Small-business payment performance is not just a question of whether customers can pay by card. It is the set of everyday decisions that determines how quickly revenue turns into usable cash, how much of each payment is lost to fees, how clearly invoices are understood, and how much time the owner spends chasing money that has already been earned.

The data points to a more complicated payment reality than a simple shift from cash to digital. Checks remain the most widely accepted payment form in Federal Reserve small-business payments research, while cards, cash, ACH, and mobile payments all hold meaningful places in the stack. At the same time, QuickBooks research shows how unpaid invoices turn payment delays into working-capital pressure for many U.S. small businesses.

The most useful numbers explain practical decisions: which payment methods to offer, which terms create collection work, why fees and slow pay should be tracked separately, and how billing quality helps prevent confusion before it becomes a cash-flow problem.

Executive Payment Benchmarks

These benchmarks frame the payment conversation. They show that small-business payments are pulled in several directions at once: customers want convenience, owners want predictable cash flow, finance teams want clean records, and every extra payment method adds both opportunity and operational work.

The numbers that define the small-business payment problem

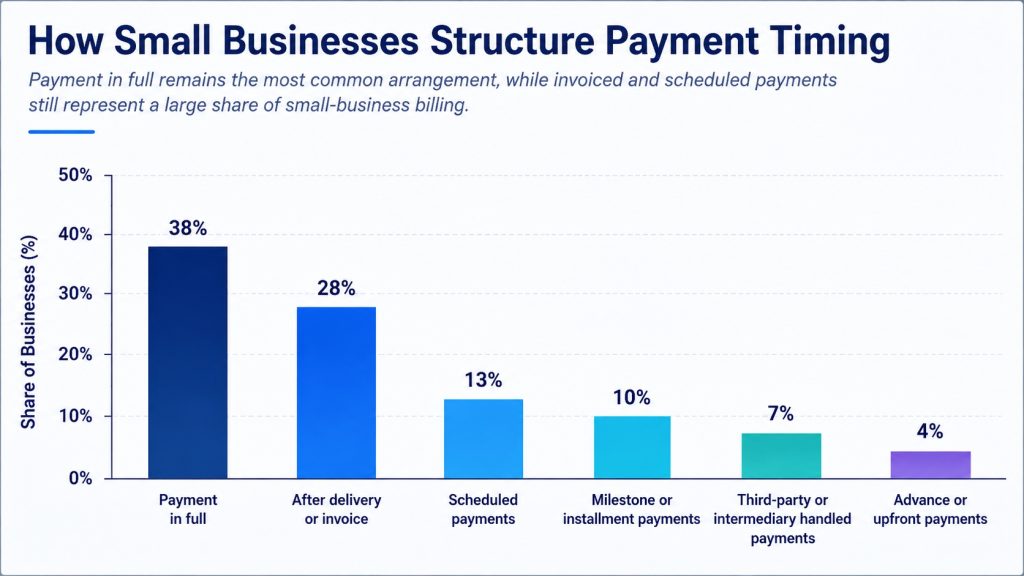

• In Federal Reserve small-business payments research, payment in full at the moment of purchase or service is the leading revenue arrangement for 38% of employer firms, which explains why point-of-sale convenience still matters across broader payment operations.

• Invoice-led and after-delivery billing is nearly as important, with 28% of employer firms saying that payment after product or service delivery produces their largest share of revenue.

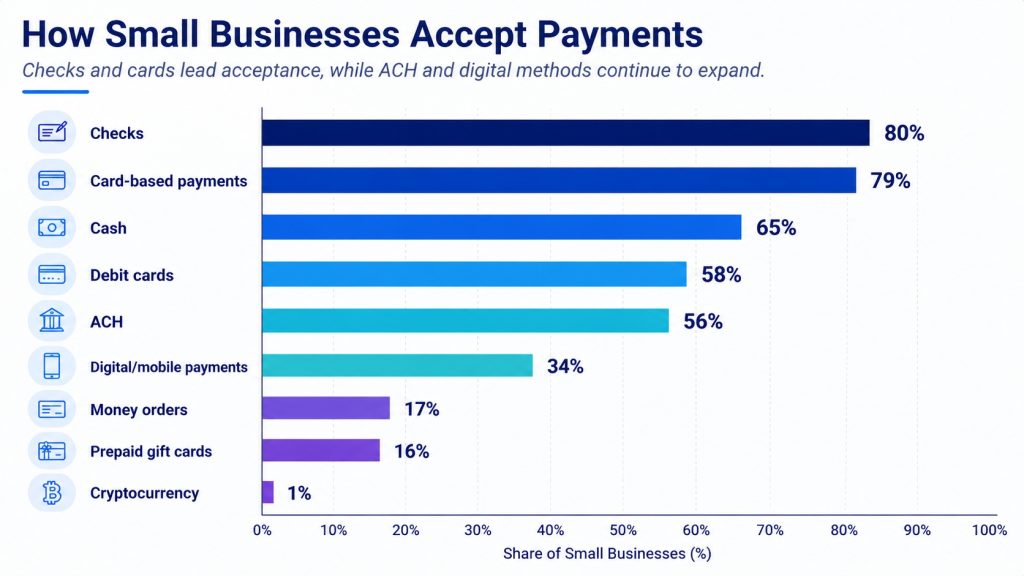

• Checks remain the most widely accepted method, used by 80% of employer firms, so paper-based or check-like collection workflows are still part of real small-business operations.

• Card acceptance is almost as common as check acceptance when grouped broadly; 79% of firms accept at least one card-based option, including credit cards, debit cards, or digital/mobile card payments.

