Invoice payment is the point where a completed job, delivered order, or approved service becomes usable cash. A company can send a correct invoice and still wait weeks for money if the buyer’s approval path is slow, the due date is generous, the payment method is inconvenient, the remittance detail is incomplete, or a dispute sits unresolved in someone’s inbox. That makes invoice payment a working-capital system, not only an accounts receivable task.

The strongest invoice-payment statistics show that the issue is both common and operational. QuickBooks found that 56% of surveyed U.S. small businesses were owed money from unpaid invoices, and those affected were owed about $17,500 on average. Xero’s five-country invoice data shows that small businesses still wait roughly 24 to 30 days for invoices to be paid, depending on the market, and that the payment often arrives days after the due date. Billtrust’s benchmark data points to the other side of the story: stronger eDelivery, touchless payment, and cash-application performance can shorten the distance between invoice issue and usable cash.

Invoice payment works best when it is managed as a full invoice-to-cash journey. Payment timing, overdue balances, trade credit, payment methods, AR automation, disputes, portals, regional differences, cash application, and follow-up practices all shape how quickly billed work becomes usable cash. The numbers help business owners, controllers, AR leaders, and finance teams decide where cash is being delayed and what kind of fix is most likely to work.

Executive Invoice Payment Benchmarks

The headline numbers define the invoice-payment problem. They show why invoice payment should be managed as a measurable process after the invoice is sent, not as a vague waiting period between billing and collections. The most useful benchmarks separate four questions: how much money is unpaid, how late invoices are, which payment paths help money move, and how much manual work remains after the payment arrives.

The Numbers That Define The Invoice-To-Cash Gap

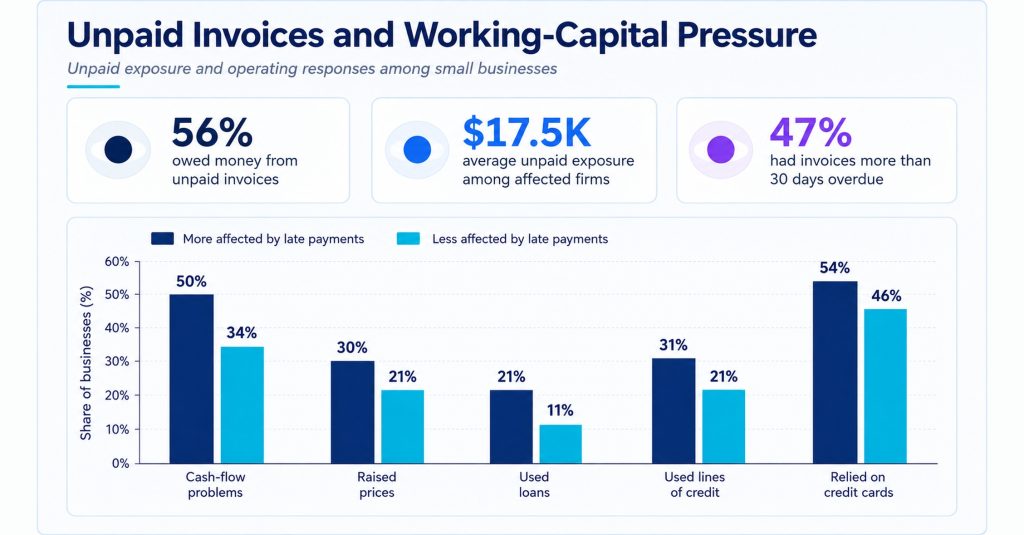

· QuickBooks’ late-payment research shows the scale of unpaid receivables, with 56% of surveyed U.S. small businesses reporting money owed from unpaid invoices and an average unpaid exposure of about $17,500 among affected firms.

· Overdue invoices are not limited to a few outlier customers; the same research found that 47% of U.S. small businesses had some invoices more than 30 days overdue.

· Cash-flow pressure becomes much more visible when overdue volume is high, with firms carrying more overdue invoices reporting cash-flow problems at 50%, compared with 34% among firms with fewer late payments.

· Longer terms can normalize delay without removing the financial pressure: QuickBooks reported cash-flow problems among 60% of businesses with longer payment terms, compared with 40% of those using immediate terms.

