The freelance economy is no longer a narrow side-hustle category. It is a broad labor system that includes full-time independent professionals, occasional project workers, creator businesses, platform-based specialists, consultants, remote technical talent, and small solo firms that sell expertise without becoming traditional employers.

The numbers matter because the growth of freelancing is reshaping how businesses access talent and how professionals generate income. Companies often hire freelancers to fill skill gaps, explore new markets, manage seasonal workloads, or gain access to specialized expertise without the long-term cost of full-time employees. At the same time, freelancers are using the market to build portfolio careers, replace traditional salaries, create additional income streams, and turn specialized skills into scalable service businesses. As this ecosystem expands, tools such as a freelance invoice template have become essential for managing payments professionally, maintaining financial records, and creating a smoother working relationship between freelancers and clients.

That is why this report treats freelance economy statistics as business signals rather than loose labor headlines. The strongest benchmarks separate participation from income quality, platform activity from direct client work, and flexible work from sustainable independent businesses. A market can look large because many people freelance occasionally, but the healthier question is whether workers are earning well, diversifying clients, getting paid reliably, and moving into higher-value skills.

Executive Freelance Economy Benchmarks

The headline numbers show the scale of freelance work, but they also show why the category is hard to measure. Freelancing can mean a side project, a main-job independent contract, a solo consulting business, a platform gig, or a creator-led income stream. The strongest benchmarks therefore need to be read together, not as interchangeable counts.

The numbers that define the freelance economy

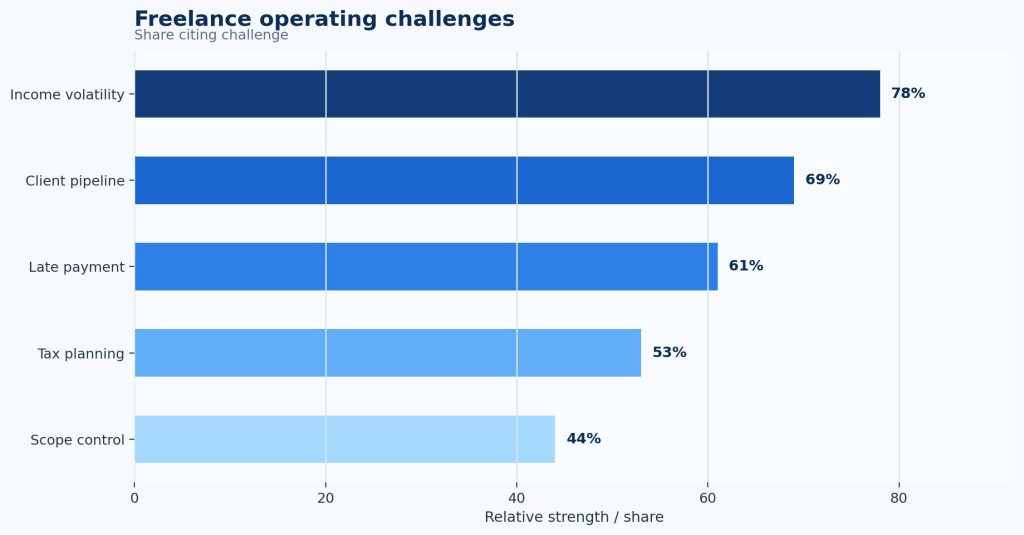

• Upwork reported 64 million Americans freelanced in 2023, equal to 38% of the U.S. workforce.

• U.S. freelancers contributed $1.27 trillion in annual earnings in 2023.

• The U.S. freelance workforce rose from 53 million in 2014 to 64 million in 2023, adding about 11 million workers over the decade.

• MBO reported 72.7 million U.S. adults in independent work arrangements in 2024, up from 72.1 million in 2023.

• MBO’s independent-worker count rose from 38.2 million in 2020 to 72.7 million in 2024, a roughly 90% increase.

• BLS found 11.9 million people were independent contractors on their sole or main job in July 2023, equal to 7.4% of total U.S. employment.

• The World Bank estimates 154 million to 435 million people work through online gig platforms worldwide.

• That global online gig range equals about 4.4% to 12.5% of the global labor force.

• Grand View Research values the global freelance-platforms market at $6.37 billion in 2025.

• The freelance-platforms market is projected to reach $24.16 billion by 2033, implying an 18.6% CAGR from 2026 to 2033.

• MBO reported a record 5.6 million independent workers earning more than $100,000 annually in 2025.

• Payoneer reported the worldwide average freelance hourly rate at $23 in 2022, while another Payoneer benchmark placed global rates near $28/hour.

• Payoneer reported North America as the highest-rate region at about $44/hour, compared with about $31/hour in Western Europe.

• IPSE reported that the solo self-employed contributed £366 billion to the UK economy in 2024.

• Upwork data reported by Axios found AI-related freelance earnings increased 25% year over year.

The executive view is simple: freelance work is large enough to influence labor planning, but too mixed to judge from headcount alone. A 64 million freelancer estimate, a 72.7 million independent-worker estimate, and an 11.9 million official main-job contractor benchmark can all be useful at the same time. They answer different planning questions. The first helps size broad freelance participation, the second captures the full independent-work ecosystem, and the third shows the narrower labor-market core. A premium reading of the category starts by choosing the right definition before comparing growth, earnings, or risk.

What this shows: the freelance economy is large, but not uniform. A high-earning independent consultant, a part-time designer with a few clients, a delivery-platform worker, and a remote software specialist may all appear inside the same broad conversation.

The most important reading is not that every worker is becoming a freelancer. It is that independent work now sits across multiple layers of the labor market. Some people freelance to increase income while keeping a salaried role, some use independent work as a full-time business, and some move between contracts because platforms make demand more visible. For businesses, this means freelance statistics should be read as a talent-capacity signal, not only a labor-count signal. A company that understands the difference can decide when to hire permanently, when to use specialized contractors, and when a recurring freelance relationship should be treated like a strategic supplier rather than a casual gig.