• Cash has not disappeared from small-business payment behavior. A 65% acceptance level keeps cash relevant for local service, retail, food, repair, and other face-to-face environments.

• ACH acceptance, at 56%, shows that bank-based digital payment is already mainstream enough to matter for recurring, invoice-led, and B2B relationships.

• Digital or mobile payments are accepted by 34% of firms, a meaningful share but still far below checks, cards, cash, and ACH.

• Payment-processing fees are the most common listed payment challenge, cited by 52% of employer firms in the Federal Reserve data.

• Collection speed is the second major pressure point: slow-paying customers are cited by 39% of employer firms, while QuickBooks research found that 56% of U.S. small businesses were owed money from unpaid invoices.

• Among businesses with unpaid invoices in the QuickBooks research, the average amount outstanding was $17,500, which makes late payment a working-capital issue rather than a minor back-office annoyance.

Editorial readout The executive numbers tell a practical story. Small businesses are not choosing between old payments and new payments; they are managing a mixed environment. A good payment strategy has to protect convenience at the point of sale, make invoice collection easier, limit fee drag, and keep records clean enough that owners can see what has been paid, what is pending, and what needs follow-up.

Why Small Business Payments Matter Beyond the Transaction

A payment can look successful from the customer side while still creating problems for the business. The card may clear but carry higher fees than expected. A check may arrive but take staff time to deposit and match. An invoice may be approved but sit unpaid for weeks. A mobile payment may be easy for the customer but fragmented for bookkeeping if it does not flow cleanly into accounting records.

That is why small-business payment statistics should be read as operating data. They are not simply a ranking of preferred methods. They show where revenue gets slowed, where administrative work accumulates, and where customers and owners may value different things. Customers often notice speed and convenience first. Owners often notice net cash, settlement timing, fees, and whether a payment can be reconciled without a long search through emails, bank deposits, or receipts.

The broader small-business context makes these details important. The SBA profile used for the research base counts 36.2 million small businesses in the United States, representing 99.9% of U.S. businesses and supporting 62.3 million employees. When payment delays or fee pressure affect even a slice of that market, the issue is not abstract. It touches payroll, supplier timing, inventory decisions, and owner confidence.

Small-business context benchmarks

• The SBA profile shows small businesses accounting for 45.9% of U.S. employees, which is why payment stability has a labor-market dimension, not only a bookkeeping dimension.

• During the measured period, small businesses contributed 88.9% of the net job increase reported in the SBA profile, making reliable cash collection part of a broader growth story.

• Small-business establishment churn also matters: the profile reports 1.1 million small-business establishment openings and 982,940 closings from March 2023 to March 2024.

• Bank loans to businesses with revenue of $1 million or less reached $84.2 billion in 2023, which reinforces the link between payments, borrowing, working capital, and resilience.

• Only 20% of employer firms in the Federal Reserve survey reported no listed payment challenges, meaning most firms are dealing with at least one friction point in how money is collected or processed.

How to use the payment-challenge data

A small business does not need every new payment product. It needs a payment system that fits the way it earns money. That means measuring more than acceptance: days to collect, method-level fees, late invoices, settlement delay, refund friction, dispute documentation, and the time required to connect each payment to the right customer record.

How Small Businesses Accept Payments

The payment mix begins with what firms actually accept. Acceptance data is useful because it reveals the practical infrastructure behind small-business sales: terminals, invoices, bank transfers, cash drawers, payment links, mobile wallets, deposit routines, and accounting workflows. The strongest small-business payment stack is usually not the one with the most options. It is the one where the available options match customer behavior and do not overwhelm the back office.

Payment acceptance benchmarks

• Checks still sit at the top of the acceptance list in the Federal Reserve data, with 80% of employer firms accepting them somewhere in the business.

• Credit cards are close behind checks. A 74% acceptance rate makes credit cards a normal part of small-business selling rather than a premium add-on.

• Cash remains part of everyday collection for 65% of employer firms, especially where transactions are local, face-to-face, urgent, or low-ticket.

• Debit cards appear at 58% acceptance, putting debit slightly ahead of ACH in broad availability even though ACH may be more important in recurring or higher-value billing relationships.

• ACH acceptance reaches 56%, giving many small businesses a bank-based digital option that can support invoices, subscriptions, retainers, and recurring services.

• Digital and mobile payments appear at 34% acceptance. That share is meaningful, but it also suggests a gap between consumer mobile-payment habits and what many small firms are ready to support operationally.

• Money orders and prepaid gift cards remain visible but niche options, accepted by 17% and 16% of employer firms respectively.

• Cryptocurrency is not yet a normal small-business payment method in this data, with acceptance at 1% of employer firms.

The most important finding is not that one method wins. It is that mixed acceptance is already normal. When the Federal Reserve buckets are combined, 81% of firms accept three or more payment forms, while 39% accept five or more. That breadth creates customer choice, but it also creates reconciliation work. Each method needs a clean path from customer intent to payment confirmation, receipt, deposit, and accounting record.

Figure 1. Small-business payment acceptance is still mixed: checks, cards, cash, ACH, and mobile payments all serve different operating needs.

Payment Terms Change the Payment Stack

Payment acceptance becomes more useful when it is connected to payment terms. A firm paid in full at the point of sale needs a different operating setup from a firm that invoices after delivery. A business with retainers, installments, insurance reimbursement, financing, or project milestones may need payment tools that make status, approvals, and timing easier to track.

This distinction matters because payment-method advice is often too generic. A restaurant, a contractor, a consultant, and a clinic may all be small businesses, but the moment when money is collected is different. Payment in full prioritizes speed. After-delivery billing prioritizes receivables discipline. Scheduled billing prioritizes automation. Installments prioritize clear milestones. Third-party payment prioritizes settlement tracking and reconciliation.