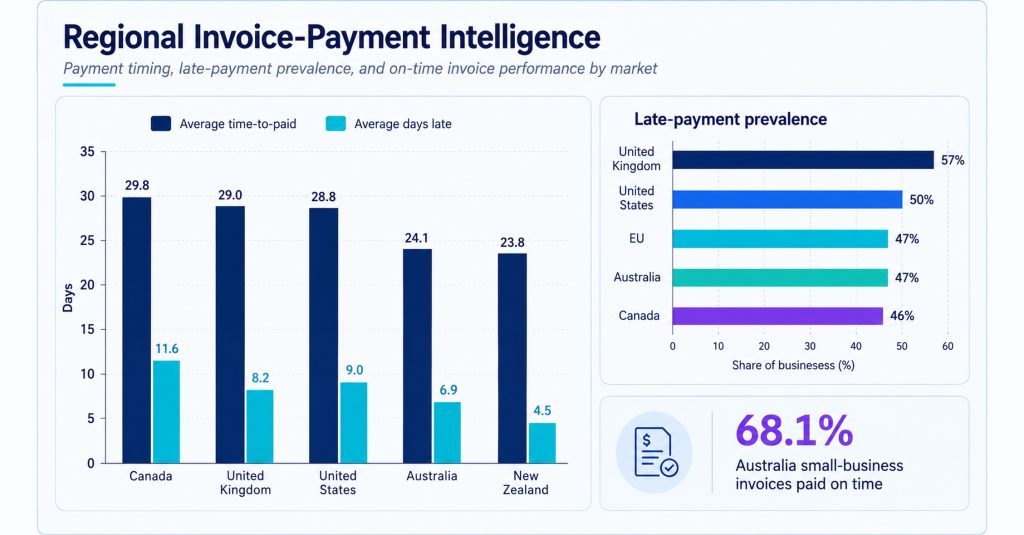

· Xero’s country-level invoice data places average time-to-paid at 29.8 days in Canada, 29.0 days in the United Kingdom, 28.8 days in the United States, 24.1 days in Australia, and 23.8 days in New Zealand.

· Late payment still sits on top of that wait. In the same Xero snapshot, invoices were paid 11.6 days late in Canada, 9.0 days late in the United States, 8.2 days late in the United Kingdom, 6.9 days late in Australia, and 4.5 days late in New Zealand.

· Atradius’ U.S. trade-credit research adds a B2B lens, with overdue invoices affecting 43% of credit-based B2B sales and average payment terms around 45 days from invoicing.

· Billtrust’s benchmark shows that process discipline can matter: days sales outstanding moved from 45 days in 2024 to 39 days in 2025, while touchless payments stayed above 92%.

· Automation helps, but information still matters. Versapay research points to data-transparency gaps, reconciliation errors, customer communication, and dispute management as recurring barriers inside invoice-processing workflows.

· A comparative late-payment review placed the late-payment share at 57% in the United Kingdom, 50% in the United States, 47% in both the EU and Australia, and 46% in Canada.

Editorial readout Invoice payment performance is not one metric. A business can have acceptable average terms but high overdue exposure, good online payment adoption but weak remittance matching, or low DSO but persistent disputes in a few large accounts. The better scorecard connects timing, terms, payment method, dispute reason, customer segment, and cash application so the team can see where the delay actually begins.

Why Invoice Payment Timing Is A Cash-Flow System

Invoice timing is often described as a customer behavior problem, but most late-payment patterns are created by the system around the customer. An invoice may be technically correct but still need a purchase-order match, a manager’s approval, a portal upload, a remittance file, or a dispute review before payment can move. For the seller, each of those steps has the same cash effect: revenue has been earned, but the money is not yet usable.

That is why DSO, average days late, aging buckets, dispute rate, unapplied cash, and payment-method mix belong together. A company with fast ACH settlement can still have slow cash application if remittance details are missing. A business with strict terms can still carry late balances if large customers treat those terms as flexible. A team with automated reminders can still struggle if the invoice lacks enough documentation to clear the buyer’s approval process.

The most practical invoice-payment analysis starts with ownership. Sales may set expectations, operations may create the documentation, billing may issue the invoice, customers may choose the method, and AR may chase the money. When those steps are managed separately, finance sees overdue balances but not the cause. When they are managed as one invoice-to-cash system, the numbers become much more useful.

· A DSO target in the 30- to 45-day range can look healthy on paper, but the right threshold depends on terms, customer mix, invoice size, seasonality, and whether overdue balances are concentrated in a few large accounts.

· The sample DSO calculation in the research workbook shows how sensitive the metric can be: $200,000 in accounts receivable against $600,000 in credit sales over a 30-day period produces a 10-day result.

· Billtrust’s move from 45 days of DSO to 39 days in the benchmark suggests that delivery, payment acceptance, matching, and follow-up can improve performance when the workflow becomes more structured.

· Average days delinquent still sat at 6 days in the same benchmark, which is a useful reminder that lower DSO does not mean every invoice arrives on time.

· Invoice volume changes the problem. Versapay’s mid-market data reported a median monthly invoice volume of 1,850, while larger revenue groups reported a median of 2,450, making small exception rates operationally expensive.

What the timing data means Invoice timing should be reviewed as a chain of events: issue date, customer receipt, approval, due date, payment initiation, settlement, remittance capture, and cash application. If one link is weak, the payment can be delayed even when the customer is willing to pay. That is why the best invoice-payment dashboards explain both how late the money is and why it is late.

How Long Businesses Wait To Get Paid

Country-level invoice-payment data is useful because it turns a familiar complaint into something finance can compare. A business that sells in several markets may use similar invoice terms everywhere, but customer payment behavior, banking norms, dispute habits, and local business culture can produce very different cash timing. The point is not to overreact to a single quarter. The point is to build a baseline that keeps each market from being judged by the wrong average.

