B2B payments look simple only when they are reduced to money moving from one company to another. In practice, the payment is the visible end of a longer finance workflow. A buyer may need a purchase order, approval chain, bank-account validation, payment file, and audit trail before money leaves. A supplier may need remittance detail, payment status, invoice history, dispute context, and clean posting before the payment becomes useful. That is why the strongest B2B payment statistics are not only about which method is growing; they show how much operational work still surrounds every rail.

The market is modernizing, but not in a straight line. U.S. B2B payment value is measured in the tens of trillions of dollars, ACH has become a mainstream rail, digital wallets and cards are part of the business environment, and instant-payment readiness is rising. At the same time, checks remain common, fraud attempts are widespread, and integration gaps can make a faster payment feel slow once the accounting work begins.

The best way to read the numbers is as a control map. Checks, ACH, cards, wires, portals, automation, instant payments, and cross-border workflows each solve a different part of the same finance problem. A strong payment strategy does not simply ask which rail is newest. It asks which path gives the business the right mix of speed, safety, cost control, remittance quality, and operational visibility.

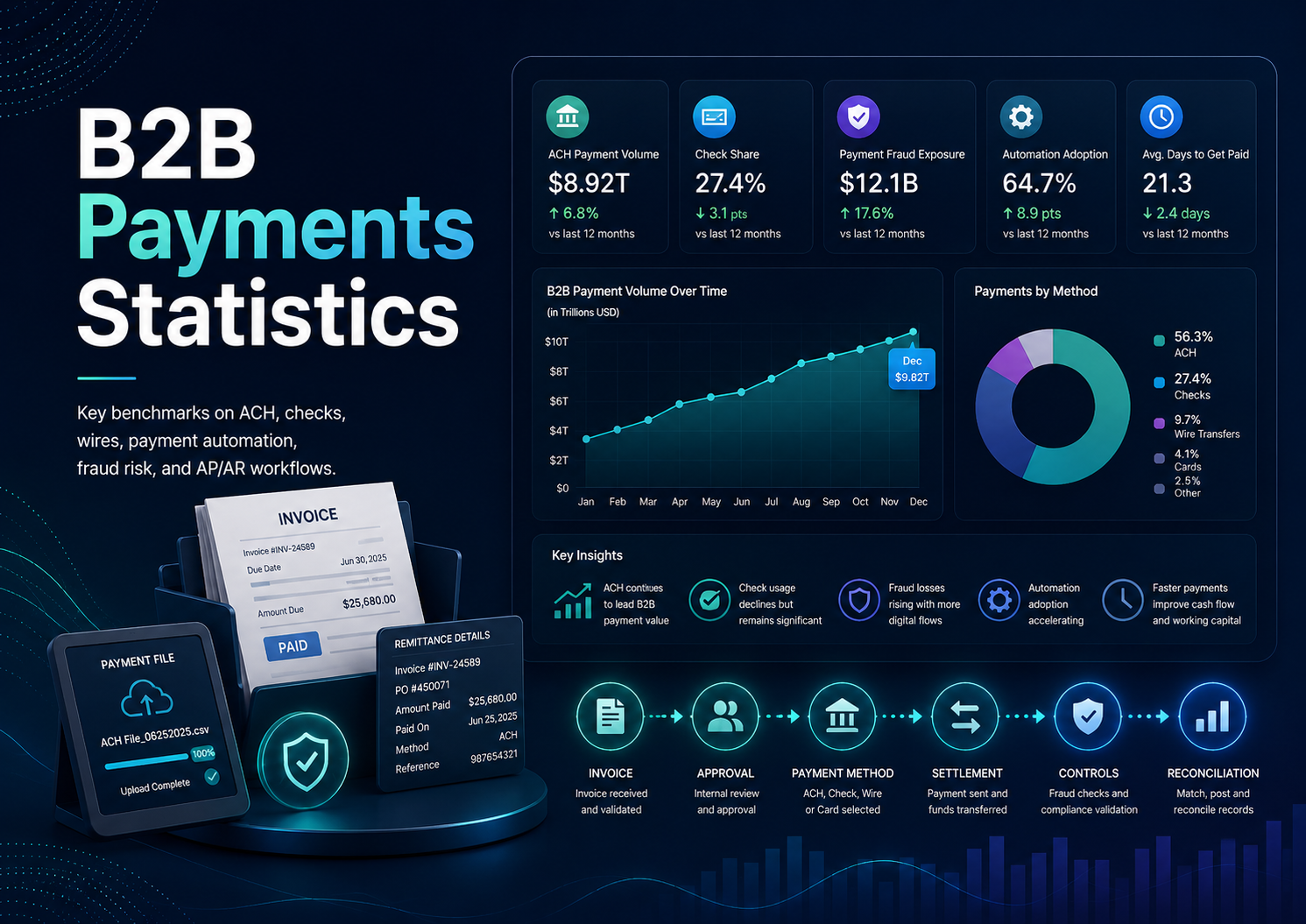

Executive B2B Payment Benchmarks

The headline data shows why B2B payment improvement belongs on the finance and operations agenda, not only inside treasury or accounts payable. Federal Reserve modernization research places U.S. B2B transaction value at $35.8 trillion in 2024, so even small gains in timing, cost, exception handling, or reconciliation can become material when payment volume is this large. The same environment still includes significant legacy behavior: cash and checks represented 32% of U.S. B2B transaction volume in 2024, even as ACH and digital options continued to expand.

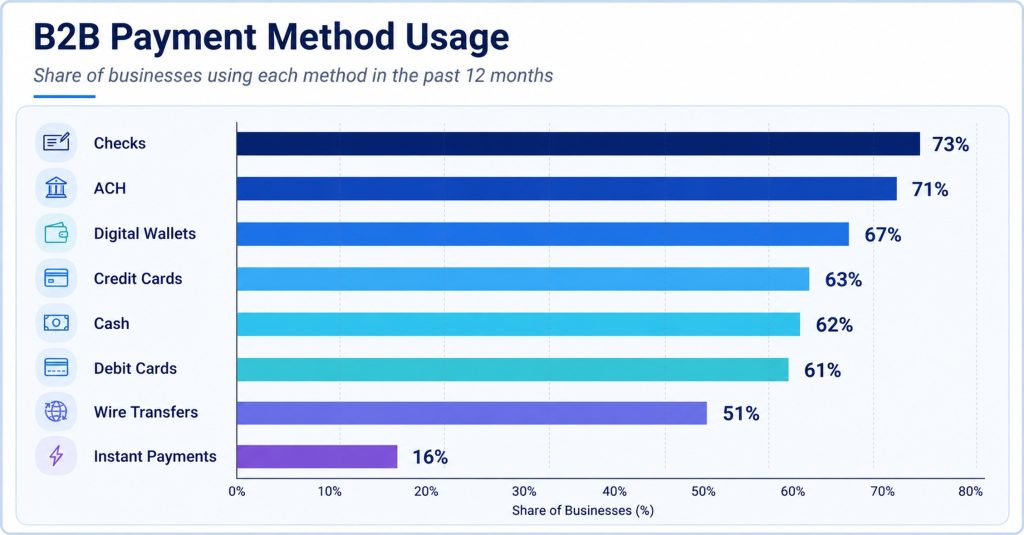

Usage patterns make the transition feel even more mixed. Federal Reserve business-payment data shows checks used by 73% of businesses during the past 12 months, while ACH was nearly as common at 71%. Digital wallets appeared at 67%, credit cards at 63%, cash at 62%, and debit cards at 61%. In other words, B2B payment work is not a single migration from paper to one electronic rail. It is a broad stack of methods that finance teams must manage at the same time.