Why Freelance Definitions Change the Numbers

Freelance statistics can look contradictory when they are actually measuring different things. The official labor-market lens is narrow because it focuses on people whose sole or main job is independent contracting. Survey-based freelance estimates are broader because they include mixed earners, side workers, creators, and people who sell skills independently even if they also hold traditional jobs. Platform estimates can be wider still because they include registered online gig workers across many countries.

| Measurement lens | Headline benchmark | What it captures | How to interpret it |

|---|---|---|---|

| BLS independent contractors | 11.9M people / 7.4% of U.S. employment | People whose sole or main job was independent contracting in July 2023. | Best for a narrow official labor-market baseline. |

| Upwork freelancers | 64M Americans / 38% of the workforce | A broader freelance workforce that includes people doing freelance work during the year. | Best for understanding total freelance participation and earnings. |

| MBO independent workers | 72.7M U.S. adults in 2024 | Independent workers across full-time, part-time, occasional, and side-work categories. | Best for understanding the full independent-work ecosystem. |

| World Bank online gig work | 154M-435M global online gig workers | Workers connected to online gig platforms worldwide. | Best for global platform scale, but not a direct comparison to national freelance surveys. |

Definition and measurement benchmarks

• Upwork’s 64 million freelancer count is about 5.4x the BLS 11.9 million main-job independent-contractor figure.

• MBO’s 72.7 million independent-worker estimate is about 6.1x the BLS main-job contractor benchmark.

• MBO’s 2024 independent-worker estimate is about 8.7 million higher than Upwork’s 2023 freelancer estimate.

• The World Bank’s lower bound of 154 million online gig workers is about 2.4x Upwork’s U.S. freelancer count.

• The World Bank’s upper bound of 435 million online gig workers is about 6.8x Upwork’s U.S. freelancer count.

• BLS reported 10.6 million independent contractors in 2017, equal to 6.9% of employment, compared with 11.9 million and 7.4% in 2023.

• The official BLS independent-contractor count increased by about 1.3 million from 2017 to 2023.

• BLS reported workers age 55+ had an 11.5% independent-contractor rate, compared with 6.9% among workers age 25-54.

The practical lesson is simple: the freelance economy should not be summarized by one number. For workforce planning, the BLS count is useful because it is narrower and more formal. For market opportunity, Upwork and MBO are more useful because they capture side work and mixed income. For platform strategy, the World Bank range explains why online gig work has become a global labor-market infrastructure category.

This definition gap also explains why growth narratives can look inconsistent. Official labor data may show a smaller freelance base because it asks whether independent contracting is the worker’s main job. Survey-based freelancer reports often capture side work, professional contracting, and occasional project income that official classifications may miss. Platform estimates then add another layer because a worker can have a profile, complete occasional tasks, or use more than one marketplace at the same time. The cleanest approach is to state which definition is being used before comparing markets; otherwise, a narrow employment statistic can be wrongly compared with a broad platform-participation estimate.

Market Size, Workforce Growth, and Platform Infrastructure

Freelance work is now large enough to influence payments, business software, tax reporting, talent acquisition, and cross-border service markets. The market is not growing only because more people want flexibility. It is also growing because businesses increasingly buy expertise as projects, platforms make workers more discoverable, and remote collaboration has reduced the friction of hiring talent outside a local labor market.

Workforce and economic scale benchmarks

• U.S. freelancer count increased from 60 million in 2022 to 64 million in 2023, adding roughly 4 million freelancers in one year.

• Freelancing represented 39% of the U.S. workforce in 2022 and 38% in 2023, showing that headcount can rise even when workforce share changes slightly.

• U.S. freelance headcount grew from 59 million in 2021 to 64 million in 2023, a gain of 5 million workers, or about 8.5%.

• The move from 60 million to 64 million freelancers represents about 6.7% year-over-year headcount growth.

• The 2014-to-2023 rise from 53 million to 64 million implies about 20.8% cumulative growth.

• U.S. freelancers generated approximately $1.35 trillion in annual earnings in 2022 and $1.27 trillion in 2023.

• The 2022-to-2023 shift represented about an $80 billion decline in estimated annual freelance earnings despite a larger freelancer count.

• Dividing $1.27 trillion by 64 million freelancers implies roughly $19,844 in annual freelance earnings per freelancer, though the average hides large differences between full-time independents and occasional freelancers.

• MBO’s independent-worker count added about 34.5 million people from 2020 to 2024.

• MBO’s high-earner count moved from about 4.7 million in 2024 to 5.6 million in 2025, adding around 900,000 $100K+ independents.

Platform infrastructure benchmarks

• The global freelance-platforms market is projected to become about 3.8x larger, rising from $6.37 billion in 2025 to $24.16 billion by 2033.

• The platform component of the freelance-platform market generated about $3.22 billion in 2025.

• That platform component is expected to reach $10.96 billion by 2033 at a 16.9% CAGR.

• North America is identified as the largest freelance-platform revenue region in 2025.

• Japan is expected to register the highest country CAGR for freelance platforms from 2026 to 2033.

• India’s freelance-platform market is estimated at $265.1 million in 2025 and forecast to reach $1.54 billion by 2033.

• India’s freelance-platform forecast implies a 25.1% CAGR from 2026 to 2033.

The platform figures matter because freelance work is not only a labor trend. It is also a software, payments, trust, and matching problem. Marketplaces need identity checks, reviews, escrow or payment protection, discovery tools, tax workflows, contract templates, dispute processes, and client communication systems. That infrastructure is one reason the platform market can grow faster than overall labor-force participation.

That infrastructure layer is especially important as freelance work moves into higher-value categories. A marketplace for low-risk microtasks can operate with simple search, ratings, and basic payment flows. A platform that supports software engineering, financial consulting, design systems, marketing analytics, legal support, or technical writing needs stronger proof of skill, clearer project scope, milestone payments, secure file exchange, and faster dispute handling. As a result, platform-market growth should be read as a sign that freelance work is becoming more operationally complex. The more companies rely on external specialists for business-critical work, the more they need vendor-style controls around onboarding, payment timing, confidentiality, and project accountability.