· Canada had the longest average time-to-paid in Xero’s five-country March-quarter set, at 29.8 days, while New Zealand had the shortest at 23.8 days.

· The United States and the United Kingdom were almost identical on wait time, with U.S. invoices paid in 28.8 days on average and U.K. invoices in 29.0 days.

· Australia sat noticeably lower than the North American and U.K. figures, with invoices paid in 24.1 days on average and 6.9 days late.

· Canada’s average late-payment delay of 11.6 days was more than twice New Zealand’s 4.5-day late-payment delay.

· The gap between the U.K. and Australia was nearly five days on average time-to-paid, which can matter for businesses with weekly payroll, inventory replenishment, or subcontractor schedules.

· Xero’s implied issue-to-due pattern also differs by country, with the data suggesting roughly 20.8 days in the U.K., 19.8 days in the United States, 18.2 days in Canada, 17.2 days in Australia, and 19.3 days in New Zealand.

Figure 1. Country-level invoice timing should separate average time-to-paid from average days late, because a market can have similar payment terms but different post-due-date behavior.

The regional lesson is simple: invoice terms are not the same as invoice payment reality. A business can write net-30 terms and still behave like a net-39 business if its customers usually pay nine days late. A finance leader reviewing multiple countries should therefore compare actual payment timing against the stated terms, then investigate whether delays come from customer approval, documentation, portal friction, payment method, or internal follow-up.

Unpaid Invoices And Overdue Balances

Unpaid invoices create pressure because they sit between completed work and usable cash. For a small business, that gap can affect payroll, inventory, supplier payments, rent, owner compensation, hiring, and whether the business needs to use credit. The most useful late-payment statistics do not only show that customers owe money; they show how businesses respond when the money is not arriving on time.

QuickBooks’ U.S. small-business data is important because it connects unpaid invoices to operating behavior. The average amount owed to affected businesses, about $17,500, may be a small balance for a large corporation but a meaningful working-capital gap for a local contractor, clinic, agency, distributor, or professional-services firm. The risk rises when that balance is tied to a few large customers that are slow to approve or pay.

· The unpaid-invoice problem begins with breadth: QuickBooks found money owed from unpaid invoices among 56% of surveyed U.S. small businesses.

· The average unpaid exposure of roughly $17,500 can represent payroll, rent, supplier deposits, insurance premiums, loan payments, or tax obligations for a smaller firm.

· Overdue aging was common enough to deserve management attention, with 47% of businesses reporting at least some invoices more than 30 days overdue.

· QuickBooks measured the average overdue share at 10% of invoices, which means a business with hundreds of monthly invoices may be managing many late balances at once.

· Cash-flow problems rose to 50% among businesses with more overdue invoices, compared with 34% among firms carrying fewer late balances.

· Firms more affected by late payments were also more likely to raise prices, use loans, rely on lines of credit, and lean on business credit cards, connecting invoice timing to financing decisions.

· Business credit-card use reached 54% among firms more affected by late payments, compared with 46% among those less affected.

· Line-of-credit usage showed the same pattern, at 31% among firms more affected by late payments versus 21% among less affected firms.

· When payment pressure becomes persistent, price changes can follow; QuickBooks reported recent price increases among 30% of firms more affected by late payments and 21% of those less affected.

Figure 2. Unpaid invoices affect more than collections workload; they can reshape credit reliance, pricing decisions, and short-term cash planning.

Business interpretation A late invoice is not only a receivable aging entry. It can become a financing cost, a pricing decision, a supplier constraint, or a payroll risk. The right response depends on whether the problem is caused by customer habit, weak terms, missing information, dispute volume, payment-method friction, or internal posting delays.

Invoice Terms, Trade Credit, And Customer Risk

Invoice terms are the first control point in payment timing. They define expectations, but they do not guarantee behavior. A customer that receives 30-day terms may pay in 39 days, dispute near the due date, or use the seller as a source of informal credit. That is why trade-credit statistics should be read together with overdue share, average days late, and the concentration of receivables by customer.

· Atradius reported that overdue invoices affected 43% of U.S. credit-based B2B sales, which makes payment risk a normal trade-credit issue rather than a rare collections event.

· Average U.S. B2B payment terms in the Atradius data sat around 45 days from invoicing, longer than the net-30 language many smaller sellers imagine as standard.

· The same source placed bad debts around 4% of U.S. B2B credit sales, a reminder that delay and non-recovery are related but not identical risks.

· Western Europe showed a different trade-credit pattern, with overdue B2B invoices affecting 49% of credit sales and bad debts near 6%.

· Central and Eastern Europe had an even higher overdue share, around 53%, while bad debts were lower than Western Europe at roughly 4%.

· In the United Kingdom, late-payment research shows the problem varies by company size: microbusinesses and SMEs can face a different collections burden from larger firms with more formal credit teams.