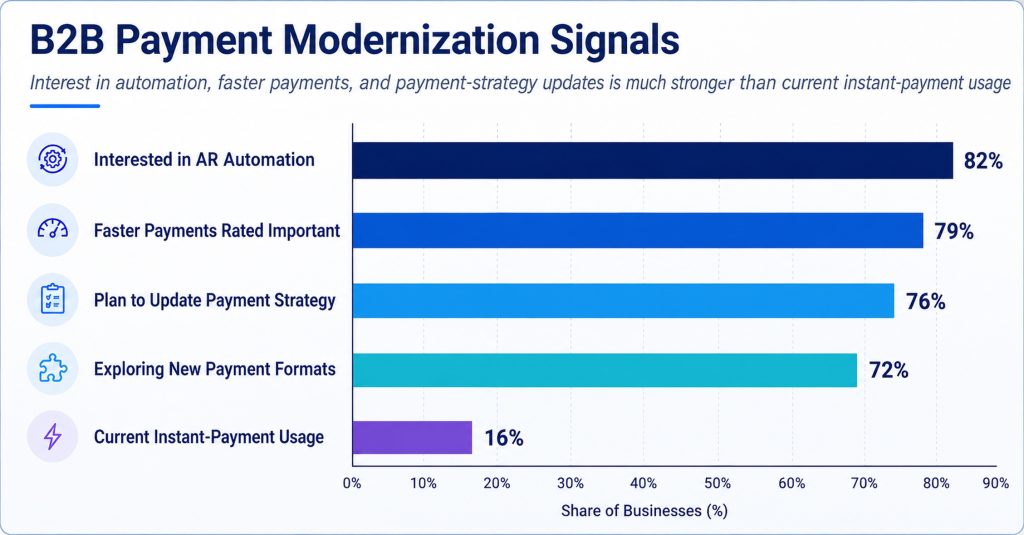

The modernization appetite is also real, but adoption needs guardrails. AFP’s digital payments research found that 76% of organizations planned to update payment strategy within three years, and 72% were exploring new payment formats and channels. Yet the same market still carries major risk and execution pressure. AFP fraud research reported attempted or actual payments fraud at 79% of organizations in 2024, while Federal Reserve business-payment data put high cost and fees at the top of the pain-point list at 48%. The practical conclusion is clear: modernization is not only about paying faster. It is about making payment movement safer, cheaper to operate, easier to reconcile, and easier for counterparties to adopt.

Signals to carry through the payment review

• ACH is already mainstream, with Nacha reporting 8.08 billion B2B ACH payments and $63.11 trillion in B2B ACH value in 2025.

• Checks are declining but still operationally important; AFP data put B2B check share at 26% in 2025, down from 33% in 2022.

• Instant payments are still early in current usage at 16%, but faster or instant payments were rated important by 79% of businesses in Federal Reserve research.

• AR modernization is not only a collection issue; Billtrust/Datos research found 82% interest in AR automation among businesses not already using it, with 75% of interested firms planning adoption within two years.

• The payment problem crosses departments: AP needs safe, timely outbound controls, while AR needs easy collection, complete remittance, and fast posting.

Editorial readout The executive view is deliberately uneven. B2B payments are not moving from old to new in one clean line. They are moving toward connected workflows where the rail, approval process, counterparty data, remittance detail, fraud control, and cash-application process all have to work together.

Why B2B Payments Are Harder Than a Payment Method Swap

Consumer payment improvement often begins with convenience: make the checkout faster, show the right wallet, reduce typing, or improve approval rates. B2B payment improvement begins with context. A payment may be tied to a contract, purchase order, invoice batch, credit term, partial delivery, dispute, or supplier master record. If those surrounding details are incomplete, the payment can move quickly and still create manual work afterward.

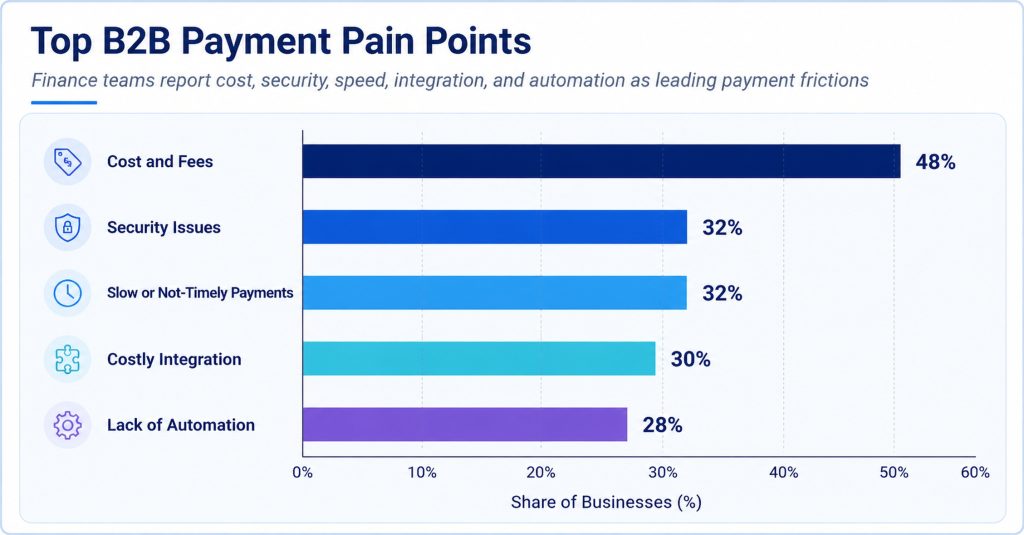

That is why the Federal Reserve pain-point data should be read as a workflow map. Cost and fees led the list at 48%, but security issues and slow or not-timely payments each reached 32%. Integration was close behind at 30%, and lack of automation was selected by 28%. A business that focuses only on the payment fee may miss the staff time lost to exceptions. A business that focuses only on speed may miss the fraud-control risk. A business that focuses only on automation may discover that remittance data is still missing when money arrives.