Payment-term benchmarks

• Payment in full at the time of service or purchase is the leading revenue arrangement for 38% of employer firms in the Federal Reserve research.

• After-delivery billing, including invoice or net-term arrangements, produces the largest revenue share for 28% of firms, which makes collection workflow central to a large part of the small-business market.

• Scheduled payment arrangements lead for 13% of firms, a pattern that often benefits from recurring invoices, stored authorization, and predictable follow-up.

• Project milestone or installment payment is the leading arrangement for 10% of firms, which makes estimate approval, deposits, progress billing, and change-order clarity more important.

• Third-party payment arrangements such as insurance, lender financing, or buy now, pay later lead for 7% of firms, but those firms may face more settlement and reconciliation complexity.

• Payment in advance is the leading arrangement for 4% of firms, a smaller overall share but an important model in reservations, tickets, bookings, classes, events, and limited-capacity services.

The method mix shifts sharply across those arrangements. Businesses paid immediately at sale lean heavily toward cards and cash. Invoice-led businesses show much stronger check and ACH usage. Scheduled and milestone models often sit between those worlds. Third-party arrangements can make ACH unusually important because settlement may move through an intermediary rather than directly from the customer at checkout.

• Among firms paid in full at sale, card-payment acceptance reaches 93%, while cash acceptance sits at 85% and check acceptance at 65%.

• For firms relying on payment after delivery or invoicing, checks are accepted by 95%, while cards are accepted by 80% and ACH by 51%.

• Set-schedule service firms show a hybrid pattern, with 84% accepting checks, 75% accepting cards, and 66% accepting ACH.

• Milestone and installment firms are similarly blended, with check acceptance at 91% and card acceptance at 90%. The operational lesson is that project billing usually needs both customer convenience and strong records.

• For businesses using third-party payment arrangements, ACH acceptance reaches 80%, higher than card, cash, or check acceptance in that arrangement.

Figure 2. Payment terms change which payment methods matter most, especially for invoice-led, scheduled, and third-party payment models.

Industry Payment Patterns Are Not Interchangeable

Small-business payment statistics become more useful when they are segmented by industry. Retail and hospitality often collect money at the moment of sale. Manufacturing and professional services often bill after delivery. Healthcare and education can include upfront payments, scheduled payments, third-party payment, and reimbursement. A payment option that is essential in one sector can be secondary in another.

That is why a payment benchmark should not be treated as a universal instruction. When a retail business sees high card and cash acceptance, that reflects customer-facing checkout pressure. When a professional-services firm sees high check and ACH acceptance, that reflects invoice approval, client finance processes, and back-office settlement. The same statistic can mean convenience in one sector and receivables discipline in another.

Industry payment pattern benchmarks

• Leisure and hospitality remains strongly point-of-sale oriented, with 79% of firms saying payment in full at sale produces the highest revenue share.

• Retail looks similar, with 76% of firms relying most heavily on payment in full at sale.

• Manufacturing is more invoice-driven; 53% of firms in that sector say payment after delivery produces the highest share of revenue.

• Professional services and real estate also lean toward after-delivery billing, with 41% identifying it as the leading revenue arrangement.

• Healthcare and education are more distributed, with payment in full, scheduled payments, and payment in advance each playing meaningful roles in the research split.

• Retail has one of the broadest customer-facing acceptance profiles, with card acceptance at 99% and cash acceptance at 94%.

• Leisure and hospitality follows the same immediate-payment logic, with 98% card acceptance and 91% cash acceptance.

• Professional services and real estate show a back-office payment pattern instead: 89% accept checks, 79% accept ACH, and 64% accept cards.

• Manufacturing also reflects B2B and invoice behavior, with 85% accepting checks and 75% accepting ACH.

Industry interpretation

The practical question is not which industry is more digital. The better question is where the payment happens in the customer journey. If payment happens at the counter, speed and card/mobile readiness dominate. If payment happens after delivery, invoice clarity, approval routing, reminders, ACH options, and reconciliation often matter more.

The Payment Challenges Small Businesses Report

Payment acceptance tells only half the story. Once a method is offered, the business has to absorb fees, wait for deposits, answer customer questions, prevent errors, manage refunds, and match the money back to the right invoice or sale. The challenge data shows that the pain points are not limited to one method. They cut across collection speed, administrative effort, risk, and margin.

Payment challenge benchmarks

• Processing fees are the most common payment challenge in the Federal Reserve small-business survey, cited by 52% of employer firms.

• Slow-paying customers create the next major pressure point, appearing in the data at 39% of firms.

• Billing work, bank deposits, and other time-consuming payment processes are not minor issues; 20% of firms cite them as a challenge.

• Settlement timing remains an operational concern, with 18% of firms reporting delays in settlement or funds availability.

• Managing multiple payment streams creates friction for 13% of firms, which is one reason payment flexibility has to be paired with reconciliation discipline.

• Fraud or theft is cited by 11% of firms, showing that risk exists even when it is not the top-ranked issue for most small businesses.

• Customer demand for more options appears at 7%, suggesting that owners often feel fee and collection pressure more directly than pure method-expansion pressure.

• Only 20% of firms report no listed payment challenges, which means four out of five firms are dealing with at least one issue from the survey list.

The ranking matters because it can keep owners from solving the wrong problem. If fees are the loudest pain point, adding more payment methods without reviewing fee impact may frustrate the business. If slow pay is the problem, the fix may be earlier invoicing, clearer terms, automatic reminders, deposits, or ACH authorization rather than a new checkout button. If billing work is consuming time, the payment method may be less important than the recordkeeping process around it.