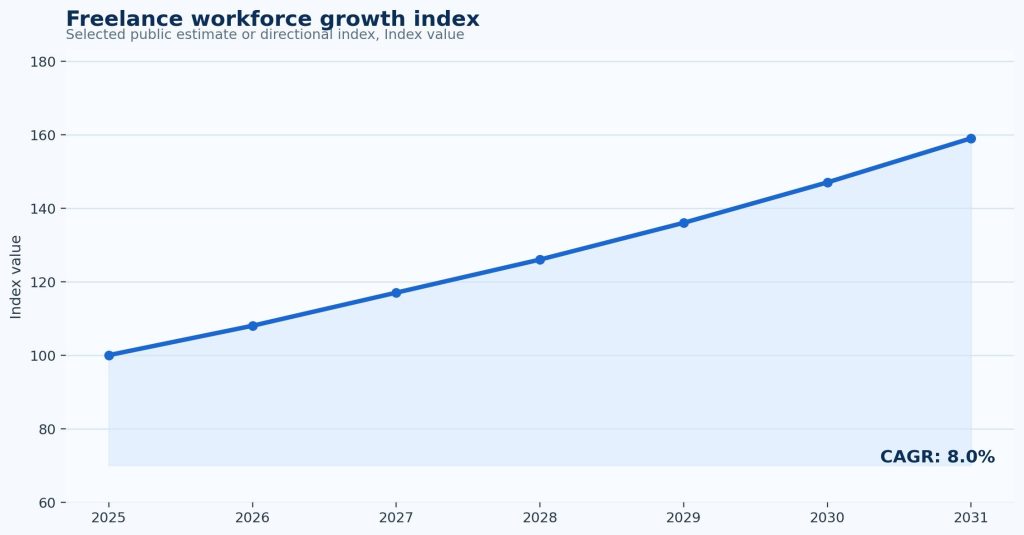

Figure 1. Freelance economy scale should be read across workforce participation, annual earnings, independent-worker definitions, and platform-market growth.

Freelance Earnings, Rates, and Income Quality

Income is the most important quality test for the freelance economy. A rising freelancer count does not automatically mean workers are earning more or becoming more secure. The same market can include high-income consultants, technical specialists, creators, occasional side earners, and workers taking on extra jobs because cost pressure has increased.

The income story is also where freelance economy statistics become more practical. A high hourly rate does not always mean high annual income if the worker spends too much time on unpaid sales, administration, revisions, and client management. A lower headline rate can sometimes produce stronger effective income when the freelancer has recurring clients, low acquisition cost, clean scope, and fast payment cycles. The better measure is not only what a freelancer charges, but how much of the working week turns into paid, collectible work.

Earnings and rate benchmarks

• MBO reported 5.6 million independent workers earning more than $100,000 annually in 2025.

• Upwork’s gig-economy summary cited 4.7 million U.S. independent workers earning over $100,000 in 2024.

• The number of U.S. independents earning over $100,000 rose from 3.0 million in 2020 to 4.7 million in 2024.

• Payoneer reported the worldwide average hourly freelance rate at $23 in 2022.

• Another Payoneer benchmark placed the global average freelance rate at $28/hour, up from $21/hour in 2020.

• The $21-to-$28/hour comparison implies about 33% rate growth between the referenced Payoneer reports.

• Payoneer reported North America at about $44/hour, roughly 42% higher than the Western Europe benchmark of $31/hour.

• Payoneer found 38% of freelancers increased rates, 46% maintained rates, and 15% saw rates decline.

• Payoneer reported 41% of freelancers raised their rates in response to inflation or cost pressure.

• Payoneer also found 55% of freelancers took on more work because of cost-of-living pressure.

• Payoneer reported female freelancers earn on average 84% of men’s earnings across fields, implying a 16% gender earnings gap.

• Payoneer reported 32% of freelancers expanded their client base into new countries.

What stronger freelance income usually has in common

• Higher-income freelancers usually sell a defined outcome, specialty, or advisory layer rather than only selling hours.

• Recurring work, retainers, productized services, and long-term client accounts often matter more than one unusually high project fee.

• Client concentration can make annual income look stable until one buyer pauses budget, changes strategy, or moves work in-house.

• Platform work can create fast access to demand, but direct client relationships usually give freelancers more control over pricing, scope, and repeat work.

• Effective income should be measured after unpaid proposal time, revisions, software costs, platform fees, taxes, late payments, and slow collection cycles.

These points make the income section more than a rate comparison. Freelancers and businesses both need to distinguish between visible price and durable earnings. The most resilient independent professionals usually combine technical skill, clear positioning, strong client selection, and a repeatable delivery process. That is different from simply being busy.

| Income signal | Statistical meaning | Business or worker implication |

|---|---|---|

| High earners | 5.6M independents above $100K annually | Freelancing can be a high-income professional model, not only supplemental work. |

| Rate pressure | 38% raised rates, 46% held rates, 15% declined | Freelancers face uneven pricing power depending on skill, region, and demand. |

| Cost pressure | 55% took on more work because of cost-of-living pressure | More work is not always a sign of stronger opportunity; it can reflect financial strain. |

| Gender gap | Women earned 84% of men’s freelance earnings | Income quality should be measured by equity, not only average rates. |

Income quality is therefore more useful than average income alone. Leaders should compare rate movement, client diversity, project size, repeat work, income volatility, and payment reliability. For freelancers, the strongest signal is not only hourly rate; it is the combination of rate, billable utilization, client concentration, payment speed, and the share of work that comes from repeat or referral demand.