A practical example is a supplier payment that moves from check to ACH. The ACH payment may settle faster and remove printing, signing, and mailing work. But if the supplier receives one lump-sum deposit without invoice-level detail, the receiving side may spend more time matching cash. The buyer sees progress because the payment left electronically. The supplier sees friction because the information did not travel with the money. The statistic that matters is not only ACH adoption; it is whether payment and remittance improve together.

| Payment issue | What the benchmark suggests | What finance should ask |

|---|---|---|

| Cost and fees | Cost pressure reached 48% in the Federal Reserve pain-point data. | Does the method lower total cost after fees, bank charges, exception handling, and staff time are included? |

| Security | Security concerns reached 32%. | Are account-change controls, approval limits, and employee verification steps strong enough for the chosen rail? |

| Speed | Slow or not-timely payments also reached 32%. | Is the bottleneck the rail, the approval process, the customer, or the posting workflow? |

| Integration | Integration pain reached 30%. | Will payment data connect cleanly with ERP, accounting, portal, and bank systems? |

| Automation | Lack of automation reached 28%. | Which manual steps remain after the payment method changes? |

Planning implication Payment strategy works best when each method is evaluated inside the full workflow. The strongest question is not ‘Which method is fastest?’ but ‘Which method reduces cost, risk, delay, and manual work after the payment is approved, sent, received, and posted?’

How Businesses Actually Pay and Get Paid

The business payment stack is wider than many modernization plans acknowledge. Checks and ACH lead usage, but wallets, cards, cash, debit cards, wires, push-to-card, prepaid debit, money services, and instant payments all appear in the operating environment. That breadth matters because each method solves a different problem and creates a different follow-up workload.

Checks remain common because they fit old approval habits, supplier expectations, and situations where bank information is missing or not trusted. ACH is strong because it supports bank-to-bank movement at scale, especially when counterparties can provide valid account details and enough remittance data. Cards can help with purchasing, subscriptions, travel, and lower-friction supplier payment, but fees and acceptance policy matter. Wires remain important for high-value, urgent, treasury-managed, or cross-border payments. Instant payments are smaller in current use but important for use cases where certainty and timing are more valuable than routine batching.

The payment method mix therefore needs to be segmented. A company can use checks for a legacy supplier group, ACH for recurring vendor bills, cards for purchasing categories, wires for high-value settlement, and portals for customer collections. Treating all of that as one generic payment modernization project usually creates confusion. The better approach is to define the role of each method by transaction value, urgency, fraud sensitivity, data needs, and counterparty preference.

Figure 1. B2B payment usage remains mixed: checks and ACH lead, but wallets, cards, wires, and emerging faster-payment rails are all part of the operating stack.

Payment-method signals that matter most

• Check usage at 73% explains why check reduction must be treated as a migration program, not a quick removal project.

• ACH usage at 71% shows that electronic bank payment is already familiar enough to support broader workflow improvement.

• Digital-wallet usage at 67% suggests business payment habits are widening beyond the older check-card-ACH-wire framework.

• Wire-transfer usage at 51% still matters because high-value and urgent payments often need stronger controls than routine transactions.

• Instant-payment usage at 16% is still early, but readiness and use-case interest point to a larger future role.

Operating interpretation The best payment mix is not the one with the newest method. It is the one that gives each payment type the right balance of cost, certainty, speed, data quality, and control. A modern stack can still include several methods if each one has a clear reason to exist.

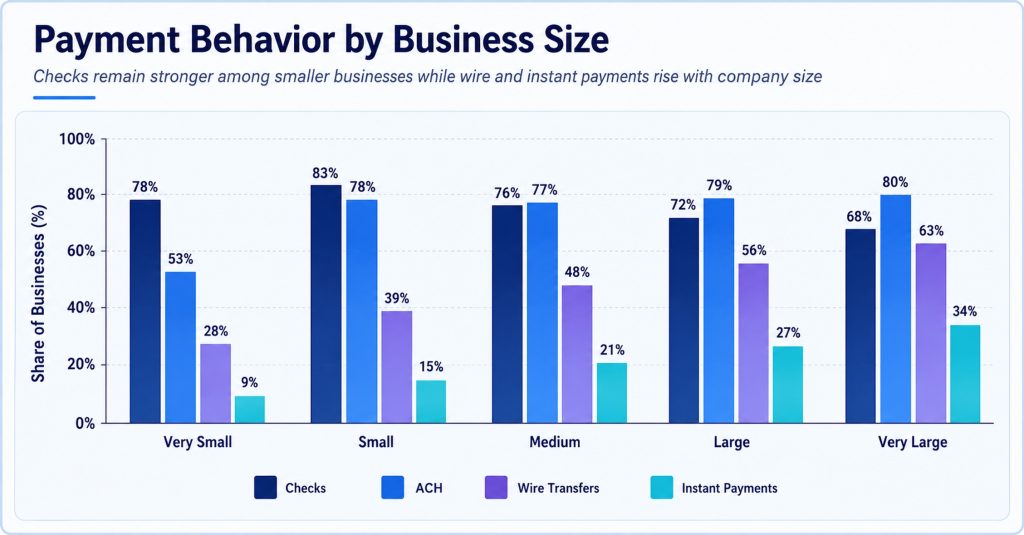

Payment Method Usage Changes by Business Size

How company size changes the payment mix

Business size changes the payment problem. A very small company may want a simple way to collect invoices and pay suppliers without adding banking complexity. A mid-sized company may need stronger approvals, better remittance capture, and cleaner accounting-system integration. A large company may care more about file formats, bank connectivity, role-based controls, counterparty validation, and payment visibility across entities.

The size data reflects those differences. Very small businesses reported check usage at 78%, while small businesses were even higher at 83%. ACH usage rose from 53% among very small businesses to 78% among small businesses, then stayed high across medium, large, and very large organizations. Wire transfers and instant payments became more prominent as business size increased, which makes sense because larger firms tend to manage more urgent, higher-value, and cross-border payment requirements.

This is also where modernization advice needs to be careful. A small supplier asked to move from checks to a portal may experience that change as extra work if the portal is hard to use. A large buyer may see the same portal as a control improvement because it centralizes invoice history, remittance, and approvals. The technology is the same, but the operating context is different.

Figure 2. Payment behavior changes by company size: larger businesses rely more heavily on wires and instant payments, while smaller businesses continue to show strong check usage.

| Business size question | Why it matters |

|---|---|

| Can counterparties onboard easily? | Smaller businesses may resist payment changes if bank-data collection, portals, or file requirements feel too complex. |

| Does the business need stronger treasury controls? | Larger companies often need approval thresholds, user roles, bank connectivity, and audit history. |

| Is remittance complete enough? | ACH or portal adoption helps only when payments can be matched to invoices without extra emails. |

| Is speed actually the bottleneck? | Some firms need faster rails, others need faster approvals, clearer dispute handling, or better posting. |

Size-based lesson A small business and a large enterprise can both say they want better payments, but they usually mean different things. One may need simplicity. The other may need scale, control, and integration. A useful strategy respects both realities.

