 62%.

• Do invoice reminders really affect cash flow? They can, because reminders influence when money arrives and how much staff time is spent chasing it. QuickBooks connected higher overdue invoice volume with 50% cash-flow problem incidence, while the U.K. Small Business Commissioner estimated 86 hours of annual chasing time per affected business.

• Should reminders include payment links? Payment links can help when friction is the issue, but they do not solve disputes, missing approvals, or customer cash-flow problems. Reminder design should include payment options, invoice details, and a clear path for questions.

• When should a reminder become escalation? Many businesses use the 30-day overdue point as a practical threshold, especially because QuickBooks found 47% of U.S. businesses and 54% of U.K. businesses with some invoices more than 30 days overdue.

• What should businesses measure after changing reminders? The most useful measures are average days late, 30+ day overdue exposure, response rate, dispute rate, payment method after reminder, and chasing hours. Email volume alone is a weak measure because a reminder can be sent without improving cash timing.

Final Takeaway

Invoice reminders are not just messages. They are part of a business’s cash-flow system, customer-relationship system, and AR operating model. The statistics show that late payment is common, unpaid invoices are financially meaningful, regional timing differs, and chasing can consume large amounts of staff time.

The strongest reminder programs do three things at once. First, they prevent avoidable delay by sending accurate invoices, confirming receipt, and making payment easy before the due date. Second, they use selective reminders that match the customer’s history, invoice generator, payment method, and country context. Third, they escalate consistently when the invoice moves from ordinary delay to cash-flow risk.

A business does not need a harsh tone to collect more effectively. It needs a clear cadence, better data, stronger payment paths, and a way to separate customers who forgot, customers who are blocked, customers who are disputing, and customers who are using the business as free financing. When reminders are designed that way, they feel less like chasing and more like disciplined cash management.