Embedded payments are no longer just a payment button inside software. They are the transaction layer that lets a platform accept money, move funds, trigger payouts, store payment credentials, reconcile records, and sometimes offer financing without sending the user to a separate banking workflow. That is why the topic belongs at the center of platform strategy, not only payments operations.

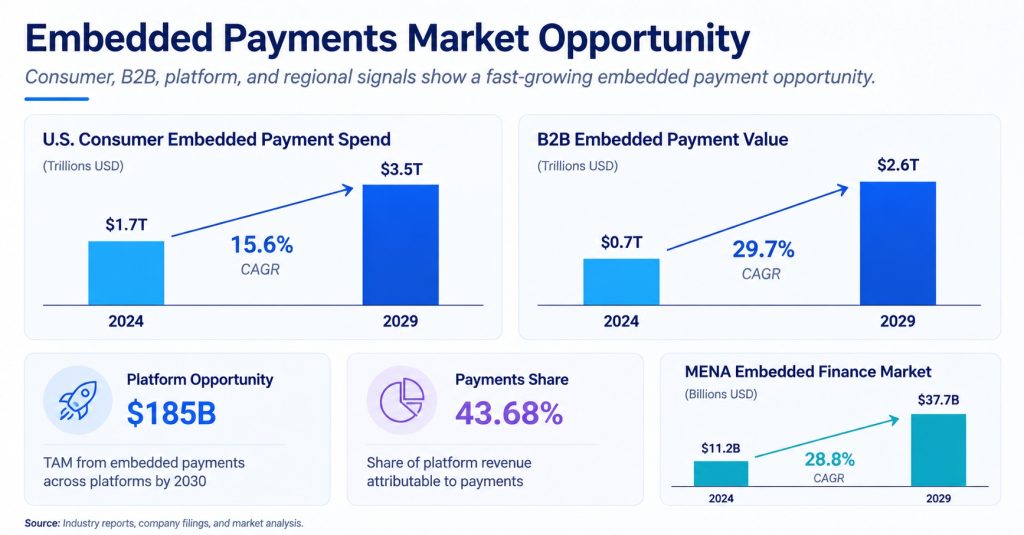

The most useful statistics show a market that is large, uneven, and highly regional. Bain estimates U.S. consumer embedded payment volume at $1.7 trillion and projects it could reach $3.5 trillion. In B2B, Bain’s projection moves from $0.7 trillion to $2.6 trillion, while Adyen and BCG estimate a $185 billion embedded payments and finance opportunity across platforms. Those numbers matter because embedded payments are where software companies, marketplaces, banks, processors, and vertical SaaS providers all meet the same customer workflow.

The most useful way to read embedded payment statistics is through practical operating decisions: where payment capability creates platform revenue, how rails shape product design, which regions require local payment logic, and what implementation work determines whether adoption turns into durable value.

Executive Embedded Payments Benchmarks

The executive picture is clear: embedded payments sit at the intersection of software distribution, payment acceptance, regional payment rails, and business workflow automation. The strongest benchmarks do not all measure the same thing. Some show transaction value, some show revenue, some show platform economics, and some show how local payment behavior changes what must be embedded.

The numbers that define the embedded payments market

• Bain’s consumer estimate places U.S. embedded payment spend at $1.7 trillion, with projected volume of $3.5 trillion as platforms capture more payment activity inside daily customer workflows.

• In Bain’s B2B view, embedded payment value starts from a much smaller penetration base: only about $0.7 trillion is embedded today even though U.S. B2B payment transaction value is measured near $27.5 trillion.

• Adyen and BCG put the platform opportunity at $185 billion, and they describe roughly 80% of that opportunity as still untapped.

• Payments carry the largest service share in one regional market-sizing view, accounting for 43.68% of embedded finance activity, ahead of several adjacent services.