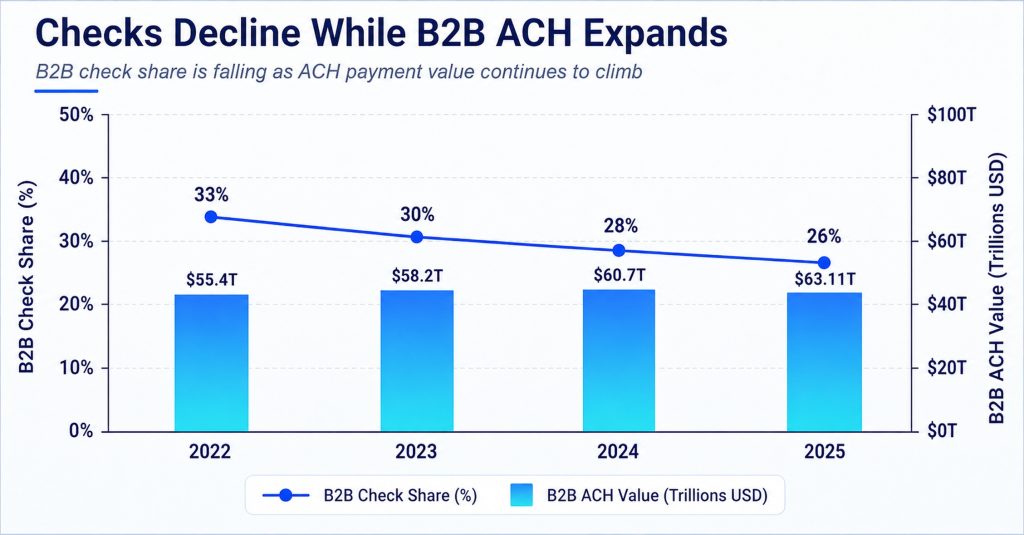

Checks Are Declining, but the Check Problem Is Not Finished

Checks are the clearest symbol of B2B payment transition because the direction is easy to understand: check share is falling, electronic rails are growing, and fraud risk keeps pressure on paper-based processes. AFP’s digital payments data put B2B check share at 26% in 2025, down from 33% in 2022. That 7-point decline shows progress, but it does not mean checks have disappeared from daily finance work.

The persistence of checks is not just habit. Some suppliers request them, some customers still pay that way, some payment files are easier to approve in legacy processes, and some teams lack verified bank details for counterparties. In other cases, checks survive because the business has not built a clean migration path. Removing the check option before fixing account validation, remittance detail, and supplier communication can simply move the friction elsewhere.

Fraud makes the issue more urgent. AFP fraud research reported attempted or actual check fraud at 63% of organizations in 2024, and attempted or actual payments fraud overall at 79%. Yet many organizations still had no plan to reduce check usage within two years. That gap between risk awareness and operating change is why check reduction has to be managed with ownership, not only with a policy statement.

Figure 3. Check share is falling while B2B ACH volume keeps rising, but the transition is gradual rather than complete.

A better way to frame check reduction

• Start with trusted counterparties where bank-account details are already verified and remittance behavior is clean.

• Move recurring, predictable payments before high-risk or exception-heavy payments.

• Separate checks used by preference from checks used because the company lacks better onboarding data.

• Measure fraud exposure, staff handling time, postage and printing cost, and reconciliation delay together rather than treating check cost as only a bank-fee issue.

Check-reduction principle The strongest check-reduction programs do not try to force every counterparty into the same channel immediately. They begin with the safest, cleanest segments, prove that the new process works, and then expand with better communication, validation, and support.

Why ACH scale still depends on data quality

ACH Is the Workhorse, but Remittance Still Decides the Experience

ACH is one of the most important bridges between traditional B2B payment behavior and modern workflow improvement. Nacha reported 8.08 billion B2B ACH payments in 2025 and $63.11 trillion in B2B ACH value. That scale makes ACH impossible to treat as a niche alternative. It is already a central bank-payment rail for businesses that want predictable electronic movement without relying on paper checks.

The operational benefit, however, depends heavily on the information that travels with the payment. A clean ACH payment with invoice-level remittance can shorten collection work and make cash application easier. A lump-sum ACH deposit with missing details can create a new kind of manual work. The payment has arrived, but the AR team still has to identify which invoices it closes, whether discounts were taken correctly, and whether a short payment reflects a dispute or a mistake.

This is where AP and AR goals overlap. AP may want ACH because it can reduce check handling and create a repeatable outbound payment process. AR may want ACH because it can bring customer money in faster and more predictably. Both sides still need complete remittance, clear status, and strong account controls. Without that, the business improves the movement of funds but not necessarily the quality of the finance process.

| ACH advantage | Where the benefit can break down |

|---|---|

| Bank-to-bank scale | ACH is broadly used, but onboarding stalls if counterparties hesitate to share or update account details. |

| Lower paper handling | Check handling can fall, but staff may still chase missing invoice references. |

| Recurring payment fit | Predictable bills work well, but disputes and partial payments still need clear exception handling. |

| Faster posting potential | Cash application improves only when remittance is complete enough for accounting records. |

ACH interpretation ACH growth is meaningful because it changes the default payment path for many B2B relationships. The next improvement layer is data quality: invoice references, remittance files, account validation, and posting logic need to mature alongside the rail.

The pain points behind payment modernization

Cost, Security, Speed, Integration, and Automation Pull in Different Directions

B2B payment decisions often involve tradeoffs. A method can be fast but expensive, secure but difficult to onboard, familiar but risky, or efficient only when the data around it is complete. That is why the pain-point data should not be read as a simple ranking. It is a reminder that payment strategy has several competing owners: treasury cares about cost and liquidity, AP cares about controls and approvals, AR cares about collection and posting, IT cares about integration, and risk teams care about fraud exposure.

Cost and fees led the Federal Reserve pain-point data at 48%, but the next problems were close enough to matter. Security issues and slow or not-timely payments each reached 32%, costly integration was selected by 30%, and lack of automation reached 28%. These numbers are more useful when they are linked to operating decisions. A company reviewing card acceptance should consider customer convenience and collection speed, but also fees and chargeback exposure. A company reviewing wires should consider urgency and certainty, but also beneficiary verification. A company reviewing portals should consider customer experience, but also whether portal data reaches the ERP cleanly.