A better income-quality view separates headline rates from take-home stability. A freelancer earning a strong project rate may still have unstable income if work arrives unevenly, clients pay late, or project scopes expand without change orders. The reverse can also be true: a freelancer with a moderate hourly rate but recurring retainers, predictable invoicing, low acquisition cost, and repeat clients may have a healthier business than someone with higher one-off project fees. For this reason, income statistics should be interpreted together with utilization, billable share of working time, payment speed, client concentration, and the percentage of work that comes from repeat relationships.

How Freelance Economics Change by Work Model

Some independent workers sell a few hours of extra work each month. Others run full-time solo businesses, manage retainers, or sell specialized technical services. The data becomes more useful when it separates occasional participation from professional independence, platform gigs from direct client work, and income opportunity from income pressure.

A useful way to understand the freelance economy is to separate the work model from the worker label. A solo consultant billing directly to enterprise clients has very different economics from a marketplace seller completing small fixed-price jobs. A creator who monetizes an audience has different risk than a contract developer with three long-term accounts. A side-hustle freelancer may value flexibility more than scale, while a full-time independent professional needs predictable demand, pricing discipline, tax planning, and client diversification.

Work-model interpretation benchmarks

• The gap between 11.9 million BLS main-job independent contractors and 64 million Upwork freelancers shows how much of the market includes side work, mixed income, or broader independent activity.

• MBO’s 72.7 million independent-worker estimate is useful because it captures full-time, part-time, occasional, and side-work arrangements rather than only one main-job category.

• The presence of 5.6 million $100K+ independents shows that freelancing can support high-income professional businesses, but it should not be confused with the experience of all freelancers.

• The 55% of freelancers taking on more work because of cost pressure shows that higher activity can also reflect financial strain rather than stronger pricing power.

• The EU benchmark that 61.2% of self-employed people had more than nine clients provides a useful indicator of diversification, while one-client dependency would signal a different risk profile.

• The 32% of freelancers expanding into new countries shows how online work can reduce local market dependence when a freelancer has exportable skills and payment access.

This work-model lens helps prevent misleading conclusions. A company hiring freelance specialists cares about availability, skill depth, reliability, and project governance. A freelancer building a durable business cares about rate quality, repeat buyers, client spread, payment speed, and pipeline stability. A policymaker cares about classification, benefits, worker voice, and platform rules.

This distinction matters because work models require different support systems. Professional service freelancers usually benefit from better proposals, retainers, project documentation, invoicing discipline, and client qualification. Platform-based freelancers often depend on marketplace ranking, review quality, category demand, and payment-release rules. Creator-style freelancers need audience development, licensing, recurring digital products, and rights management. Treating all of these models as the same gig economy hides the actual business problem. The question is not only how many freelancers exist, but which operating model gives workers the best chance to turn project income into durable independent businesses.

Freelance business models and their risk profile

Solo consultants usually carry the highest strategic value when they sell judgment, diagnosis, implementation support, or specialized expertise. Their risk is not only finding clients; it is avoiding a pipeline that depends on one or two large accounts.

Platform marketplace workers benefit from built-in discovery, reviews, payments, and buyer traffic, but they may face stronger price comparison, platform-rule changes, and fee pressure. For this group, the path to better income often depends on moving from commodity tasks toward repeat buyers and premium project categories.

Technical specialists, designers, analysts, and automation experts can often create more pricing power when they package work around measurable outcomes. A freelancer who can reduce reporting time, improve conversion, automate a workflow, or support a product launch is easier to value than a freelancer who only lists a task.

Creator-led freelancers operate differently again. Their income may come from services, sponsorships, products, subscriptions, teaching, or community access. That model can scale beyond hours, but it also requires audience trust, content consistency, and platform-risk management.

Freelance Platforms, Marketplaces, and Client Demand

Platform statistics show how freelance work is being packaged and sold. A marketplace may grow revenue even if buyer count declines, because spend per buyer rises, take rates change, services revenue expands, or larger transactions replace smaller gigs. These details matter because they reveal whether platforms are still mainly task marketplaces or moving toward higher-value project infrastructure.

Marketplace data should be read as demand infrastructure, not as the whole freelance economy. Many high-value freelancers never rely primarily on public platforms; they build direct referral networks, agency partnerships, corporate procurement relationships, or niche communities. At the same time, platform data is still useful because it shows how buyers are behaving at scale: how much they spend, whether larger projects are growing, and whether services revenue is moving beyond small one-off gigs.

Marketplace operating benchmarks

• Upwork reported $769.3 million in full-year 2024 revenue, up 12% year over year.

• Upwork reported 832,000 active clients at the end of 2024.

• Upwork reported $4,815 in gross services volume per active client in Q4 2024.

• Upwork revenue grew 19% year over year to $190.9 million in Q1 2024.

• Upwork marketplace take rate was 17.7% in Q1 2024, compared with 14.7% in Q1 2023.

• Upwork active clients grew 5% year over year to more than 872,000 in Q1 2024.

• Upwork Q2 2024 revenue grew 15% year over year to $193.1 million.

• Fiverr reported $430.9 million in total revenue for full-year 2025.

• Fiverr’s 2025 revenue grew 10.1% year over year, accelerating from 8.3% in 2024.

• Fiverr reported $297.5 million in 2025 marketplace revenue and $133.4 million in services revenue.

• Fiverr services revenue increased 50.9% year over year in 2025.

• Fiverr’s marketplace was driven by 3.1 million annual active buyers in 2025.

• Fiverr’s annual spend per buyer reached $342 in 2025.

• Fiverr’s marketplace take rate was 27.7% in 2025.

• Fiverr reported gross merchandise value from transactions over $1,000 grew 22.8% year over year.

• In 2024, Fiverr active buyers declined from 4.0 million to 3.6 million, but spend per buyer rose from $278 to $302.

The platform story is mixed in a useful way. Upwork’s client base and revenue growth show enterprise and professional-services demand, while Fiverr’s higher spend per buyer and growth in larger transactions suggest a shift from very small gigs toward more complex purchases. For freelancers, that means platform success depends less on simply being listed and more on positioning, specialization, repeat buyers, proof of work, and the ability to package higher-value outcomes.