Figure 3. Fees and slow-paying customers dominate the small-business payment challenge list, but settlement, billing work, fraud, and stream management also matter.

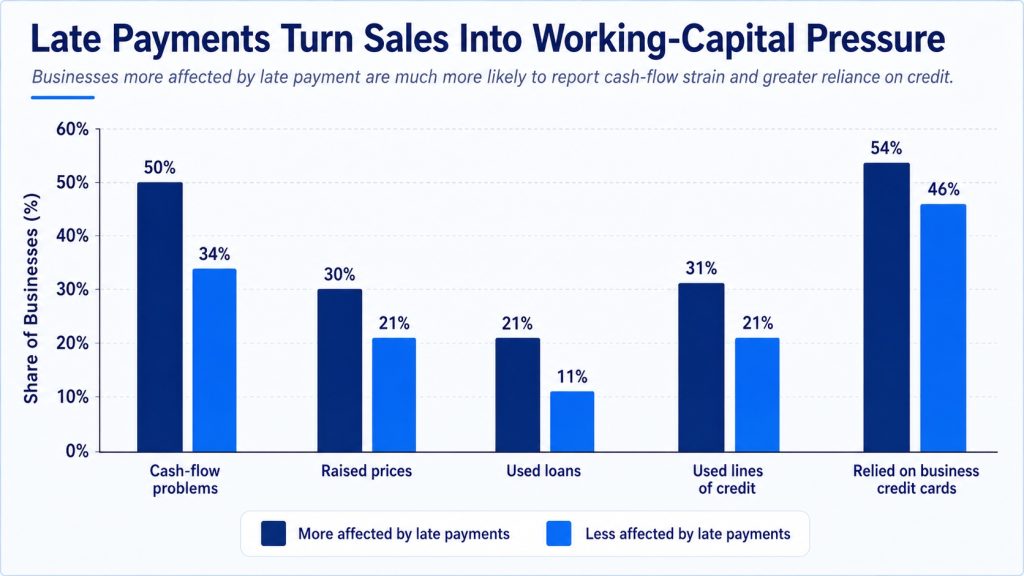

Late Payments Turn Sales Into Working-Capital Pressure

Late payment is where a sale stops feeling like revenue and starts behaving like a loan to the customer. The business may have completed the work, paid employees, bought materials, handled delivery, or paid software and financing costs, but the cash has not arrived. That timing gap can be enough to push owners toward credit cards, lines of credit, delayed hiring, price increases, or tighter customer terms.

The late-payment data is especially relevant for businesses that rely on invoices. A store that is paid at the counter has different risk from a service company that sends an invoice after the job. Once payment is separated from delivery, the business needs a process that makes the amount, due date, payment method, and approval path obvious to the customer.

Late-payment and working-capital benchmarks

• QuickBooks research found that 56% of U.S. small businesses were owed money from unpaid invoices, making receivables discipline a mainstream issue rather than a rare exception.

• Among businesses with unpaid invoices, the average amount owed was $17,500, enough to influence hiring, inventory, owner pay, or credit use for many small firms.

• Some invoices were overdue by 30 or more days at 47% of U.S. small businesses in the QuickBooks research.

• The average share of invoices overdue by 30 or more days was 10%, which means late payment can affect a measurable portion of the receivables book rather than one isolated customer.

• Cash-flow problems were reported by 50% of businesses with higher overdue invoice volume, compared with 34% among businesses with lower overdue volume.

• Longer terms showed their own strain: 60% of businesses with longer payment terms reported cash-flow problems, compared with 40% of firms with immediate terms.

• Pricing pressure can follow collection pressure. Businesses more affected by late payments were more likely to have raised prices recently, at 30% versus 21% among less affected businesses.

• Credit reliance also rises with payment stress. Among businesses more affected by late payment, 21% used loans, 31% used lines of credit, and 54% used business credit cards.

• The less-affected group still used credit, but at lower rates: 11% used loans, 21% used lines of credit, and 46% used business credit cards.

Cash-flow readout

A late invoice is not only a customer-service problem. It changes the timing of payroll, vendor payments, inventory purchases, tax reserves, and owner compensation. The more useful payment metric is not simply whether the invoice was eventually paid; it is how long the business had to finance the customer before the money arrived.

Figure 4. Late payments are not only collection problems; they are linked with cash-flow strain, price pressure, and credit reliance.

ACH, Same Day ACH, and Bank-Based Payment Scale

Card payments and mobile payments often dominate customer-facing conversations, but bank-based payments matter deeply for invoice-led, recurring, B2B, and higher-value payment flows. ACH is not always the most visible payment method, yet it can be one of the most useful options when the business wants cleaner recurring collection, lower manual follow-up, and a direct route between bank records and accounting records.

ACH should not be presented as a universal replacement for cards or cash. Its fit depends on trust, transaction size, billing frequency, authorization, and how easily the customer can approve bank payment. For many service businesses, though, the value of ACH is practical: fewer mailed checks, less card-fee pressure in some cases, and a clearer path for recurring or scheduled payments.