The management mistake is to assign each issue to a different project without one shared scorecard. A fee-reduction project may choose the lowest-cost rail and accidentally increase exceptions. A speed project may push faster settlement before account-validation controls are ready. An automation project may add a portal while leaving old email-based dispute work unchanged. The benchmark data argues for a more connected payment review.

Controls must move before volume moves

Figure 4. B2B payment pain points are clustered around cost, risk, speed, integration, and automation rather than one isolated problem.

Management takeaway A payment method should be judged through a full-cost lens. Transaction fees matter, but so do exceptions, fraud controls, staff time, status questions, missing remittance, bank-account maintenance, failed payments, disputes, and customer or supplier experience.

Fraud Risk Has Become a Modernization Requirement

Fraud risk is one reason payment teams can be cautious about change. The caution is justified. B2B fraud often targets process weakness rather than the payment rail alone: a fake account-change request, a compromised vendor email, a manipulated approval chain, a check intercepted in transit, or a rushed wire instruction. A faster payment method can help the business only if the control environment is ready for it.

The fraud data makes controls part of modernization, not a separate compliance topic. Attempted or actual payments fraud affected 79% of organizations in AFP research, while check fraud appeared at 63%. Federal Reserve payment data also put security issues at 32% as a business pain point. These figures explain why finance teams cannot evaluate speed without asking how account details are verified, who can approve payment changes, how exceptions are reviewed, and whether employees are trained to spot social-engineering attempts.

Visibility is the real AR automation gain

The strongest modernization programs treat fraud prevention as workflow design. Vendor master updates receive stricter verification than routine invoice approvals. Bank-detail changes require callback or secure confirmation. Payment files have user roles and thresholds. Wires and instant payments receive additional review because reversibility may be limited. Employees are trained to recognize instructions that arrive with urgency, secrecy, or unexpected account changes. That kind of control design lets companies modernize without turning payment speed into payment vulnerability.

| Risk area | Why it matters in modernization |

|---|---|

| Account-change requests | Electronic payment adoption often requires bank-account collection and updates, which fraudsters can imitate. |

| Checks in transit | Paper-based processes remain exposed to theft, alteration, and mail risk. |

| Business email compromise | BEC can manipulate trusted relationships, making approval discipline as important as payment method. |

| Wires and instant payments | Speed and finality can raise the stakes when beneficiary data is wrong or fraudulent. |

| Vendor master data | Payment safety depends on who can create, update, approve, and review counterparty records. |

Control implication Fraud control should be designed into payment modernization from the beginning. A company moving from checks to ACH, portals, cards, wires, or instant payments should strengthen account validation, change management, approvals, audit trails, and employee training before volume moves.

AR Automation and Customer Payment Portals Are About Visibility, Not Only Collection

Accounts receivable modernization is often described as a faster way to collect money. That is true, but incomplete. For many finance teams, the larger benefit is visibility. A useful portal or AR automation workflow helps customers see what they owe, understand invoice history, attach remittance detail, resolve disputes, select approved payment methods, and confirm status without starting another email thread.

Interest in AR automation reflects that broader need. Billtrust/Datos research found that 82% of businesses not already using AR automation were interested in adopting it, and 75% of interested businesses planned adoption within two years. Those figures do not mean every implementation will succeed. They show demand for cleaner workflows, especially in areas where manual follow-up, missing remittance, and unclear payment status consume staff time.

The strongest AR teams measure whether automation reduces work after the customer pays. A portal that accepts money but leaves short payments unexplained can still create unapplied cash. A payment button that speeds collection but fails to pass invoice references can still create posting delays. A reminder workflow that sends more emails without improving dispute resolution can increase noise. AR automation works best when the customer experience, payment path, remittance data, and accounting record are designed together.

| AR improvement | What to measure after rollout |

|---|---|

| Customer payment portal | Portal adoption, payment completion, support emails, and customer payment-status questions. |

| Automated reminders | Promise-to-pay rate, dispute response, repeat late payers, and collection workload. |

| Remittance capture | Unapplied cash, short-payment explanations, invoice matching, and posting delay. |

| ERP integration | How quickly payment status, credits, disputes, and receipts reach accounting records. |

AR lesson A portal should not be judged only by whether customers can pay through it. It should also reduce payment-status emails, missing invoice requests, unapplied cash, dispute confusion, and manual posting work.

AP and AR Need Connected but Different Payment Strategies

One of the weakest ways to write a B2B payment strategy is to treat AP and AR as if they need the same thing. They are connected, but not identical. AP needs safe, approved, timely outbound movement. AR needs easy collection, complete information, and fast posting. Treasury needs liquidity visibility. Accounting needs clean records. Risk teams need controls. A strong plan recognizes those differences and then connects them through shared data and governance.

Speed matters most when timing changes the outcome

This is where the method benchmarks become more useful when they are placed inside a realistic finance workflow. Check usage at 73% matters because AP teams still manage printing, mailing, signing, tracking, and fraud controls in many environments. ACH usage at 71% matters because AR teams can collect electronically only when the remittance data is good enough to apply cash. The 48% cost-and-fee pain point may mean bank charges to treasury, card costs to AR, supplier payment fees to AP, or portal costs to operations. The 32% security concern may appear as vendor bank-account risk, customer account-change risk, or employee approval risk.

A practical example is a mid-sized distributor. AP wants to move suppliers from checks to ACH to reduce handling and fraud exposure. AR wants customers to pay electronically through a portal so cash posts faster. IT wants fewer disconnected files. Sales wants customers to have payment flexibility. None of those goals is wrong. The strategy fails only if each team improves its own workflow while pushing new exceptions onto another team.

| Team | Primary payment question | Useful benchmark connection |

|---|---|---|

| AP | Can the business pay safely, on time, and with the right approvals? | Check usage remains high enough that outbound payment controls still matter. |

| AR | Can customers pay easily with enough remittance detail to post cash? | ACH and portal adoption help only when invoice references and status data are clear. |

| Treasury | Can payment timing, liquidity, and bank exposure be forecast reliably? | Payment speed matters, but so do cutoff times, bank choice, and visibility. |

| Risk / controls | Can account changes, approvals, and fraud attempts be verified? | Fraud exposure makes governance part of modernization rather than an afterthought. |

| IT / systems | Can payment data move between banks, ERP, portals, and reporting tools? | Integration pain at 30% shows why systems ownership is part of payment strategy. |

Connected strategy rule AP and AR do not need identical workflows, but they do need compatible data. A payment strategy becomes practical when outbound safety, inbound collection, remittance quality, system integration, and fraud controls are designed as one finance operating model.

Faster and Instant Payments Are a Use-Case Decision

Instant-payment adoption is still early, but the interest signals are much stronger than the current usage number alone. Federal Reserve data showed instant-payment usage at 16%, while 79% of businesses said faster or instant payments were important. The same research found that 85% of businesses said they would be ready for faster or instant payments within three years. That gap between current use and expected readiness is the real story.