· A business using long terms should review whether slow payers are strategically important customers, habitual late payers, dispute-heavy buyers, or accounts that need clearer payment instructions.

The practical question is not whether terms should always be shorter. Some industries use longer terms because the buyer needs approval time, proof of delivery, project verification, or consolidated billing. The question is whether the terms are intentional. If a seller offers 45-day terms but funds payroll weekly and pays suppliers before collection, the company has created a cash-flow bridge that should be priced, monitored, and reviewed as carefully as any other credit decision.

Payment Methods That Move Invoices From Approved To Paid

Once an invoice is approved, the payment method determines how quickly money can move and how cleanly it can be posted. Checks may still fit certain buyers because they carry familiar controls, signatures, and remittance stubs. ACH can be faster and cheaper but needs correct banking details and remittance information. Cards can improve convenience and speed for some customers while adding fees and policy decisions. Payment links and portals can make collection easier, but only when the customer can find the invoice, select the right balance, and trust the workflow.

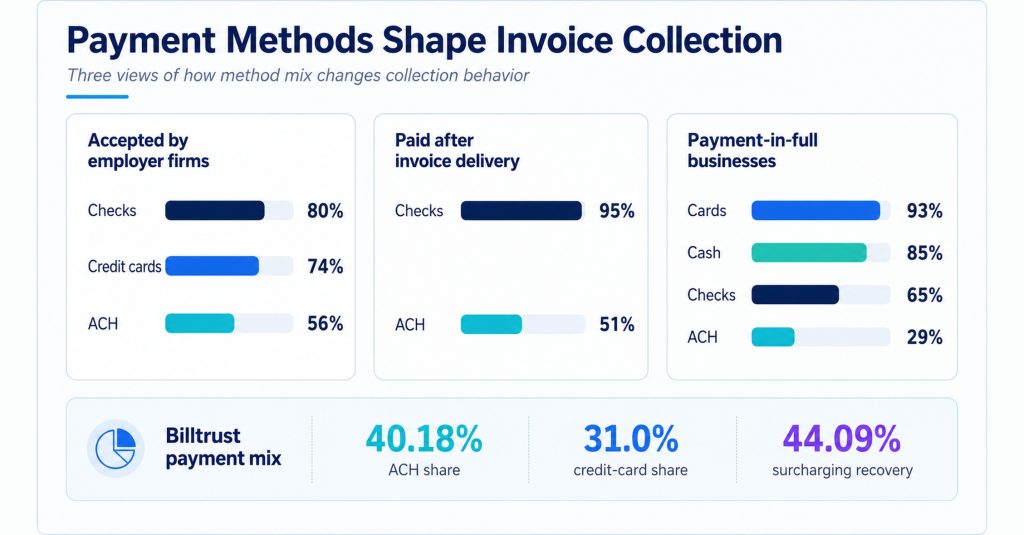

· Federal Reserve small-business data shows that 80% of employer firms accept checks, which explains why invoice-payment modernization cannot simply assume paper disappears quickly.

· Credit-card acceptance is also common, at 74% of employer firms, giving many businesses a faster collection path when fees and customer expectations make sense.

· ACH acceptance reached 56% across employer firms, but invoice-style businesses often need ACH for larger B2B balances because bank payments can be more appropriate than cards.

· Among firms paid after delivery or by invoice, check acceptance rises to 95%, showing how strongly invoice billing is still connected to traditional payment habits.

· The same invoice-after-delivery segment shows ACH acceptance at 51%, a meaningful base but still far below check acceptance.

· Payment-in-full businesses look different: card acceptance reaches 93%, cash 85%, checks 65%, and ACH only 29%, which reflects point-of-sale behavior more than invoice-to-cash behavior.

· Billtrust’s benchmark placed ACH share near 40.18% and credit-card share around 31.0%, a mix that makes fee policy, remittance capture, and customer segmentation important.

· A surcharging recovery rate of 44.09% shows that card-cost recovery is not automatic; it depends on customer response, policy communication, jurisdiction, and payment behavior.

Figure 3. Invoice-payment method choices should be evaluated by speed, cost, customer habit, remittance quality, and how cleanly the payment posts.

Payment-method rule The best invoice-payment method is not always the fastest settlement rail. It is the method that moves approved invoices into posted cash with the fewest avoidable exceptions. For a recurring customer, ACH enrollment may matter most. For a low-frequency small customer, a payment link may be simpler. For a large buyer, better remittance detail may create more value than a new payment button.

AR Automation And Touchless Invoice Payment

Automation works best after the invoice process is clear. If the invoice data is wrong, the approval path is unclear, or remittance is incomplete, automation can simply move the problem faster. The strongest AR benchmarks therefore need to be read in two layers: how much of the process is electronic, and how much of it is clean enough to post without manual work.

· Billtrust benchmarked touchless payments above 92%, showing that a mature payment environment can reduce manual handling after the customer chooses a supported method.

· Electronic invoice delivery was measured at 81.76%, which still leaves a meaningful minority of invoices outside the most efficient delivery path.