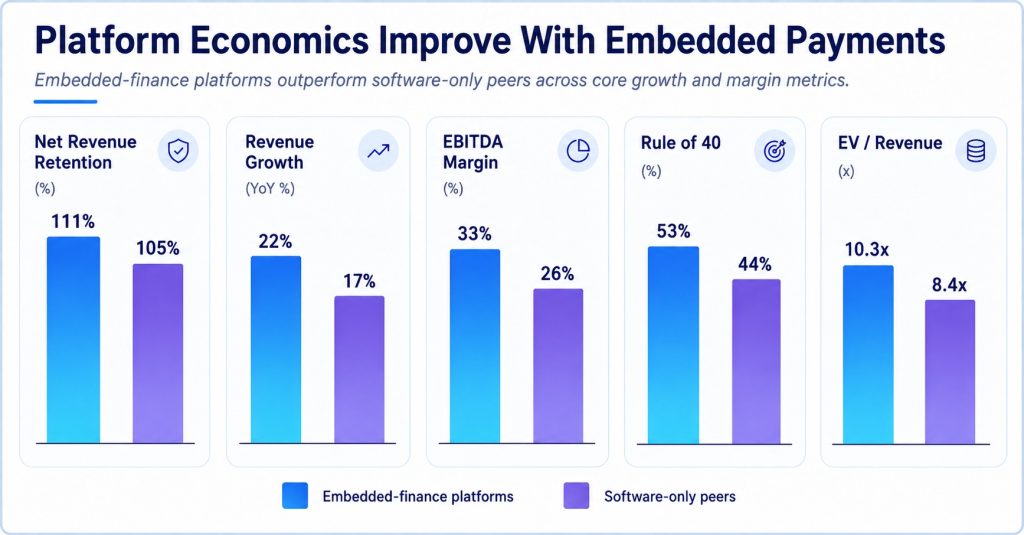

• William Blair and Stripe data suggests that embedded finance platforms can show stronger operating metrics, including 111% net revenue retention versus 105% for software-only peers.

• The same valuation work shows an EV/revenue multiple of 10.3x for embedded-finance platforms compared with 8.4x for software-only platforms.

• Worldpay’s global payment context shows why embedded checkout and wallet flows matter: digital wallets represented 53% of ecommerce spend in 2024 and 32% of point-of-sale spend.

• Regional payment rails are not background detail. India’s UPI reached about 22,000 crore transactions in calendar 2025, while Brazil’s Pix reached 68.7 billion transactions in 2024.

• The UK illustrates how mature card and account-to-account markets can coexist. UK Finance counted 48.8 billion total payments in 2024, with debit cards making up 53% of all payments and Faster Payments/remote banking reaching 5.6 billion payments.

• Nacha’s ACH data gives a U.S. bank-payment anchor for embedded B2B and payout use cases, with the ACH Network processing 35.2 billion payments worth $93 trillion in 2025.

• Worldpay estimates global digital payment value grew from $1.7 trillion in 2014 to $18.7 trillion in 2024, giving embedded-payment products a much larger transaction base to organize.

• MENA is becoming a regional signal rather than a footnote: the World Economic Forum cites an embedded-finance market of $11.2 billion in 2024 and a projected $37.7 billion by 2029.

Editorial readout Embedded payments are not one market moving at one speed. Consumer payments, B2B payments, platform monetization, local wallets, real-time bank rails, and payout infrastructure all move differently. A platform that treats embedded payments as a generic checkout feature will miss the harder questions: which users already trust the platform, which rails fit the region, how reconciliation works, and whether the payment product improves the workflow enough to justify the operational burden.

Figure 1. Embedded payments should be judged through platform opportunity, B2B and consumer transaction value, SMB demand, and regional rail maturity rather than through a single market-size estimate.

What Embedded Payments Actually Mean

Embedded payments are easiest to understand through the user’s job. A restaurant owner wants deposits and card-on-file payments inside the booking system. A contractor wants milestone payments attached to estimates, invoices, and change orders. A marketplace wants split settlement and seller payouts after the buyer pays. A SaaS platform wants invoices, fees, disputes, payouts, refunds, and reporting to live in the same place as the work that created the payment.