Bank-based payment benchmarks

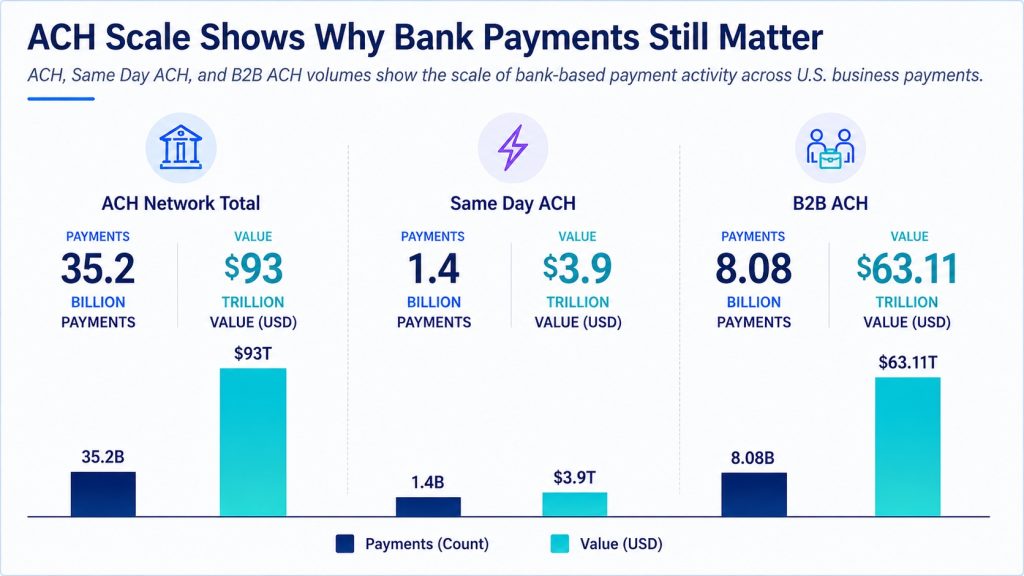

• Across the ACH Network, 35.2 billion payments were processed in 2025, carrying $93.0 trillion in value.

• ACH volume grew 4.9% in 2025, while ACH value grew 7.9%, showing growth in both transaction count and dollars moved.

• Same Day ACH reached 1.4 billion payments in 2025, with $3.9 trillion in value moving through the same-day rail.

• The growth rate for Same Day ACH was faster than the overall network, with volume up 16.7% and value up 21.4%.

• B2B ACH remains especially relevant for business payments, with 8.08 billion payments and $63.11 trillion in value in the 2025 data.

• For small businesses, the practical value of ACH is not simply that it is digital. It can reduce reliance on mailed checks, support recurring billing, and create cleaner bank-to-accounting reconciliation when implemented well.

Figure 5. ACH and Same Day ACH provide scale and faster-settlement context for bank-based small-business payment strategies.

Consumer Payment Behavior Shapes What Customers Expect

Small-business payment decisions are also shaped by how consumers already behave in daily life. Owners may focus on settlement timing, fees, and bookkeeping, while customers focus on convenience, habit, rewards, trust, and whether the payment option feels normal. A business that ignores customer habits may create friction even when its internal payment process is technically efficient.

The consumer payment data used in the workbook does not tell every small business which method to accept. It does show why a one-method strategy can feel outdated in many customer-facing settings. Cards dominate many consumer payment moments, cash still appears frequently, mobile behavior is growing, and online payment preference can differ from in-person payment preference.

Consumer payment behavior benchmarks

• Credit cards represented 35% of consumer payments by number in the Federal Reserve payment-choice findings used for the workbook, while debit cards represented 30%.

• Cash still accounted for 14% of consumer payments by number, which helps explain why removing cash can create friction in certain local or low-ticket settings.

• Remote purchases and person-to-person payments made up 23% of the measured consumer purchase and P2P activity, keeping remote payment convenience relevant even for local businesses.

• Mobile phone payments averaged 11 per month, compared with 4 in 2018, showing how quickly mobile payment habits have become normal.

• Even though cash is a smaller share of total payment volume than cards, 83% of consumers used cash at least once in the prior 30 days.

• Checks are no longer the daily default for many consumers, but 35% still used a check in the prior 30 days in the source data.

• Cash is often situational rather than preferred: 66% of cash payments were made by consumers who generally preferred another payment method.

• For online payments, the preference split in the source data favored credit cards at 56%, with debit cards at 36%.

For a small business, the takeaway is not to chase every consumer trend. The more practical step is to test payment fit by transaction type. A local repair business might need cards, cash, and payment links. A subscription service might prioritize card-on-file and ACH. A professional-services firm might keep checks available for legacy clients while nudging new clients toward ACH or card payment through clearer invoice instructions.

Fees, Surcharges, Discounts, and the Margin Question

Payment fees are often discussed as a card-processing issue, but the margin question is broader. Each method has a cost profile. Cards carry processing fees. Cash has handling and deposit work. Checks can create delay, manual matching, and return risk. ACH may reduce some costs but requires authorization and process discipline. Payment links and mobile tools may save time but still need reconciliation.

The right question is not whether a fee exists. The right question is what the business receives in exchange for that cost. A card payment that arrives quickly may be worth more than a lower-cost method that creates weeks of collection work. A check with low direct fees may still be expensive if it delays cash or requires staff time.

• The Federal Reserve data makes fee pressure visible: payment-processing fees are cited by 52% of employer firms, the highest-ranked challenge in the survey.

• Customer-facing industries show the pressure clearly. In the workbook challenge split, 69% of leisure and hospitality firms and 65% of retail firms report fees as a payment challenge.

• Healthcare and education show another version of the issue, with 79% reporting fees as a challenge in the workbook’s challenge table.

• Consumer payment data adds nuance: 6% of cash payments received a discount, while 3% of credit-card payments and 3% of debit-card payments were surcharged.

• Certain bill categories show higher surcharge exposure. Government taxes or fees had a 21% credit-card surcharge share in the consumer data, while utilities and rent each showed 15% for credit-card payments.

• Fee recovery should not be treated as a universal fix. Surcharges, cash discounts, and payment-method steering all need to be evaluated against customer trust, compliance rules, competitive norms, and conversion behavior.