For buyers, the platform question is also a quality-control question. A marketplace can reduce search time, but it does not automatically solve scope clarity, realistic budgeting, or project management. The strongest client-side use cases happen when a company can define the deliverable clearly, compare freelancer evidence, set milestones, and approve work without excessive back-and-forth. The weakest cases happen when a buyer treats a vague business problem as a simple task listing. That is why platform metrics should be paired with project success indicators such as repeat-hire rate, revision frequency, delivery time, dispute rate, and post-project business outcome.

Regional and Country Freelance Economy Statistics

Regional statistics are essential because the freelance economy does not develop the same way everywhere. In the United States, broad independent-work surveys show large participation. In the United Kingdom, solo self-employment has a large economic contribution. In the European Union, self-employment share has declined in some measures even while client-diversification indicators remain strong. In India and South Asia, gig work is tied closely to digital platforms, youth employment, and labor-policy reform.

Regional comparisons should not be treated as a ranking of which country is “best” for freelancing. They show different maturity patterns. The United States has a large independent-work participation base and significant high-income independent activity. The United Kingdom and Europe have deep self-employment and contractor markets shaped by tax, benefits, and regulation. South Asia and Southeast Asia are important because online platforms, remote delivery, English-language services, and IT-enabled work make cross-border freelancing more visible.

United States

The U.S. numbers are valuable because they show both participation and earning potential. Large headcount, high aggregate earnings, and a growing six-figure independent segment make the U.S. market useful for studying freelance work as a serious business model. The risk is that broad participation data can hide very different experiences between high-skill consultants, creative professionals, gig workers, and occasional side earners.

• The U.S. had 64 million freelancers in 2023 and 72.7 million independent workers in MBO’s 2024 broader estimate.

• BLS counted 11.9 million main-job independent contractors in July 2023.

• A Fiverr/Illuminas metro report cited by Axios placed independent professionals at 4.1% of the U.S. labor force.

• Phoenix’s freelance workforce increased 23% from 2018 to 2023.

• Phoenix freelancers’ incomes rose 42% from 2018 to 2023.

• Phoenix freelancers earned an estimated average of $45,884 in 2023.

• In Phoenix, 71% of freelancers worked solely as freelancers in 2023, up from 61% in 2021.

• Boston ranked as the 10th-largest U.S. metro for freelancers, with an estimated 132,348 freelancers in 2023.

• Boston had 67,786 professional-services freelancers and 41,302 technical-services freelancers in the referenced metro report.

• San Diego had approximately 83,000 independent professionals in 2023, with average freelance earnings of $47,310.

• Axios coverage says 55% of U.S. freelancers expected increased earnings in the coming year.

United Kingdom and Europe

European and UK benchmarks are especially useful for policy and classification. They show how self-employment interacts with benefits, tax rules, client concentration, and worker protection. For businesses, this makes compliance and contract design as important as price. For freelancers, it makes client diversity and clear scope part of risk management.

• IPSE reported the UK solo self-employed contributed £366 billion to the UK economy in 2024.

• That contribution increased from £331 billion in 2023 to £366 billion in 2024, a gain of about £35 billion.

• The UK solo self-employed contribution grew by roughly 10.6% year over year.

• IPSE reported the number of UK side hustles increased by 20% since 2023.

• Working mums accounted for 21% of all UK side hustles in the IPSE report.

• Eurostat says the EU self-employed share decreased by 1.6 percentage points between 2015 and 2025.

• Eurostat says the euro-area self-employed share decreased by 1.2 percentage points over the same period.

• Eurostat reported 61.2% of EU self-employed persons had more than nine clients in the last 12 months.

• Spain had 75.9% of self-employed persons with more than nine clients, while Belgium had 74.1%.

• Foreign-born self-employment across 37 OECD countries averaged 13.8%, compared with 13.4% for native-born workers.

India, South Asia, and online platform markets

South Asia matters because freelance work is closely connected to global delivery. India, Pakistan, and the Philippines show how remote services, platform visibility, and digital-payment access can connect local talent to international demand. The opportunity is export-oriented income; the risk is price competition, platform dependence, and exchange-rate or payment friction.

• Reuters reported India’s gig workforce was expected to be around 10 million in 2024/25.

• India’s gig workforce is projected to reach 23.5 million by 2030 in the cited policy-research coverage.

• Grand View Research estimates India’s freelance-platform market at $265.1 million in 2025.

• India’s freelance-platform market is projected to reach $1.54 billion by 2033.

• India’s platform forecast implies a 25.1% CAGR from 2026 to 2033.

• The ILO says self-employed workers and micro-enterprises account for more than 80% of employment in South Asia.

• Filipino online freelancers are commonly estimated at around 1.5 million across platform-focused sources.

• Payoneer says 55% of Filipino freelancers are between ages 21 and 35.

• Payoneer says 69% of Filipino freelancers run businesses while also taking gigs.

• Pakistan appeared in Payoneer-linked fastest-growing freelance earnings coverage with 47% growth.

• Payoneer lists the top freelancing countries as the U.S., U.K., Brazil, Pakistan, Ukraine, Philippines, India, Bangladesh, Russia, and Serbia.

The regional pattern is important: freelance work is not one global labor market with one wage structure. The U.S. data emphasizes workforce participation and high-earning independents. UK data emphasizes economic contribution. EU data highlights self-employment structure and client diversification. India and South Asia show how platform growth, youth employment, and labor-policy recognition are becoming central to the freelance economy.

Regional differences also change the meaning of the same headline statistic. A country with high platform participation may be exporting digital services because local wages are lower, English-language capability is strong, or international demand is easier to reach online. A mature market with high self-employment may reflect professional independence, consulting, and portfolio careers rather than platform task work. Policy also matters: tax rules, labor protections, benefits access, payment infrastructure, and cross-border settlement costs all shape whether freelancing feels like entrepreneurship, temporary work, or income patching.