That workflow view is important because embedded payments can include different products. Some platforms embed card acceptance. Others add ACH, instant payments, wallets, local A2A rails, BNPL, virtual cards, vendor payouts, or wallet balances. The payment product may be visible to the end user, or it may sit behind an operating process such as invoice collection, payout scheduling, or automated reconciliation.

Where the payment becomes embedded

• A vertical SaaS platform embeds payments when the user can accept a card, ACH transfer, or wallet payment without leaving the workflow that generated the invoice, booking, subscription, order, or service visit.

• A marketplace embeds payments when buyer collection, platform fees, seller payouts, refunds, disputes, tax handling, and settlement timing are managed inside the marketplace experience.

• A B2B platform embeds payments when suppliers, buyers, invoices, remittance details, approval rules, and reconciliation data travel with the money rather than being handled in separate files and email threads.

• A consumer app embeds payments when checkout, stored credentials, wallet selection, loyalty, tips, delivery, and refunds become part of the same branded experience instead of a separate processor screen.

• A regional rail becomes embedded when local payment behavior is exposed through a platform interface. UPI in India, Pix in Brazil, Faster Payments in the UK, ACH in the U.S., and card-wallet funding in North America all create different product requirements.

Why definition matters The definition affects the numbers. A market-size forecast may count payments, lending, insurance, accounts, cards, or investment products. A platform operator needs a narrower question: which payment job can be embedded in the existing customer workflow, and does that payment job create enough value to support compliance, support, risk, onboarding, and reconciliation?

The Platform Revenue Case

The first business case for embedded payments is revenue. Payments can turn software usage into transaction economics, but only when the platform already has user trust and enough payment volume to make the product meaningful. That is why embedded payments often appear first in software categories where the platform already manages orders, bookings, invoices, payroll, invoices, subscriptions, delivery, or vendor relationships.

Adyen and BCG’s platform estimate is useful because it links embedded payments to the SaaS business model rather than treating payments as a standalone acquiring product. A $185 billion opportunity is large, but the more useful detail is the adoption gap. If only about 20% of the market is currently addressed, the next phase depends less on whether the opportunity exists and more on which platforms have the right distribution, compliance model, user trust, and operational capacity.

Platform economics worth watching

• Platform demand is already visible. In Adyen and BCG’s research, around 50% of small and midsize businesses said they would likely use a full suite of embedded finance products from a platform they already rely on.

• The same platform opportunity has grown materially, with Adyen and BCG describing a 25% TAM increase since the earlier 2022 estimate.

• Embedded finance can become a major platform revenue line. Adyen’s SaaS platform material describes top platforms generating 50%+ of revenue from embedded payments and finance.

• Restaurant software provides a simple example of vertical fit: Adyen cites 70% restaurant demand for payment services from their platform, which makes sense because reservations, checks, tips, deposits, and refunds already sit inside restaurant operations.

• William Blair and Stripe benchmarks show embedded-finance platforms with 22% revenue growth and 33% EBITDA margin, compared with 17% growth and 26% EBITDA margin for software-only peers in one comparison.

• The Rule of 40 comparison points in the same direction: embedded-finance platforms reached 53%, while software-only peers reached 44%.

• Valuation data suggests investors reward strong payment attachment. Embedded-finance platforms had a 10.3x EV/revenue multiple compared with 8.4x for software-only platforms, a premium of about 23%.

• Retention may be the quieter advantage. Embedded-finance platforms showed 111% net revenue retention versus 105% for software-only platforms, while customer-level gross retention reached 95% for embedded-finance customers.

These statistics do not mean every software company should become a payments company. They mean payment products can improve retention, revenue density, and valuation when they solve a workflow problem the platform already owns. A scheduling product that adds payments without deposits, refund logic, chargeback support, and reporting may create more friction. A scheduling product that handles deposits, cancellations, tips, recurring customers, and end-of-day reconciliation can make payments feel like part of the product rather than an add-on.