Margin interpretation

Payment cost should be reviewed alongside payment speed and collection effort. A lower-fee method is not automatically better if it increases overdue invoices, customer confusion, or staff work. A higher-fee method is not automatically worse if it improves close rate, reduces follow-up, and creates cleaner records.

Fraud, Failed Payments, and Trust Still Belong in the Scorecard

Small-business payment statistics often focus on acceptance and cash flow, but risk should not be separated from the payment discussion. Fraud, theft, disputes, failed payments, incorrect invoices, and customer mistrust can all weaken the value of a completed sale. A payment process that collects money quickly but creates refund confusion or dispute exposure is not fully healthy.

Trust is especially important for businesses that invoice after service or collect remotely. Customers need to understand who is billing them, what the charge covers, when payment is due, and which payment methods are legitimate. The same clarity that improves collection can also reduce disputes and support requests.

• Fraud or theft is reported as a payment challenge by 11% of employer firms in the Federal Reserve small-business payments data.

• Broader business payment research puts security issues among the top pain points, reported by 32% of businesses in the 2024 Federal Reserve Business Payments Study.

• Slow or not-timely payments are also reported by 32% of businesses in that study, linking speed and reliability in the same operating conversation.

• High cost or fees are listed by 48% of businesses in the same study, aligning with the small-business survey’s finding that fees are the most common challenge.

• A lack of automation is cited by 28% of businesses, which matters because manual payment work can increase mistakes, missed follow-up, and reconciliation gaps.

• Costly integration appears at 30%, showing that better payment infrastructure can require effort before it creates savings.

For smaller businesses, the risk scorecard does not have to be complicated. It should track failed payments, disputed payments, refund requests, chargeback reasons, missing receipt questions, and customers who say they did not understand the charge. These signals often point back to invoice clarity, payment instructions, documentation, and follow-up timing.

Payment Metrics Small Businesses Should Track

Statistics are useful only if they help a business decide what to measure. A small business does not need an enterprise finance dashboard, but it does need enough visibility to know whether cash is arriving on time, whether fees are manageable, and whether customers are being offered the right payment path for the way the business actually earns revenue.

| Metric | What it shows | Why it matters |

|---|---|---|

| Payment-method mix | Share of sales or invoices paid by check, card, cash, ACH, mobile payment, or other methods. | Shows whether the business is serving customer habits without creating unnecessary back-office complexity. |

| Days to collect | Average days from invoice date or service completion to usable cash. | Connects payment behavior directly to cash-flow planning. |

| Overdue invoice share | Share of invoices unpaid after 30 days or another internal threshold. | Turns late payment into a measurable operating signal instead of an occasional complaint. |

| Fee burden | Processing fees and related payment costs as a share of revenue or method volume. | Helps separate visible card fees from the hidden costs of slower or more manual methods. |

| Settlement delay | Time between customer payment and usable funds in the business account. | Separates customer promptness from payment-rail timing. |

| Reconciliation workload | Time required to match payments to invoices, receipts, orders, or customer accounts. | Shows whether payment flexibility is creating avoidable administrative work. |

| Failed or disputed payments | Payments that fail, are reversed, are questioned, or require extra documentation. | Keeps trust and risk connected to the payment process. |

A scorecard like this connects payment behavior to decisions. If fees are high but payment speed is excellent, the owner may look for better pricing rather than removing card acceptance. If checks are common but collection is slow, the owner may keep checks for legacy customers while nudging new customers toward ACH or payment links. If overdue invoices are rising, the solution may be clearer terms, earlier reminders, or deposits rather than another payment method.

A 90-Day Payment Improvement Plan

A small business does not need to rebuild its entire payment system at once. A practical 90-day review can begin with data cleanup, move into targeted fixes, and end with a repeatable scorecard. The goal is to improve cash quality without creating a confusing payment experience for customers.

| Timing | What to do | Expected output |

|---|---|---|

| Days 1-30 | Map current payment behavior by method, customer type, invoice status, days to collect, and fee burden. | A baseline that shows where cash is delayed, where fees are concentrated, and where records are incomplete. |

| Days 31-60 | Fix high-confidence leaks such as unclear payment terms, late invoice sending, missing ACH instructions, confusing receipts, or weak reminder timing. | A short list of controlled changes with clear owners and measurable before/after signals. |

| Days 61-90 | Review fee impact, overdue trends, settlement timing, failed payments, disputes, and reconciliation workload. | A repeatable payment scorecard that can be reviewed monthly rather than only at tax time or during a cash crunch. |

Planning principle

The best payment teams do not chase every benchmark. They compare outside statistics against their own payment data, then fix the leaks with high volume, clear ownership, and a visible cash-flow impact.

What the Statistics Mean for Different Business Models

The same payment statistic can mean different things depending on the business model. A 65% cash acceptance rate is highly relevant for a quick-service restaurant or local repair shop, but much less important for a professional-services firm that sends monthly invoices. A 56% ACH acceptance rate may look ordinary in aggregate but can be strategically important for recurring services, retainers, B2B sales, and high-value invoices.

That is why payment methods should not be presented as a single ranking from best to worst. The payment stack should be interpreted through the flow of work. When the customer receives the product immediately, the payment method must be convenient at the same moment. When the business delivers first and invoices later, the payment method must support approval, reminders, and reconciliation.

• A counter-service business should read the 93% card-acceptance figure among firms paid in full at sale as a convenience benchmark because customers often expect quick card or tap-based payment.

• An invoice-led business should read the 95% check-acceptance figure among after-delivery firms as proof that legacy payment behavior still affects receivables, even when digital options are available.