Figure 2. Regional freelance statistics should compare workforce scale, platform growth, economic contribution, and client diversification rather than relying on a single global average.

AI, Skills, and the Shift Toward Higher-Value Projects

AI is changing the freelance economy in two ways at once. First, it increases demand for workers who can build, apply, prompt, review, automate, or integrate AI workflows. Second, it raises the bar for routine work because clients may expect faster turnaround, broader tool fluency, and clearer business outcomes. The strongest AI-related freelance data is therefore less about hype and more about changing project mix.

The most important AI question is not whether freelancers will use AI tools. Many already do. The better question is where AI changes the value of the human contribution. Routine production can become faster and cheaper, but clients still need judgment, quality control, context, workflow design, compliance awareness, brand fit, and accountability. Freelancers who combine AI fluency with domain expertise are better positioned than freelancers who only use AI to complete the same low-differentiation tasks faster.

Skill-demand and project-value benchmarks

• Upwork data reported by Axios found freelance earnings from AI-related jobs were up 25% year over year.

• Fiverr reported GMV from transactions over $1,000 grew 22.8% year over year, suggesting more platform demand for larger or more complex projects.

• Fiverr said the number of buyers spending more than $10,000 annually accelerated 7%.

• Fiverr services revenue grew 50.9% in 2025, showing monetization beyond simple marketplace transactions.

• MBO summaries placed independent creators at 10.1 million, giving the freelance economy a significant creator-economy overlap.

• Independent creators rose 13% to 10.1 million in the referenced MBO summary.

• One 2025 MBO summary placed Gen Z at 28% of the independent workforce, up from 21% in 2024.

• The same summary placed Millennials at about 34% of independent workers and Gen X at about 27%.

• Baby Boomers fell to about 11% of the independent workforce after being 19% in 2023 in the referenced summary.

• NITI Aayog-related coverage said AI could generate up to 4 million new jobs in India by 2030.

For businesses, this means freelance hiring briefs should become more specific. Instead of asking for generic content, design, data, or automation help, teams should define the business problem, the tools already in use, the quality standard, and the decision the work needs to support. For freelancers, the same shift means portfolios should prove problem-solving ability, not only output volume.

AI does not remove the need for freelancers; it changes what freelancers need to prove. Clients are likely to value specialists who can combine domain knowledge, speed, data judgment, and quality control. For many freelancers, the practical question is no longer whether AI tools exist, but whether their services can be packaged as measurable outcomes that save time, improve content quality, automate workflows, or support better decisions.

The more useful AI question is not whether AI removes freelance work, but which parts of freelance work become more valuable. Routine drafting, simple image variations, basic research collection, and low-complexity coding can become cheaper when AI tools are widely available. But clients still need people who can set direction, check quality, adapt outputs to brand or business constraints, and take responsibility for the final result. This is why the strongest freelancers are likely to combine tool fluency with judgment: they use AI to produce faster, but sell clarity, reliability, taste, technical accuracy, and business understanding.

Client Acquisition, Diversification, and Income Resilience

Freelance stability often depends less on the number of projects completed and more on the quality of demand. A freelancer with one large client may appear successful but carry concentration risk. A freelancer with many small clients may have better diversification but higher marketing and administrative burden. The strongest statistics therefore look at client count, international reach, promotion channels, and rate-setting power.

This section is important because client acquisition is the hidden cost of freelancing. A worker may charge a strong hourly rate but lose income if too many hours go into proposals, unpaid calls, platform bidding, revisions outside scope, or chasing late payments. A healthy freelance business usually has more than demand; it has a repeatable way to convert demand into paid, scoped, collectible work.

Client and resilience benchmarks

• Eurostat reported 61.2% of EU self-employed persons had more than nine clients in the last 12 months.

• Spain’s self-employed client-diversification rate was 75.9%, while Belgium’s was 74.1%.

• Payoneer reported 32% of freelancers expanded their client base into new countries.

• Payoneer reported 74% of freelancers use social media to promote services, up from 65% two years earlier.

• That social-media-promotion increase represents a 9 percentage-point gain.

• Payoneer reported 21% of freelancers use Instagram to promote freelance services.

• In Phoenix, 29% of freelancers also had a traditional job, showing that blended income remains part of the market.

• In the Phoenix report, 76% of Gen Z freelancers said they were at least somewhat likely to raise rates, compared with 49% of freelancers overall.

• Payoneer’s 32% international-client expansion benchmark points to cross-border demand as a practical growth lever.

• World Bank research notes online gig work can provide opportunities for women, youth, migrants, people with disabilities, and lower-skilled workers, but access and protection vary by market.

For freelancers, these numbers point to an operating model: build repeatable demand, reduce dependence on one platform or one client, track conversion by channel, and separate high-margin specialized work from low-margin volume work. For businesses, the lesson is that freelance talent pools are more reachable than before, but quality hiring still depends on clear scopes, evaluation criteria, payment reliability, and strong onboarding.

The healthiest freelance businesses usually reduce dependence on any single channel. Platform marketplaces can provide visibility, but they can also change ranking rules, fees, category demand, and buyer behavior. Referrals can be high-quality, but they may not scale predictably. Social media can create reach, but attention is volatile. A durable freelancer often blends several acquisition paths: repeat clients, referrals, direct outreach, content, community visibility, partnerships, and selective marketplace use. This is why acquisition statistics should be interpreted as portfolio data. The objective is not to use every channel; it is to avoid having all future income depend on one algorithm, one client, or one seasonal demand spike.

What durable freelancers track beyond revenue

• Client concentration: how much revenue depends on the largest one, two, or three clients.

• Effective hourly income: total collected income divided by all working hours, including sales, admin, revisions, and payment follow-up.

• Repeat-client share: the percentage of revenue coming from existing relationships instead of one-time projects.

• Proposal conversion: how often qualified leads turn into paid work, and which channels produce the best clients.

• Payment reliability: days to payment, overdue invoices, disputed invoices, and the share of income collected without follow-up.