· Online envelope matching reached 88.48%, a strong figure that still leaves exception work when invoice volume is high.

· Line-item matching was even stronger, near 93.76%, but small mismatch percentages can still create significant workload at scale.

· Average days delinquent sat at 6 days, showing that automation can improve workflow without eliminating late behavior entirely.

· Versapay’s research around AR automation interest shows high demand for better workflows, but the adoption question depends on training, customer communication, and clean system data.

· When customers want to pay multiple invoices at once, the portal needs statement-level visibility, not only one invoice link at a time.

· Partial-payment support matters when buyers dispute one line item but are willing to pay the undisputed balance.

Figure 4. AR automation should be judged by both payment movement and information quality: delivery, matching, touchless payment, and delinquency all matter.

The operating lesson is that invoice-payment automation should not be sold internally as a magic collections tool. It is more accurate to frame it as a way to reduce avoidable touches: fewer missing invoices, fewer manual deposits, fewer customer emails asking how to pay, fewer remittance hunts, fewer unapplied cash items, and fewer cases where an invoice is technically paid but not yet applied to the right account.

Invoice Disputes, Portals, And Payment Information

Many invoice-payment delays are not caused by unwillingness to pay. They come from missing information. A buyer may need a purchase order, proof of delivery, tax clarification, a corrected line item, a statement balance, or the ability to pay several invoices together. When those details are difficult to find, the invoice can sit in a queue even if the customer has budget and intent.

· Versapay research shows customers value portal capabilities that let them see invoice history, payment status, and account detail rather than relying on email back-and-forth.

· The ability to pay multiple invoices together was valued by roughly 39% of customers in the research workbook, which is especially important for wholesale, distribution, and recurring B2B relationships.

· Line-item dispute capability was valued by about 37.67%, showing that customers often need to challenge part of an invoice without freezing the whole balance.

· Customer-friendly user experience was cited around 36%, which sounds like a design issue but becomes a cash issue when buyers avoid a confusing portal.

· Support for partial payment, valued near 33%, can keep undisputed cash moving while a smaller exception is resolved.

· Communication gaps in AR research matter because a customer may not know whether the invoice is wrong, the payment was received, a credit was applied, or the account still has an open balance.

· Data-transparency issues can slow both sides: the buyer cannot approve confidently, and the seller cannot tell whether the invoice is waiting on the buyer, the bank, the portal, or internal posting.

Portal interpretation A portal should not simply display a balance due. It should reduce the number of reasons a buyer has to delay payment. That means invoice copies, purchase-order references, payment history, dispute paths, statement views, partial-payment handling, remittance capture, and clear payment instructions all belong in the invoice-payment discussion.

Regional Invoice-Payment Intelligence

Regional statistics deserve their own section because the same invoice policy can perform differently across markets. Payment speed, late behavior, trade-credit use, bad-debt risk, bank-payment adoption, and customer approval culture all vary. A finance team that treats regional averages as universal may push the wrong fix: stricter reminders where documentation is the issue, shorter terms where buyer approval is the bottleneck, or a new portal where local payment habits require a different method.

· The five-country Xero data shows Canada with the longest average wait at 29.8 days, but also the highest average late delay at 11.6 days.

· New Zealand had the shortest average wait in that dataset at 23.8 days and the lowest average late delay at 4.5 days.

· The United States and United Kingdom were close on average time-to-paid, but the U.S. late delay of 9.0 days was slightly higher than the U.K. figure of 8.2 days.

· Australia’s average wait of 24.1 days was relatively short, yet the late delay of 6.9 days still shows that faster markets are not automatically on-time markets.

· The comparative late-payment review placed the United Kingdom at 57% late-payment prevalence, above the United States at 50%, the EU and Australia at 47%, and Canada at 46%.

· Within Canada, province-level timing can add another layer to planning; Ontario, Alberta, and British Columbia may show different invoice behavior depending on industry mix and customer base.

· Australia’s payment-times reporting data adds a policy-oriented view, including a small-business invoice on-time figure around 68.1% in the workbook’s source set.

Figure 5. Regional invoice-payment comparisons are most useful when they connect payment timing, late-payment prevalence, and local customer behavior instead of ranking countries in isolation.

The right regional response is diagnostic. If a market pays later because terms are longer, the decision may be commercial. If customers pay after the due date despite similar terms, the problem may be approval timing, reminder cadence, documentation quality, or collections discipline. If invoices are paid but cash application lags, the regional issue may be bank file quality, remittance habits, or portal adoption rather than customer willingness to pay.

How Invoice Payment Delays Show Up In Real Workflows

Invoice-payment statistics become more useful when they are translated into real workflows. A contractor, distributor, professional-services firm, SaaS company, and healthcare supplier can all experience late invoice payment, but the causes are different. One may wait for project sign-off; another may wait for a bulk statement payment; another may need a buyer’s AP portal; another may have recurring subscriptions with failed payment details.