Platform interpretation The strongest embedded-payment opportunities usually start where three conditions overlap: the platform sees the transaction before anyone else, the customer already trusts the platform to manage the workflow, and the payment data improves the next step. Without all three, the platform may capture some fees but struggle with adoption, support, and risk.

Figure 2. Platform economics improve when embedded payments connect to retention, revenue growth, margin, and valuation rather than only payment-processing volume.

Consumer Embedded Payments: Small Actions at Large Scale

Consumer embedded payments are often small moments repeated at enormous volume: booking a ride, ordering food, paying for a home-service appointment, tipping a worker, renewing a subscription, or checking out inside a social or marketplace experience. The payment disappears into the action. That is why the embedded part matters. The user does not think, “I am using payment infrastructure.” The user thinks the app handled the task.

Bain’s consumer numbers explain why those small interactions create large markets. Consumer payments make up more than 60% of embedded finance transactions in Bain’s framework, and U.S. consumer embedded payment spend is already estimated around $1.7 trillion. The projection to $3.5 trillion is not just a growth forecast; it reflects the continued movement of commerce into platforms that control checkout, identity, order history, and fulfillment communication.

Consumer payment signals that matter

• Bain estimates embedded consumer payment revenue at $12 billion today, with projected revenue of $21 billion as transaction volume expands.

• The aggregate take rate in Bain’s consumer embedded payment estimate is about 75 basis points, which is useful for understanding why volume and product attachment both matter.

• Retail and food-service platforms are expected to capture about 70% of projected SMB transaction volume in Bain’s consumer model, showing why merchant-facing software matters even when the end payment is consumer-to-business.

• Platform revenue from embedded consumer payments is projected at $14 billion, while enabler revenue is projected at $7 billion in the same Bain framework.

• Worldpay’s digital-wallet data shows the consumer payment environment moving toward embedded credentials: wallets represented 53% of ecommerce spend and 32% of POS spend in 2024.

• Mobile behavior makes embedded payments harder to separate from product experience. Worldpay reports smartphones grew from 19% of global ecommerce spend in 2014 to 57% in 2024.

• The card layer still matters even when wallets are visible. In the U.S., Worldpay reports 65% of Americans fund digital wallets with credit or debit cards.

• BNPL is another embedded consumer path. Worldpay data shows online BNPL spend growing from about $2.2 billion in 2014 to $342 billion in 2024.

A consumer platform should not look at those numbers and simply add every payment method. The better question is where payment friction interrupts the task. A deposit inside a booking flow solves no-show risk. A wallet inside a mobile checkout solves typing friction. A stored credential inside a subscription product solves renewal friction. A payout inside a gig platform solves worker liquidity. The embedded payment is valuable when it removes a specific operational step.

| Consumer use case | Payment job | Useful embedded-payment metric |

|---|---|---|

| Booking or appointment software | Deposits, cancellation fees, tips, stored cards | Deposit conversion, no-show rate, refund turnaround |

| Food, retail, and local commerce platforms | Wallets, cards, order-ahead payments, loyalty-linked checkout | Mobile completion, payment-method mix, refund volume |

| Subscription software | Card-on-file, account updater, renewal retries | Retry success, involuntary churn, failed-payment recovery |

| Marketplace or gig platform | Buyer collection, platform fee, seller/worker payout | Payout speed, dispute rate, seller retention |

| Creator or community platforms | One-click payments, tips, memberships, microtransactions | Repeat payment rate, wallet share, chargeback rate |

Embedded B2B Payments: The Bigger Workflow Problem

B2B embedded payments are usually less visible than consumer checkout but more operationally complicated. A B2B payment often has an invoice, a purchase order, approval rules, remittance data, vendor records, bank-account validation, payment timing, and cash-application work attached to it. That means the embedded payment product must move information as well as money.