These metrics turn freelance statistics into a practical operating system. The freelancer who tracks only revenue may miss early signs of risk. The freelancer who tracks concentration, repeat demand, effective income, and collection speed can usually make better decisions about pricing, positioning, and which clients to keep.

Governance, Risk, and Worker Protection Statistics

Freelance growth creates policy questions because independent work does not always fit neatly into traditional employment systems. Some workers value flexibility and control, while others face income volatility, weak benefits, unclear platform rules, or limited protections. The governance statistics do not weaken the freelance economy story; they make it more realistic.

The governance conversation is not only about whether freelancing is good or bad. It is about matching work flexibility with fair rules, payment security, transparent platform policies, tax clarity, and protection against misclassification. Independent workers often value autonomy, but autonomy is weaker when payment is unreliable, platform rules are opaque, or a worker depends on one buyer without employee protections.

Policy and protection benchmarks

• Reuters reported India consolidated 29 older labor laws into four labor codes.

• Reuters noted India’s labor reforms included legal recognition and protections for gig and platform workers.

• Karnataka’s gig-worker bill establishes a Welfare Board and a Gig Workers Welfare Fund.

• The UK government warned some gig-economy firms they may be operating illegally under employment-agency or self-employment rules.

• The World Bank report states many gig workers are not protected against unfair practices, abuse, or injuries depending on local labor regulations.

• The ILO says almost seven in 10 workers worldwide are self-employed or work in small businesses.

• ILO data shows global self-employed workers remained above roughly 1.48 billion in recent years.

• ILO tables place the recent global self-employed share around the mid-40% range of total employment.

• World Bank metadata defines self-employed workers as employers, own-account workers, cooperative members, and contributing family workers.

The control issue is not whether freelancing is good or bad. It is whether the work model has enough transparency, payment security, dispute handling, benefits planning, tax clarity, and legal recognition for the people who depend on it. Countries with fast platform growth may need stronger rules around classification, insurance, earnings transparency, data access, and worker representation as the market matures.

For businesses, governance also means knowing when a freelancer relationship is no longer casual. A contractor who handles sensitive data, uses internal systems, manages client-facing deliverables, or works with the same team for months needs clearer access rules, documentation, confidentiality terms, payment terms, and performance expectations. For workers, governance shows up as contract clarity, scope protection, tax planning, insurance, and payment enforcement. The risk statistics are therefore not separate from the market statistics. As freelance work becomes larger and more professional, the need for better operating rules grows with it.

Freelance Economy Metrics Leaders Should Track

A strong freelance scorecard should measure more than headcount. Businesses using freelancers need to know whether independent talent improves speed, cost control, specialization, and project quality. Freelancers need to know whether their work mix is becoming more resilient or simply more fragmented. Marketplaces need to know whether growth comes from more buyers, larger projects, higher spend per buyer, or higher take rates.

| Metric | What it measures | Why it matters |

|---|---|---|

| Freelance participation rate | Freelancers as a share of the workforce, such as 38% in Upwork’s U.S. 2023 benchmark. | Shows how widely freelance work has spread across the labor market. |

| Main-job contractor rate | Official independent contractors as a share of employment, such as BLS’s 7.4% figure. | Creates a narrower labor-classification baseline. |

| Annual freelance earnings | Total earnings, such as $1.27T in U.S. freelance earnings. | Measures economic scale, not just worker count. |

| High-earner count | Workers above a threshold such as $100K annually. | Separates professional independent work from occasional gigs. |

| Average hourly rate | Benchmarks such as $23/hour, $28/hour, or $44/hour by region. | Helps compare income quality across skills and locations. |

| Client concentration | Share of freelancers with multiple clients, such as EU’s 61.2% with more than nine clients. | Shows resilience and dependence risk. |

| Platform buyer quality | Spend per buyer, active buyers, and high-value transactions. | Shows whether marketplace demand is moving upmarket. |

| Cross-border demand | Share expanding into new countries, such as Payoneer’s 32% benchmark. | Shows whether freelancers can escape local demand limits. |

| AI-related earnings | Growth in AI freelance earnings, such as 25% year over year. | Reveals where project demand is changing fastest. |

| Worker-protection maturity | Legal recognition, welfare funds, dispute systems, and platform rules. | Shows whether market growth is matched by stronger safeguards. |

The most useful freelance metrics combine scale with quality. A market can add workers but lower average earnings. A platform can lose buyers but increase spend per buyer. A freelancer can raise rates but become more dependent on one client. A company can cut hiring costs but increase coordination risk. The best scorecards track both opportunity and fragility.

Figure 3. Freelance economy scorecards should combine workforce scale, income quality, platform demand, client diversification, and risk signals.

Practical Freelance Economy Business Case

Consider a mid-sized company that needs design, analytics, content, automation, and customer-support expertise but does not need every skill full time. The freelance economy lets the company buy specific outcomes instead of adding permanent headcount for every project. The upside is flexibility and access to specialized talent. The risk is fragmented scopes, weak knowledge transfer, inconsistent quality, and payment or compliance friction if freelance work is not managed as a system.

Planning benchmarks for businesses and freelancers

• Use the 11.9M, 64M, and 72.7M U.S. benchmarks as separate lenses: main-job contractors, freelancers, and broader independent workers.

• Use the 154M-435M World Bank online gig range for global platform talent planning, not for direct comparison with one-country surveys.

• Treat the $6.37B-to-$24.16B freelance-platform forecast as evidence of investment in matching, trust, payments, and project infrastructure.

• Compare average hourly-rate benchmarks by region: $44/hour in North America and $31/hour in Western Europe in the cited Payoneer data.

• Track whether freelance spending is concentrated in small tasks or larger projects; Fiverr’s 22.8% growth in transactions above $1,000 is a useful upmarket signal.

• For freelancers, track rate changes against workload. If 55% of freelancers take on more work because of cost pressure, more projects may not mean a healthier business.