· A contractor working on milestones may have a clean invoice but still wait if the buyer has not approved the completed phase or released retainage.

· A wholesaler with many small invoices may care less about one late bill and more about whether customers can pay a statement, include remittance detail, and avoid short-paying without explanation.

· A professional-services firm may find that invoices sit because the buyer wants more detail about hours, scope, expenses, or approvals before releasing payment.

· A SaaS vendor may have a lower invoice-friction problem if autopay and ACH are common, but failed cards, contract amendments, and billing-contact changes can still delay collection.

· A healthcare or education supplier may deal with third-party payment arrangements, split responsibility, or documentation requirements that make invoice timing less predictable.

· Businesses paid after delivery face a different challenge from businesses paid at the time of sale; Federal Reserve data shows slow-paying customers are much more relevant in invoice-style arrangements than point-of-sale transactions.

These examples show why invoice-payment improvement should begin with customer paths, not a generic reminder sequence. A reminder helps when the customer forgot. It does not fix missing documentation, a disputed line item, a failed portal upload, a buyer that needs consolidated statements, or an internal cash-application backlog. The more precisely a business identifies the delay reason, the less likely it is to treat every overdue invoice the same way.

What Better Invoice Payment Follow-Up Looks Like

Follow-up is one of the easiest areas to over-simplify. A business may send reminders, but the reminders may be too late, too generic, or disconnected from the reason the invoice is unpaid. A better follow-up process separates pre-due confirmation, due-date reminders, post-due escalation, dispute resolution, and credit review. Each step should answer a specific question: did the customer receive the invoice, can they approve it, do they know how to pay, is anything disputed, and has the payment posted correctly?

· A pre-due reminder is most useful when it catches missing purchase orders, wrong contacts, delivery documentation, or portal requirements before the invoice becomes late.

· A due-date reminder should make payment easy, not simply repeat the balance; it should include payment options, invoice identifiers, and any statement-level context the customer needs.

· A post-due message should separate forgetfulness from friction. The customer who misplaced the invoice needs a different response from the customer waiting on dispute review.

· When invoices are more than 30 days overdue, as many QuickBooks respondents reported, the issue should usually move from routine reminder to risk review.

· A high-risk customer should not necessarily lose access to credit immediately, but the business should know whether the exposure is growing, concentrated, disputed, or historically recoverable.

· Collections work becomes more productive when AR can see payment history, open disputes, previous reminders, partial payments, and the customer’s preferred payment path in one place.

Follow-up principle Good invoice follow-up is not louder collections. It is clearer diagnosis. The reminder sequence should help the business learn whether the invoice is unpaid because of timing, approval, documentation, dispute, method, cash constraint, or posting error. Once the reason is known, the follow-up can become more specific and less repetitive.

Payment Links, Reminders, And Customer Behavior

Payment links and reminders are often treated as small tactical features, but they can reveal a great deal about invoice-payment behavior. If a customer pays quickly after receiving a payment link, the original barrier may have been convenience. If a customer opens reminders but still does not pay, the barrier may be approval, documentation, or cash availability. If a customer repeatedly pays only after a phone call, the business may have a relationship or accountability issue rather than a payment-method issue.

The most useful reminder strategy is therefore not simply to send more messages. It is to match each message to the invoice’s status. A pre-due note can confirm that the buyer received the invoice and has what they need. A due-date note can make payment easy. A post-due note can ask whether the invoice is approved, disputed, missing a purchase order, or waiting for a scheduled pay run. The language should stay professional, but the workflow behind it should become more diagnostic over time.

This is also where invoice-payment statistics become useful for daily management. A company that tracks which reminders produce payment, which customers ask for copies, which invoices trigger disputes, and which payment methods create clean remittance can improve without guessing. The data may show that a payment link reduces friction for small balances, that a statement view helps high-volume customers, or that a particular customer segment needs purchase-order validation before invoices are sent.

· Payment links are most valuable when the buyer is willing to pay but does not want to request bank details, print a check, or log into a separate portal.

· When a business offers cards for invoice payment, the convenience benefit should be compared with fee exposure, surcharge recovery, and the invoice sizes most likely to use the option.

· ACH enrollment works best when the seller can capture banking authorization cleanly and connect the payment to invoice-level remittance data.

· Recurring invoices should be reviewed separately because scheduled or autopay options can reduce follow-up work when the customer relationship is stable.

· Payment reminders become stronger when they include invoice number, due date, amount, payment options, and a direct path for raising a dispute.

· A reminder that asks whether the invoice has been approved can surface internal buyer delays earlier than a generic overdue notice.

· Customers that repeatedly short-pay invoices should be tagged differently from customers that pay late but pay in full, because the operational fix is not the same.

· When reminder-to-payment conversion is weak, the team should inspect invoice detail, customer contacts, portal requirements, and dispute history before assuming customers are ignoring the message.