Bain’s B2B numbers show both the size of the opportunity and the reason adoption is not automatic. U.S. B2B payment transaction value is estimated at $27.5 trillion, but embedded B2B payment value is only about $0.7 trillion today. The projected move to $2.6 trillion suggests strong growth, but it also shows that much of the B2B payment market still runs through older workflows, bank portals, ERP exports, checks, wires, ACH files, and approval processes.

B2B stats that belong in the operating discussion

• Bain estimates AP/AR services represent about 90% of B2B payment value, which means embedded B2B payments are really about invoice and receivables workflow, not only the payment rail.

• Embedded B2B payment revenue is estimated at $1.9 billion today, including about $0.7 billion from card payment revenue and $1.2 billion from ACH revenue.

• The projected B2B embedded payment revenue figure rises to $6.7 billion, with projected card platform revenue of $1.5 billion and enabler revenue of $0.8 billion.

• The B2B transaction-value base is projected to increase from $27.5 trillion to $33.3 trillion, but the larger story is penetration: embedded volume is projected to grow from $0.7 trillion to $2.6 trillion.

• Juniper’s B2B payment research adds a global transaction-value lens, forecasting a market of $174.2 trillion in 2025 and $213.5 trillion by 2030.

• The Federal Reserve’s business-payment study shows why embedded payment products must support multiple rails: business usage included wire transfers at 68%, Same Day ACH at 67%, cash at 62%, checks at 63%, and credit cards at 60% in 2024.

• Same Day ACH usage in that study rose by 13 percentage points from 2023 to 2024, while wire transfers rose by 14 percentage points, showing that speed and certainty are both part of business payment modernization.

• The ACH Network processed 8.08 billion B2B ACH payments worth $63.11 trillion in 2025, giving embedded B2B platforms a large bank-payment foundation if they can handle remittance and reconciliation cleanly.

For a B2B platform, the payment rail is rarely the whole product. A supplier portal that collects ACH payments but fails to carry invoice numbers creates work for AR. A buyer workflow that sends virtual cards but does not match remittance details creates supplier support tickets. A construction platform that collects deposits but cannot track change orders creates disputes. Embedded B2B payments work only when the data model follows the transaction.

B2B interpretation The B2B embedded-payment opportunity is large because the payment is connected to the job record. Invoices, purchase orders, supplier approvals, tax documents, delivery confirmation, bank details, and remittance messages all shape whether the payment creates efficiency or only changes the rail. The best embedded products treat money movement and operational data as one workflow.