• For marketplaces, compare buyer count with spend per buyer. Fiverr’s 2024 data showed active buyers down to 3.6M while spend per buyer rose to $302.

• For regional expansion, treat India’s 25.1% platform CAGR forecast and the UK’s £366B solo self-employed contribution as different types of opportunity signals.

The practical business case is strongest when freelance work is planned around repeatable scopes, defined outcomes, clean payment workflows, and reliable performance measures. The weakest freelance programs treat every project as a one-off transaction. The strongest ones build a bench of trusted specialists, document handoffs, track project success, and know when a task should remain freelance versus become a permanent role.

Research Depth and Methodology Notes

Freelance economy research needs more caution than many software or payments topics because the market is defined by work arrangements rather than a single product category. A platform-revenue forecast, a national labor survey, a freelancer-income survey, and a self-employment table can all be accurate while describing different populations.

How to read the statistics responsibly

• Use official labor data, such as the 11.9 million BLS independent-contractor figure, when the goal is labor-market classification.

• Use survey-based participation data, such as Upwork’s 64 million freelancers, when the goal is understanding how many people perform freelance work during the year.

• Use broader independent-worker estimates, such as MBO’s 72.7 million, when the goal is understanding the full independent-work ecosystem.

• Use the World Bank’s 154 million to 435 million range when discussing global online gig platforms, but avoid comparing it directly with a single-country freelance survey.

• Use platform-revenue statistics, such as the $6.37 billion freelance-platform market, to measure marketplace infrastructure rather than worker income.

• Use rate benchmarks, such as $23/hour, $28/hour, and $44/hour, as directional comparisons because rates vary by skill, geography, platform fees, project type, and client quality.

• Use regional data carefully because EU self-employment trends, UK solo self-employed contribution, U.S. freelance participation, and India platform-market growth each describe a different labor-market structure.

The strongest conclusion is not that one source is right and another is wrong. The stronger conclusion is that freelance work now has multiple measurable layers. Participation tells one story, earnings tell another, platform revenue tells another, and worker protection tells another. A useful statistics report keeps those layers separate, then explains where they reinforce each other and where they point to risk.

How to Use Freelance Economy Statistics in Planning

Freelance economy statistics are most useful when they turn into practical decisions. A business can use them to decide whether to build a contractor bench, create preferred-vendor processes, improve onboarding, or budget for specialist talent. A freelancer can use them to benchmark pricing, identify stronger skill categories, choose acquisition channels, and decide whether a platform, direct-client, or hybrid model fits their goals. The numbers are not just proof that independent work is large; they are signals about where demand, risk, and operating complexity are moving.

Planning questions for businesses

• Which work is project-based, specialized, or seasonal enough to be better handled by freelancers than permanent hires?

• Which freelance roles need vendor-style onboarding because they touch customer data, financial information, brand assets, or internal systems?

• Which projects are likely to become recurring enough that the business should build a preferred contractor pool instead of starting from scratch each time?

• Which metrics will prove success: faster delivery, lower fixed payroll risk, access to rare skills, better creative output, or more flexible capacity?

Planning questions for freelancers

• Which income source is most reliable: repeat clients, referrals, direct outreach, public content, a marketplace profile, or a mix of several channels?

• Which services have enough demand and pricing power to support a sustainable business after taxes, software, unpaid sales time, and payment delays?

• Which tasks can be productized into fixed-scope offers, retainers, templates, audits, or packages so income is not tied only to hourly availability?

• Which risks need a system: late payment, scope creep, client concentration, weak contracts, inconsistent pipeline, or underpriced administrative work?

The strongest planning approach combines external benchmarks with internal records. Businesses should compare freelance spending against project outcomes, delivery speed, revision rates, and repeat-hire quality. Freelancers should track income by client, project type, source channel, effective hourly rate, unpaid admin time, and payment speed.

FAQ

How many freelancers are there in the United States?

Upwork reported 64 million U.S. freelancers in 2023, equal to 38% of the workforce. MBO’s broader independent-worker estimate was 72.7 million adults in 2024. BLS reported a narrower official benchmark of 11.9 million people whose sole or main job was independent contracting in July 2023.

How big is the global online gig workforce?

The World Bank estimates 154 million to 435 million people work through online gig platforms worldwide. That range equals about 4.4% to 12.5% of the global labor force, depending on the estimate and activity definition used.

How much do freelancers contribute to the economy?

Upwork reported U.S. freelancers contributed $1.27 trillion in annual earnings in 2023. In the UK, IPSE reported solo self-employed workers contributed £366 billion to the economy in 2024.

Are freelancers earning more?

The answer depends on the segment. MBO reported 5.6 million independent workers earning more than $100,000 annually in 2025, but Payoneer also reported 55% of freelancers took on more work because of cost pressure. The market contains both high-income specialists and workers using freelancing to manage financial strain.

How fast is the freelance-platform market growing?

Grand View Research values the global freelance-platforms market at $6.37 billion in 2025 and projects $24.16 billion by 2033, an 18.6% CAGR from 2026 to 2033.

How is AI affecting freelance work?

Upwork data reported by Axios found AI-related freelance earnings rose 25% year over year. The practical effect is not only automation; it is also stronger demand for workers who can apply AI tools to content, software, analytics, operations, marketing, and workflow improvement.

Final Takeaway

Freelance economy statistics show a labor market that is large, global, and increasingly shaped by skills, platforms, remote demand, AI adoption, and independent income strategies. The strongest numbers are not simply the biggest counts. They are the comparisons that explain what kind of freelance work is being measured, whether income is durable, how clients find talent, which regions are supplying digital services, and where independent workers face the greatest business risk.

The premium lesson is that freelance growth should be judged by quality as well as scale. A healthy freelance economy produces clearer paths to reliable income, stronger client diversification, better payment systems, higher-value skills, and fairer protections. Businesses should use the statistics to build smarter contractor systems, and freelancers should use them to measure whether they are building a real independent business rather than only completing more projects.