Reminder interpretation The best reminder program creates information as well as action. It should tell the business whether the invoice is unpaid because the buyer forgot, the invoice is waiting for approval, the payment method is inconvenient, the customer disputes the balance, or the business has already received money that has not been applied. That diagnosis is what turns follow-up from repetitive chasing into a more controlled invoice-to-cash process.

Company Size Changes The Invoice Payment Problem

Company size affects invoice payment in two ways. Small businesses often feel each unpaid invoice more sharply because cash reserves are thinner and customer concentration can be higher. Larger companies may have more formal AR teams and systems, but they also process more invoices, more exceptions, more customer portals, and more payment data. As a result, the same percentage problem can produce a very different workload.

· A small firm owed $17,500 from unpaid invoices may experience that as a payroll or supplier-payment issue, not simply an AR metric.

· A larger business processing thousands of invoices may tolerate a small exception rate poorly because each point of mismatch can create many manual cases.

· Versapay’s median monthly invoice volumes of 1,850 in the mid-market and 2,450 in larger revenue groups show why scale changes the cost of manual handling.

· For small businesses, the priority may be clearer terms, payment links, and earlier reminders; for larger firms, the priority may be matching, portal adoption, dispute routing, and cash-application automation.

· High-volume businesses should segment late payment by customer group because one enterprise buyer can dominate the overdue balance even if the overall invoice count looks manageable.

· Low-volume service businesses should review invoice detail and customer communication because one disputed project invoice can distort cash flow for a full month.

This is why a single invoice-payment benchmark should never be used as a universal target. A healthy metric for one company may be weak for another if terms, margins, customer size, industry risk, and invoice volume differ. The most useful target is the one that fits the business model and improves over time without damaging customer relationships or margin quality.

From Invoice Format To Clean Cash Application

A paid invoice is not finished if the payment cannot be matched. This is one of the most overlooked parts of invoice-payment performance. The buyer may have sent the money, but the seller still needs enough detail to identify the customer, invoice number, purchase order, amount, discount, credit memo, fee, and bank deposit. Without that connection, cash can sit unapplied even after the customer believes the account is settled.

· Billtrust’s 88.48% online envelope match rate is a strong automation marker, but the unmatched share can still produce manual work at scale.

· A line-item match rate near 93.76% shows that structured data can support clean posting, while still leaving exceptions that require review.

· When eDelivery reaches 81.76%, the remaining paper, PDF, or non-standard cases deserve attention because they may belong to customers with older payment habits.

· A card share around 31.0% may help speed payment for certain customers, but it also makes fee visibility and surcharge policy important.

· A surcharging recovery rate around 44.09% means finance cannot assume all card costs will be offset by policy alone.

· Customers that pay multiple invoices together need statement views, bulk selection, and remittance clarity, not only individual invoice links.

· Line-item dispute support matters because a buyer may be willing to pay most of the invoice while one item waits for review.

Clean cash application starts before the payment arrives. The invoice should carry the right identifiers, the payment page should capture the right references, the bank or processor data should flow into the accounting system, and the AR team should have rules for partial payments, discounts, short pays, and disputed items. If any of those pieces are missing, faster payment can still create a manual posting backlog.

A Practical Invoice Payment Example

Consider a regional distributor that sends thousands of invoices each month to retailers, contractors, and service providers. Although the company works with dependable customers, cash flow still arrives inconsistently because every client follows a different payment process. Some customers pay by check, others prefer ACH transfers, while some combine multiple invoices into a single payment or question freight and tax charges before approval. Certain clients also require invoices to pass through complex AP portal systems, creating additional delays. Similar challenges can affect creative professionals who rely on a photography invoice template to organize project charges, payment schedules, editing fees, and client approvals more clearly. For the accounts receivable manager, overdue balances are not caused by one single issue, but by a variety of payment habits, approval workflows, and billing complications that require more organized financial processes.

The distributor does not need one universal payment method. It needs a cleaner path for each customer behavior. High-volume buyers can receive consolidated statements and ACH instructions. Small customers can use payment links. Dispute-heavy accounts can receive clearer line-item detail and delivery proof. Customers that pay multiple invoices together can be moved to a portal view that supports bulk selection and remittance capture. The goal is not to add options for their own sake; it is to reduce the number of invoices that need human follow-up.

· If the distributor’s customer base behaves like invoice-after-delivery firms in the Federal Reserve data, check acceptance may remain very high, near 95%.

· ACH still has room to grow in that same invoice-style segment because acceptance sits around 51%, below checks but high enough to justify enrollment work.

· Card payment can remain useful for smaller invoices because credit-card acceptance across employer firms is around 74%, even if the distributor must manage fees carefully.

· Slow-paying customer challenges are especially relevant in payment-after-delivery arrangements, where the Federal Reserve data places that issue around 66%.

· Customers using scheduled service arrangements may be better candidates for ACH or recurring payment enrollment because ACH acceptance in that segment sits near 66%.

· If the distributor supports partial payment, undisputed cash can keep moving while freight, tax, or quantity exceptions are resolved.