• A recurring-service business should pay close attention to the 66% ACH acceptance level among scheduled-service firms because automated bank payment can reduce repeated manual follow-up.

• A contractor or project-based firm can use the 10% milestone-payment share as a reminder that deposits, progress billing, change approvals, and payment schedules should be visible before work begins.

• A firm paid through financing, insurance, or another third party should treat the 80% ACH acceptance level in that segment as a settlement and reconciliation signal, not just a payment-method statistic.

From Payment Acceptance to Payment Operations

Adding payment methods can improve convenience, but it can also create more operational work if the business does not have a clean process for receipts, reconciliation, refunds, deposits, and invoice status. This is the point where payment acceptance becomes payment operations. A business can look flexible to customers and still be disorganized internally if each payment method lands in a different system with different labels and timing.

The Federal Reserve challenge data supports this point. Time-consuming processes such as billing customers and making deposits are cited by 20% of employer firms, while 13% report the challenge of managing multiple payment streams. Those numbers are lower than fee and slow-payment pressure, but they often sit underneath both problems. If records are weak, fees are harder to review and overdue invoices are harder to chase.

• A business that accepts checks, cards, cash, ACH, and mobile payments should not only track the customer-facing mix; it should also track how long each method takes to reconcile.

• When 13% of firms say multiple payment streams are a challenge, the problem is often not the existence of multiple methods but the lack of one reliable place to see payment status.

• The 20% figure for time-consuming billing or deposit work is especially important for owner-operated businesses where administrative time competes directly with sales, service, and delivery.

• Settlement delay, cited by 18% of employer firms, should be tracked separately from customer payment speed because a customer can pay promptly while funds still take time to become usable.

• Fraud or theft, at 11%, may look smaller than fee or collection pressure, but even a small fraud or dispute rate can consume owner attention when the business lacks documentation.

A Practical Small-Business Payment Example

Consider a small commercial cleaning company with six employees and a mix of monthly office contracts, one-time deep cleans, and move-out cleaning jobs. The company accepts cards for new customers, checks from a few long-term office accounts, ACH for recurring clients, and cash for occasional small jobs. On paper, that looks flexible. In practice, the owner may still struggle to see which invoices are outstanding, which checks are in transit, which card payments carried higher fees, and which recurring accounts need follow-up.

The Federal Reserve acceptance data helps explain the mix. Checks, accepted by 80% of employer firms, remain normal for commercial clients. Cards, accepted by 79% when card-based options are grouped, help with new or urgent jobs. ACH, accepted by 56%, fits recurring contracts because it can make scheduled collection easier. Cash, accepted by 65%, may still appear in local one-time work.

The challenge data explains what can go wrong. Fees may reduce margin on card payments, matching the 52% of firms that cite processing fees as a challenge. A slow-paying office client creates the type of collection issue reflected in the 39% slow-payment figure. Manual invoice work can become part of the 20% time-consuming-process problem, especially when the owner is matching deposits after hours instead of scheduling work or following up with prospects.

A better payment system for this company would segment customers. Recurring office clients could receive invoices with ACH authorization and a clear due date. One-time customers could receive payment links immediately after service. Checks could remain available for legacy clients but be tracked separately with deposit dates. The owner could review overdue invoices weekly rather than waiting until cash is tight. The statistics do not replace judgment; they help the owner see where the payment system is leaking time and cash.

How to Interpret Payment Statistics Without Overreacting

A common mistake in payments content is to turn every statistic into an immediate recommendation. If digital wallets are growing, the conclusion becomes “add wallets.” If checks remain high, the conclusion becomes “keep checks.” If fees are the top challenge, the conclusion becomes “avoid card payments.” Real businesses need a more careful reading. Each statistic should be interpreted through customer behavior, transaction size, cash-flow urgency, cost, risk, and recordkeeping.

• The 80% check-acceptance figure does not mean checks are the future of small-business payment. It means many businesses still need workflows for check receipt, deposit, matching, and follow-up.

• The 34% digital/mobile acceptance figure does not mean every firm is behind. It means mobile-payment fit should be judged by customer context, transaction size, and staff readiness.

• The 52% fee-challenge figure does not automatically mean card acceptance should be reduced. It means the owner should compare fee cost against faster collection, higher conversion, and reduced follow-up.

• The 39% slow-payment figure does not only point to difficult customers. It can also reflect unclear terms, weak invoice design, delayed sending, missing reminders, or limited payment options.

• The 56% ACH acceptance figure does not make ACH the right method for every sale. It is most useful where bank payment lowers collection work or fits recurring and invoice-led relationships.

Data Quality and Payment Recordkeeping

Small-business payment improvement often begins with cleaner records rather than a new payment product. If invoices are not numbered consistently, if payment terms are unclear, if receipts are missing, or if deposits are not matched back to customer accounts, the business may not know whether its payment problem is customer behavior, staff process, fee structure, or documentation.

This is where the payment statistics connect naturally to invoice and receipt workflows. When QuickBooks reports an average unpaid invoice exposure of $17,500 among businesses owed money, the figure is not only about customers delaying payment. It also points to the value of knowing exactly which invoices are overdue, which customers pay late repeatedly, which methods clear fastest, and which reminders lead to payment.

• A reliable invoice number helps connect a check, ACH transfer, card payment, or cash receipt back to the work that generated it.

• Clear due dates make the 30-day overdue threshold easier to monitor, which matters because 47% of U.S. small businesses in QuickBooks research had some invoices overdue by 30 or more days.

• Consistent receipt records reduce customer confusion and make refunds, disputes, and tax-time review easier to handle.

• A weekly receivables review can turn the 39% slow-paying-customer benchmark into an internal metric that the owner can actually manage.