The best way to interpret faster payments is by use case. A routine supplier invoice does not always need instant settlement if the approval process takes days and the supplier is paid on terms. An urgent supplier payment, payroll exception, merchant settlement, insurance disbursement, or request-for-payment workflow may benefit more clearly. The question is not whether faster is always better. The question is where payment certainty and timing improve the business outcome enough to justify the operational change.

Cross-border payment risk is a data problem too

The use-case data supports that view. In Federal Reserve business-payment research, 34% selected B2B recurring bills and invoices as a faster-payment use case, while 29% selected B2B just-in-time payments. Payroll reached 35% among B2P use cases. These are not abstract preferences. They point to real payment moments where timing, certainty, and communication matter.

Figure 5. Faster-payment interest is strongest when businesses connect speed to concrete use cases such as recurring bills, just-in-time payments, and payroll.

| Use case | Why faster payment may help |

|---|---|

| Recurring bills and invoices | Payment timing can become more predictable when approval and request-for-payment workflows are clean. |

| Just-in-time supplier payment | Faster settlement can protect supply relationships when timing is operationally important. |

| Payroll or earned wage exceptions | Speed matters when the recipient experience depends on immediate availability. |

| Merchant settlement | Faster funding can improve liquidity for businesses with frequent sales volume. |

| Large disbursements | Certainty and communication may matter as much as speed because payment errors can be expensive. |

Faster-payment rule Faster payment should be connected to a use case, not adopted as a slogan. When speed reduces uncertainty, protects a relationship, or improves cash timing, it can be valuable. When the bottleneck is approval, data, or reconciliation, the rail alone is not enough.

Cross-Border B2B Payments Add Time, Cost, and Visibility Problems

Cross-border B2B payments expose the same issues as domestic payments, but with more variables. Currency conversion, intermediary banks, sanctions screening, beneficiary details, cut-off times, local banking rules, invoice currency, and documentation can all affect the payment experience. When something goes wrong, the problem is often harder to trace because more parties are involved.

The payment method choice matters here, but so does communication. A supplier may care less about the label on the rail and more about whether funds arrive on the expected date, in the expected currency, with enough detail to match the invoice. A buyer may care about fees, exchange-rate transparency, approval controls, and whether payment status is visible before the supplier starts asking for updates.

For many companies, the most practical cross-border improvement is not a single new payment method. It is a clearer operating model: approved currencies, validated beneficiary data, documented fee responsibility, standard remittance requirements, and reporting that shows where payments are stuck. Those controls reduce confusion even when the underlying payment path still varies by country or bank.

| Cross-border friction | Operational response |

|---|---|

| Unclear fees | Define whether fees are sender-paid, shared, or receiver-paid before the payment is sent. |

| Currency mismatch | Align invoice currency, payment currency, and exchange-rate expectations. |

| Beneficiary-data errors | Validate bank identifiers and account details before high-value payments are released. |

| Limited status visibility | Use payment tracking or bank confirmations where available for supplier-sensitive payments. |

| Remittance gaps | Send invoice references and supporting documents through a channel the supplier can actually use. |

Cross-border interpretation International payment improvement is rarely only about speed. It is about predictability: who pays the fees, which currency is used, when funds should arrive, what information travels with the payment, and how both sides confirm status when something is delayed.

A scorecard for payment outcomes, not only payment methods

Governance Turns Payment Modernization Into an Operating System

Payment governance is where the benchmark data becomes operating ownership. It is not enough to know that cost, security, speed, integration, and automation appear as payment pain points; the business also needs owners for each recurring decision. Payment governance should define who can add or change counterparty bank details, who approves exceptions, who measures fees, who owns remittance standards, who resolves disputes, and who decides when a method should be retired.

The benchmark data supports governance because the problems are spread across teams. Cost pressure at 48% may involve treasury, AP, AR, procurement, banking partners, card processors, and customer policy. Security concerns at 32% require finance and IT to work together. Integration pain at 30% makes system ownership part of payment strategy. Lack of automation at 28% should push leaders to measure staff time and exception volume, not only method adoption. AFP’s finding that 76% of organizations planned payment-strategy updates suggests many businesses are already planning change, but planning only helps when ownership and implementation are clear.

A governance model also prevents modernization from becoming tool-first. A company may adopt a portal, add ACH, introduce virtual cards, or explore instant payments. If no one owns data quality, customer adoption, supplier communication, fraud-control updates, and exception reporting, the new method can simply create a new place for old problems to hide.

| Governance question | Why it should be answered before rollout |

|---|---|

| Who owns payment-method policy? | Without ownership, teams may add methods without deciding when each one should be used. |

| Who owns counterparty data? | Bank details, customer records, supplier master data, and account changes affect fraud risk and payment accuracy. |

| Who owns remittance rules? | Payments that arrive without invoice references can create manual cash-application work even if the rail is electronic. |

| Who owns exception reporting? | Short pays, duplicate payments, disputes, and failed payments need a visible owner and recurring review. |

| Who owns adoption communication? | Customers and suppliers need clear instructions, not just access to a new tool. |

Governance takeaway B2B payment modernization becomes sustainable when it has owners, metrics, and review cycles. Without governance, a business may modernize the payment option while leaving the old approval, data, and exception problems unchanged.

Metrics Finance and Operations Leaders Should Track

A useful B2B payment scorecard has to look beyond method adoption. A company can increase ACH usage and still have poor remittance. It can lower check volume and still have high fraud exposure through account-change requests. It can add a portal and still see customers email for invoice copies. It can process payments faster while cash application remains slow. The scorecard should show whether the full workflow improved, not only whether a new rail was used.

The strongest metrics connect payment behavior to business outcomes. Finance teams should review method mix, days sales outstanding, days payable outstanding, payment cost by method, exception rate, remittance completeness, unapplied cash, failed payments, fraud attempts, supplier adoption, customer portal usage, and settlement timing. The goal is not a large dashboard for its own sake. The goal is to identify where money, data, and work are getting stuck.

| Metric | Why it matters |

|---|---|

| Payment-method mix | Shows which rails actually carry volume and which are used only for special cases. |

| Days sales outstanding | Connects customer payment behavior to cash-flow timing. |

| Days payables outstanding | Shows how outbound payment timing affects supplier relationships and working capital. |

| Cost by method | Combines transaction fees, bank charges, staff time, exceptions, and support work. |

| Remittance completeness | Shows whether payments arrive with enough data to close invoices cleanly. |

| Unapplied cash | Measures how much received money still requires manual matching. |

| Fraud attempts and losses | Keeps risk visible as payment speed and digital adoption increase. |

| Exception rate | Reveals where short pays, disputes, duplicate payments, or missing data create work. |

| Portal or automation usage | Shows whether new tools reduce email, calls, and manual follow-up. |

Scorecard principle The right metrics help teams see the payment lifecycle from start to finish. A payment is not fully successful when money moves. It is successful when it is approved safely, received predictably, matched accurately, posted cleanly, and understood by both sides.