The example shows why invoice-payment improvement should be designed around customer paths. One customer may need better documentation, another may need ACH instructions, another may need portal access, and another may need earlier escalation. The right system keeps money moving while also preserving the relationship, because not every late invoice is a bad customer and not every fast payment is clean cash application.

Invoice Payment Metrics Leaders Should Track

A useful scorecard should help the team locate the delay. A blended overdue balance tells finance that cash is late, but it does not show whether the problem is customer approval, weak terms, missing documentation, slow method, disputed lines, failed payment, or internal posting backlog.

| Metric | What it shows | How leaders should use it |

|---|---|---|

| Average time-to-paid | How many days pass between invoice issue and payment. | Compare by customer group, country, product line, and payment method. |

| Average days late | How far payments drift beyond the due date. | Separate term design from post-due behavior. |

| DSO | How efficiently receivables convert into cash. | Review trend and concentration, not only the headline number. |

| Overdue aging buckets | Where unpaid balances sit by age. | Move older balances into escalation, dispute, or credit review. |

| Payment-method mix | How customers pay invoices. | Balance speed, cost, remittance quality, and customer preference. |

| Dispute rate | How often invoice detail blocks payment. | Fix documentation, pricing, tax, delivery, and approval issues upstream. |

| Match rate | How cleanly payments connect to invoices. | Reduce unapplied cash and manual cash-application work. |

| Reminder-to-payment conversion | Which follow-ups actually move money. | Improve reminder timing, message quality, and escalation paths. |

| Customer concentration | Whether a few accounts drive overdue exposure. | Prioritize account-level conversations and credit-policy review. |

A 90-Day Invoice Payment Improvement Plan

Statistics become useful when they become an operating plan. A realistic improvement cycle starts with measurement, fixes obvious friction, and then adds automation where the process is clean enough to automate.

| Timing | What to do | Output |

|---|---|---|

| Days 1-30 | Build the baseline by customer, country, invoice age, payment method, dispute reason, and cash-application status. | A clear map of where invoices are delayed and why. |

| Days 31-60 | Fix high-confidence leaks such as missing invoice detail, unclear payment instructions, weak reminders, portal friction, and customers without easy ACH or card paths. | A prioritized fix list with owners and before/after metrics. |

| Days 61-90 | Review terms, credit exposure, automation candidates, dispute patterns, and customer-segment behavior. | A repeatable invoice-to-cash scorecard and a practical policy for follow-up, payment methods, and escalation. |

The best 90-day plan does not assume technology alone will fix customer behavior, and it does not assume harder collections will fix process gaps. It links invoice quality, payment method, customer communication, credit policy, and AR automation into one operating model.

Invoice Payment Statistics FAQ

Common questions

· What is the average time for an invoice to be paid? The answer depends on country, terms, and customer mix. Xero’s March-quarter data placed average time-to-paid at 28.8 days in the United States, 29.8 days in Canada, 29.0 days in the United Kingdom, 24.1 days in Australia, and 23.8 days in New Zealand.

· How late are invoices paid on average? In the same five-country set, Canada averaged 11.6 days late, the United States 9.0 days, the United Kingdom 8.2 days, Australia 6.9 days, and New Zealand 4.5 days.

· How common are unpaid invoices for small businesses? QuickBooks found unpaid-invoice exposure among 56% of surveyed U.S. small businesses, with affected businesses owed about $17,500 on average.

· Why do invoices get paid late? The cause can be long terms, approval delays, missing purchase orders, disputes, weak reminders, inconvenient payment methods, portal requirements, incomplete remittance data, or internal posting backlogs.

· Which payment methods help invoice collection? ACH, cards, payment links, portals, scheduled payments, and autopay can all help, but the best method depends on invoice size, customer habit, fees, remittance quality, and posting accuracy.

· Which invoice-payment metrics matter most? A practical scorecard includes time-to-paid, average days late, DSO, overdue aging, dispute rate, payment-method mix, match rate, unapplied cash, customer adoption, and reminder-to-payment conversion.

Final Takeaway

Invoice payment statistics show that the real question is not whether customers eventually pay. The operational question is how reliably a business turns issued invoices into usable, accurately posted cash without excessive reminders, unresolved disputes, avoidable fees, credit reliance, or manual reconciliation.

The strongest numbers point in the same direction. Many small businesses are owed money from unpaid invoices. Country-level payment delays continue beyond due dates. B2B trade credit leaves meaningful shares of sales overdue. AR teams still fight missing information even when payment options are available. At the same time, automation benchmarks show that eDelivery, touchless payment, ACH/card acceptance, matching, and customer portals can improve invoice-to-cash performance when the underlying workflow is clear.

For finance leaders, the practical goal is a payment system that does three things well. First, it gives customers clear invoices, terms, documentation, and convenient payment options. Second, it gives the business early visibility into late, disputed, risky, or incomplete invoices. Third, it connects payment collection, remittance detail, and posting so that money received becomes cash applied. Invoice payment is not only a collections issue; it is a working-capital system, a customer-experience system, and a data-quality system at the same time.