• Payment-method reporting should separate customer convenience from back-office cleanup because the easiest method at the point of sale may not be the easiest method to reconcile.

Common Mistakes the Statistics Help Expose

Payment statistics are most useful when they expose habits that feel normal but quietly weaken cash flow. Many owners do not experience payment problems as one dramatic failure. They experience them as small recurring delays: an invoice sent late, a check deposited days after arrival, a payment link forgotten, a customer confused about the amount due, or a card payment that arrives quickly but erodes margin.

One mistake is treating payment acceptance as the same thing as payment performance. A business can accept checks, cards, cash, ACH, and mobile payments while still having a weak process if invoices are unclear or deposits are difficult to match. The Federal Reserve data showing 81% of firms accepting three or more payment forms should be read alongside the 13% that report managing multiple streams as a challenge.

Another mistake is waiting too long to follow up. QuickBooks data showing unpaid invoices at 56% of U.S. small businesses and 47% with some invoices overdue by 30 or more days should push owners toward earlier reminders. A reminder sent after the due date may already be late from a cash-flow perspective.

• When a business focuses only on new payment methods, it can miss older but expensive problems such as unclear terms, slow invoice sending, or inconsistent follow-up.

• When an owner reacts only to card fees, the business may underestimate the hidden cost of checks, delayed deposits, late invoices, and manual reconciliation.

• When payment data is reviewed only at tax time, the owner loses the chance to act while collection problems are still small.

• When every customer gets the same terms, the business may give slow-paying customers more credit than their payment history justifies.

• When receipts are inconsistent, customers have more reason to ask follow-up questions, dispute details, or delay internal approval.

Leadership Questions for Payment Decisions

The final use of the data is decision-making. A strong payment review should not leave owners with disconnected numbers. It should give owners and finance teams a way to decide what to fix first. The best question is rarely “Which payment method is best?” A better question is “Which payment change would improve cash speed, customer convenience, fee control, and record quality for this specific business model?”

| Question | Why it matters |

|---|---|

| Where does payment happen in the customer journey? | Point-of-sale businesses need speed; invoice-led businesses need approval, reminders, and receivables visibility. |

| Which customers pay late most often? | Late-payment patterns can reveal whether the issue is terms, approval, payment options, or customer selection. |

| Which method creates the most cleanup work? | A method that looks convenient can still be costly if staff spend time reconciling it manually. |

| Which fees are visible and which costs are hidden? | Processing fees are easy to see; slow checks, missed reminders, and manual deposits can be just as expensive. |

| What proof does the customer need before paying? | Clear invoices, receipts, purchase details, and payment instructions can reduce approval delays and disputes. |

Small Business Payment Statistics FAQ

What payment method do small businesses accept most often?

Checks are the most widely accepted method in the Federal Reserve small-business payments data, with acceptance at 80% of employer firms. Card acceptance is close behind when credit, debit, or digital card-based options are grouped, reaching 79%.

Are small businesses still using cash?

Yes. Cash remains accepted by 65% of employer firms in the Federal Reserve data. It is less dominant than it once was in many settings, but it still matters for face-to-face, local, small-ticket, urgent, and service transactions.

How common is ACH for small businesses?

ACH is accepted by 56% of employer firms in the survey. It is especially relevant for invoice-led, recurring, scheduled, and B2B payment relationships where bank-to-bank payment may be easier to reconcile than checks or cards.

What is the biggest payment challenge for small businesses?

Fees are the most frequently reported challenge, cited by 52% of employer firms. Slow-paying customers follow at 39%, which is why fee control and collection speed should be treated as separate but connected problems.

How serious are unpaid invoices for small businesses?

QuickBooks research found that 56% of U.S. small businesses were owed money from unpaid invoices, with an average unpaid amount of $17,500 among businesses that had money outstanding. That makes unpaid invoices a working-capital issue, not merely an accounting inconvenience.

Should small businesses add more payment methods?

They should add the methods that fit their revenue model. A point-of-sale business may need fast card and mobile payment options, while an invoice-led business may benefit more from ACH, clear payment terms, reminders, deposits, and better reconciliation.

What payment metric should owners watch first?

For many small businesses, the first useful metric is days to collect. It connects invoice timing, customer behavior, payment method, reminder discipline, and settlement speed into one measure that affects cash flow directly.

Final Takeaway

Small-business payment statistics point to one practical conclusion: getting paid is a system. Payment acceptance, invoice timing, customer convenience, processing fees, settlement speed, credit reliance, and follow-up workload all affect whether a sale becomes healthy cash. A business can offer many payment options and still struggle if the process around those options is unclear.

The most effective payment strategy always begins with understanding the business model and operational needs. Retail and hospitality businesses usually prioritize fast transactions, customer convenience, and reliable cash or card payment processing. Manufacturing companies and professional service providers often require detailed invoices, ACH payment options, automated reminders, and stronger receivable management practices. Businesses that manage property or equipment rentals may also depend on a well-structured rental invoice system to track recurring charges, deposits, payment schedules, and customer agreements more accurately. Meanwhile, project-based companies need milestone billing, approval tracking, and clear change-order documentation, while subscription-based businesses benefit from automation and consistent recurring billing records that improve financial predictability.

For Zintego’s audience, the payment lesson is closely tied to billing quality. A clean invoice, clear payment terms, easy payment instructions, accurate receipts, and consistent follow-up can reduce confusion before it becomes a cash-flow problem. The numbers show where payment pressure appears, but the practical solution is usually operational: send the invoice promptly, make the amount and due date easy to understand, offer the right payment options, record the payment cleanly, and follow up before a delay becomes normal.