Where B2B Payment Modernization Usually Breaks Down

Many B2B payment projects do not fail because the payment rail is weak. They fail because the surrounding workflow is not ready. A buyer may be willing to pay by ACH but unable to send useful remittance. A supplier may accept a portal but still email for invoice copies. A treasury team may approve instant payments but lack account-validation rules. A controller may want automation but still depend on manual posting because ERP integration is incomplete.

The most common breakdown is treating adoption as the finish line. A payment method is not truly adopted if customers avoid it, suppliers misunderstand it, staff build workarounds, or accounting records still require manual repair. Adoption should be measured by completed workflows: payment released, remittance sent, funds received, invoice matched, exception resolved, and status visible.

This is why pilot design matters. A business should not start with the most difficult counterparty group unless the purpose is stress testing. It can begin with a clean segment, prove the workflow, identify edge cases, and then expand. That approach creates learning without forcing every customer or supplier into a process that is not ready.

Common failure patterns

How the same statistics change by business model

• ACH is available, but customers send lump-sum payments without invoice-level detail.

• A portal is launched, but customer service still receives payment-status emails because invoice history is incomplete.

• Virtual card acceptance improves payment timing for some suppliers, but fees make others resist the program.

• Check reduction is announced before supplier bank data is validated and securely maintained.

• Instant-payment readiness is discussed before approval thresholds and fraud controls are updated.

• Cross-border payment tools are added without clarifying currency, fee, and beneficiary-data rules.

Practical B2B Payment Scenarios

The clearest way to make B2B payment statistics feel practical is to place them inside common operating situations. A wholesaler, a SaaS vendor, a manufacturer, and a professional-services firm may all say they want better payments, but they do not experience the same problem. The wholesaler may be chasing remittance detail from many customers. The SaaS vendor may want customers on ACH or cards to reduce collection effort. The manufacturer may be balancing supplier payment timing against working capital. The services firm may need clearer invoice status because clients approve work in stages.

Consider a regional wholesaler that collects from hundreds of retailers. Moving more customers to ACH may improve cash timing, but the bigger benefit arrives when customers include invoice references consistently. Without that detail, a single payment can cover several invoices, credits, shortages, and disputed line items. The cash is in the bank, but the AR team still has to spend time applying it. In that setting, the ACH adoption statistic is useful only when paired with remittance completeness and unapplied cash metrics.

A SaaS company may face a different version of the same issue. Card payments can be convenient for smaller subscriptions, but card fees become more visible as invoice values rise. ACH can improve payment economics for larger customers, yet onboarding must be simple enough that customers do not delay the switch. If the business also has customers who still pay by check, the migration plan should be based on account size, payment reliability, support effort, and customer readiness rather than a universal policy deadline.

A manufacturer may care most about supplier continuity. It may use ACH for predictable supplier payments, wires for urgent international purchases, and checks for legacy suppliers that have not moved. The payment method decision is tied to supply risk. Paying a critical supplier late can create operational problems that are much larger than the transaction fee. In this case, the statistic about faster-payment importance matters because it points to use cases where timing protects production, not because every supplier needs instant settlement.

A professional-services firm may need a simpler client payment experience more than a complex treasury stack. Its invoices may be project-based, milestone-based, or retainer-based. If clients approve invoices slowly, the firm may benefit from clearer invoice history, online payment links, recurring payment options, and reminders that explain what is due. Here the AR automation benchmarks become more meaningful than generic payment-method adoption. The business is not only collecting money; it is reducing the amount of follow-up required after work has already been delivered.

| Business scenario | Most useful payment focus | Metric to watch |

|---|---|---|

| Wholesaler collecting from many buyers | ACH and portal payments with complete remittance detail | Unapplied cash, invoice-match rate, and dispute volume. |

| SaaS vendor billing recurring accounts | Customer segmentation by ACH, card, and check migration readiness | Payment cost by account size and failed-payment recovery. |

| Manufacturer managing suppliers | Safe outbound controls for ACH, wires, and urgent payments | Supplier payment timing, approval delay, and account-change exceptions. |

| Professional-services firm billing milestones | Client-friendly invoice status, payment links, and reminders | DSO, promise-to-pay response, and follow-up workload. |

Scenario lesson The payment method is only one part of the answer. The same benchmark can mean different things in different businesses, so the numbers should always be connected to the workflow the reader is trying to improve.

How to Choose the Right Payment Path

A practical payment decision model starts with the transaction, not the technology. Before choosing ACH, card, wire, instant payment, portal payment, or check migration, a business should ask what the payment is trying to accomplish. Is the priority low cost, certainty, speed, supplier satisfaction, customer convenience, fraud control, or clean reconciliation? A single method rarely wins on every dimension.

For routine supplier payments, ACH may be the default path when bank details are verified and the payment can be batched safely. For urgent or high-value supplier obligations, wires or faster-payment options may be appropriate, but only with stronger beneficiary verification. For customer collections, portals and payment links may be more important than the rail because the customer needs clarity on invoice history, available methods, credits, and disputes. For smaller business purchases, cards may be useful because they add convenience, controls, and reporting, even if fees must be managed carefully.

The decision model keeps the numbers practical. A high usage number shows familiarity, not always superiority. A low usage number can still identify a high-value use case. A pain-point number shows friction, but the response depends on where the friction appears. Cost can be a fee problem, a labor problem, a failed-payment problem, or a support problem. Security can mean check fraud, account-change fraud, user permissions, or approval weakness. Integration can mean ERP files, bank feeds, portal data, remittance capture, or reporting. The right payment path is the one that solves the specific operating problem without creating a larger downstream issue.

| Decision factor | What to consider |

|---|---|

| Payment value | High-value payments often need stronger approval, beneficiary verification, and audit history. |

| Urgency | Faster rails are most useful when timing changes the business outcome. |

| Counterparty readiness | A method works only when the customer or supplier can use it without creating side work. |

| Remittance need | Invoice-heavy payments need data quality, not only settlement. |

| Fraud exposure | Account changes, wires, checks, and urgent payments need different control levels. |

| System fit | The payment path should connect to ERP, bank, portal, and reconciliation workflows. |

Decision rule Payment modernization should not force every transaction through the newest method. It should route each payment through the method that best fits value, urgency, data needs, counterparty readiness, fraud risk, and system fit.

Communication and Counterparty Adoption Matter as Much as the Rail

A payment method can be technically available and still fail in practice if customers or suppliers do not understand the change. B2B payment adoption is a relationship problem as much as a technology problem. A supplier may ignore an ACH enrollment request if it looks risky, asks for too much information, or arrives without a familiar contact. A customer may avoid a portal if the login process is unclear, the invoice list is incomplete, or the payment method they prefer is not visible. Those small points of friction can slow adoption even when the underlying method is objectively better.

This is why communication should be part of the payment strategy, not a one-time announcement at the end. Counterparties need to know what is changing, why the change is being made, which payment options remain available, how bank information is protected, what remittance detail is required, and where to get help. Internal teams need the same clarity. Sales should know how payment changes affect customers. Procurement should know how supplier onboarding will work. Customer support should know what to say when a buyer cannot find an invoice or payment confirmation.

The statistics about payment-strategy updates, AR automation interest, check persistence, and security concerns all point back to this adoption problem. A company may plan to update payment strategy, but the plan succeeds only if people use the new workflow correctly. Security concerns are easier to manage when counterparties understand verified enrollment channels. AR automation is more valuable when customers know where to find invoices, credits, statements, and receipts. Check reduction becomes more realistic when suppliers receive clear instructions and a secure way to provide bank details.

A strong rollout also separates messages by audience. High-volume customers may need direct outreach, testing, and remittance-format guidance. Long-tail customers may need simpler portal instructions and reminders. Strategic suppliers may need an onboarding call before payment terms change. Internal approvers may need a shorter policy guide that explains which payments can use ACH, card, wire, instant payment, or check exception. That level of communication may seem less exciting than the payment technology itself, but it is often what turns a payment option into an adopted process.

| Audience | Adoption message that matters |

|---|---|

| Customers | Where to find open invoices, how to pay, how to send remittance, and how payment status is confirmed. |

| Suppliers | How bank details are collected safely, when payment timing changes, and which contacts are authorized. |

| AP staff | Which payment method to use by supplier type, payment value, urgency, and risk level. |

| AR staff | How to handle portal questions, short payments, remittance gaps, and customer payment disputes. |

| IT and controls | Which systems own payment data, account changes, audit logs, and exception reporting. |

Adoption lesson Payment modernization works better when it is treated as a behavior change. Clear instructions, verified channels, role-based training, and counterparty support can matter as much as the payment method selected.

90-Day B2B Payment Improvement Plan

B2B payment statistics become more useful when they turn into a short operating plan. A company does not need to solve every payment problem at once. It needs to identify the largest sources of delay, cost, risk, and manual work, then choose the payment changes that remove the most friction first.

The plan should begin with evidence rather than a vendor demo. Which customers pay late? Which suppliers still require checks? Which payment types create missing remittance? Which bank-account changes create risk? Which methods cost more after staff time is included? Which invoices remain open even after money arrives? Those questions help the business prioritize the workflow, not just the rail.

| Timing | What to do | Output |

|---|---|---|

| Days 1-30 | Build the baseline by method, customer or supplier segment, invoice size, approval path, remittance quality, fraud exposure, and exception volume. | A clear map of where money slows down and where staff time is being consumed. |

| Days 31-60 | Target high-confidence fixes such as ACH onboarding, check-reduction candidates, portal cleanup, account-validation controls, or remittance requirements. | A short list of controlled improvements with owners, expected benefit, and success metrics. |

| Days 61-90 | Review adoption, settlement timing, exception reduction, fraud-control quality, customer or supplier response, and cash-application improvement. | A repeatable payment scorecard that distinguishes faster settlement from better operations. |

Planning principle A strong 90-day review separates payment movement from payment success. The business should know whether a change improved cost, speed, security, remittance, adoption, and posting quality before it expands the rollout.

B2B Payments Statistics FAQ

What is the biggest B2B payment trend?

The biggest trend is gradual modernization rather than instant replacement. Checks are declining, ACH is scaling, digital and card options are common, and faster-payment readiness is rising, but businesses still need better remittance, controls, and integration.

Are checks still common in B2B payments?

Yes. AFP data shows B2B check share falling from 33% in 2022 to 26% in 2025, but Federal Reserve business-payment data still shows check usage among businesses at 73% during the past 12 months.

How large is B2B ACH?

Nacha reported B2B ACH volume of 8.08 billion payments in 2025, with B2B ACH value reaching $63.11 trillion.

Why are B2B payments harder than consumer payments?

B2B payments often involve invoices, approvals, purchase orders, remittance data, ERP posting, supplier verification, credit terms, and fraud controls. The payment itself is only one part of the workflow.

What payment pain point matters most?

Cost and fees led the Federal Reserve business-payment pain-point list at 48%, but security, speed, integration, and automation were also major concerns.

How important are faster payments for B2B?

Current instant-payment usage was 16% in the Federal Reserve business data, but 79% of businesses said faster or instant payments were important and 85% said they would be ready within three years.

What should companies measure first?

A strong starting point is payment-method mix, DSO, DPO, cost by method, reconciliation exceptions, remittance completeness, fraud attempts, counterparty adoption, and portal or automation usage.

Final Takeaway

B2B payments are changing, but the transition remains uneven. Checks are declining, ACH is growing, digital wallets and cards are common, wires remain important, instant-payment readiness is rising, and automation interest is strong. At the same time, cost, security, integration, fraud, remittance quality, and manual work still determine whether a company actually improves its payment operation.

The most useful B2B payment strategy begins with visibility, not a mandate to use one method everywhere. Finance and operations leaders need to know which customers or suppliers create delays, which methods are expensive after staff time is included, which payments create exceptions, which counterparties are ready to move, and which controls must be strengthened before speed increases.

That visibility should also be reviewed regularly, not only during a software selection project. Payment behavior changes when customers grow, suppliers update banking details, international activity expands, fraud tactics shift, or accounting systems are replaced. A method that worked well for one segment last year may become expensive, risky, or difficult to reconcile as volume changes.

Companies modernizing B2B payments are focusing on systems that deliver speed where fast transactions are critical, stronger security where financial risk is higher, and simplified reconciliation where invoice volumes continue to grow. Businesses also need flexible solutions that can adapt to different supplier and customer relationships without creating additional operational complexity. Alongside digital payment tools, using a well-structured cash receipt template helps companies maintain accurate transaction records and improve financial transparency after payments are completed. The real challenge is not simply adopting modern payment methods, but creating a workflow that reduces friction, improves documentation, and supports smoother finance operations long after the transaction has been processed.

The businesses that make the most progress usually avoid one-size-fits-all mandates. They identify where checks are still justified, where ACH can replace manual handling, where cards or portals improve customer experience, where wires or faster payments protect high-value relationships, and where automation can remove repetitive follow-up. Then they review the result with evidence: fewer exceptions, cleaner remittance, lower fraud exposure, better adoption, fewer avoidable emails, faster dispute resolution, and less time spent explaining where the money went. At that level, B2B payment statistics stop being a list of numbers and become a practical map for better finance operations, cleaner customer relationships, and safer supplier payment routines.