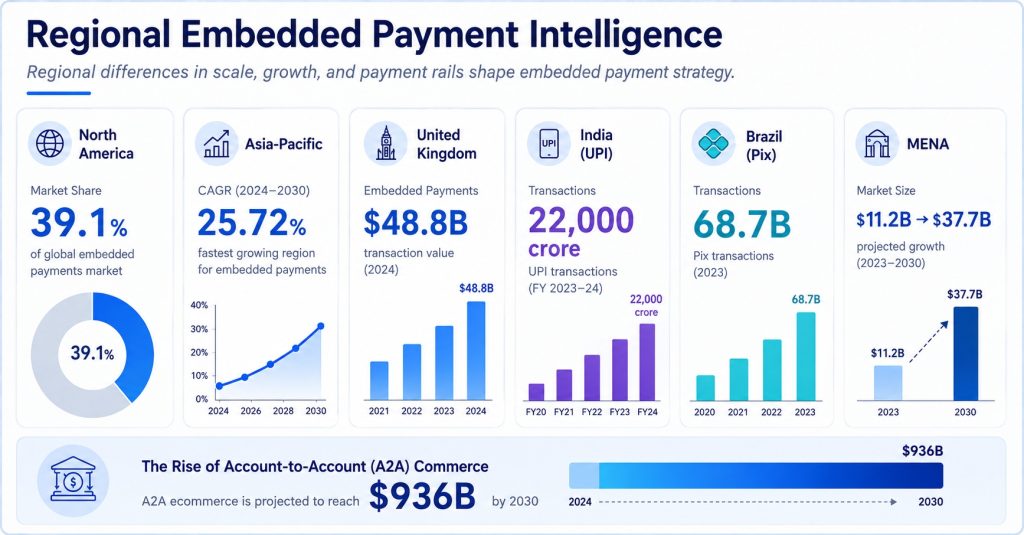

Regional Embedded Payment Intelligence

Regional context matters more for embedded payments than for many other software categories. A platform can reuse product logic across markets, but it cannot assume the same payment habits, rails, settlement expectations, bank relationships, or consumer trust patterns. The regional numbers show why localization is not only about currency and language.

North America remains a large embedded-finance base, but Asia-Pacific is one of the fastest-moving regions because mobile, real-time payments, and super-app behavior already train users to pay inside digital journeys. Europe and the UK add a different mix: cards, contactless, Direct Debit, Faster Payments, open-banking rules, and BNPL expectations. Brazil and India show how local account-to-account rails can become platform infrastructure at national scale.

Regional and country stats to use carefully

• Mordor’s regional view names North America as the largest embedded-finance region, with about 39.1% of the market in 2025.

• The same forecast shows Asia-Pacific as the faster-growth region, with embedded-finance CAGR of 25.72% to 2031 compared with a global CAGR of 23.84%.

• Retail and ecommerce account for 36.05% of embedded-finance end use in the Mordor estimate, while consumer propositions account for 61.52%.

• Worldpay’s global digital-payment value rose from $1.7 trillion in 2014 to $18.7 trillion in 2024, creating the transaction backdrop for embedded payment products.

• UK Finance counted 48.8 billion total UK payments in 2024, and debit cards alone represented 26.1 billion payments.

• In the UK, card payments accounted for 64% of all payments in 2024, while cash accounted for 9% and is projected to fall to 4% by 2034.

• Faster Payments and other remote banking payments reached 5.6 billion UK payments in 2024, and the projection rises to 8.5 billion by 2034.

• UK BNPL use also changed quickly: the share of UK adults using BNPL rose from 14% in 2023 to 25% in 2024.

• India’s UPI processed about 22,000 crore transactions in calendar 2025, with a daily average near 60 crore transactions.

• UPI crossed the 2,000 crore monthly transaction mark in August 2025 and reached 2,163 crore monthly transactions by December.

• Brazil’s Pix processed 68.7 billion transactions in 2024, with transaction growth of 52% year over year and person-to-business Pix growth of 90%.

• Worldpay’s Brazil data shows Pix-linked A2A ecommerce value rising from $3.6 billion in 2020 to $35.3 billion in 2024.

• Canada provides a mature card-market comparison, with 22.5 billion retail payment transactions worth C$12.2 trillion in 2024.

• MENA embedded finance is forecast to expand from $11.2 billion in 2024 to $37.7 billion by 2029, a projected increase of $26.5 billion.

• Worldpay’s global A2A ecommerce projection reaches $936 billion by 2030, which makes local bank-payment integration a strategic embedded-payment topic rather than a niche regional feature.

| Consumer use case | Payment job | Useful embedded-payment metric |

|---|---|---|

| Booking or appointment software | Deposits, cancellation fees, tips, stored cards | Deposit conversion, no-show rate, refund turnaround |

| Food, retail, and local commerce platforms | Wallets, cards, order-ahead payments, loyalty-linked checkout | Mobile completion, payment-method mix, refund volume |

| Subscription software | Card-on-file, account updater, renewal retries | Retry success, involuntary churn, failed-payment recovery |

| Marketplace or gig platform | Buyer collection, platform fee, seller/worker payout | Payout speed, dispute rate, seller retention |

| Creator or community platforms | One-click payments, tips, memberships, microtransactions | Repeat payment rate, wallet share, chargeback rate |

Figure 3. Regional embedded-payment planning should compare global market growth with local rails such as cards, wallets, Faster Payments, UPI, Pix, ACH, and A2A ecommerce.

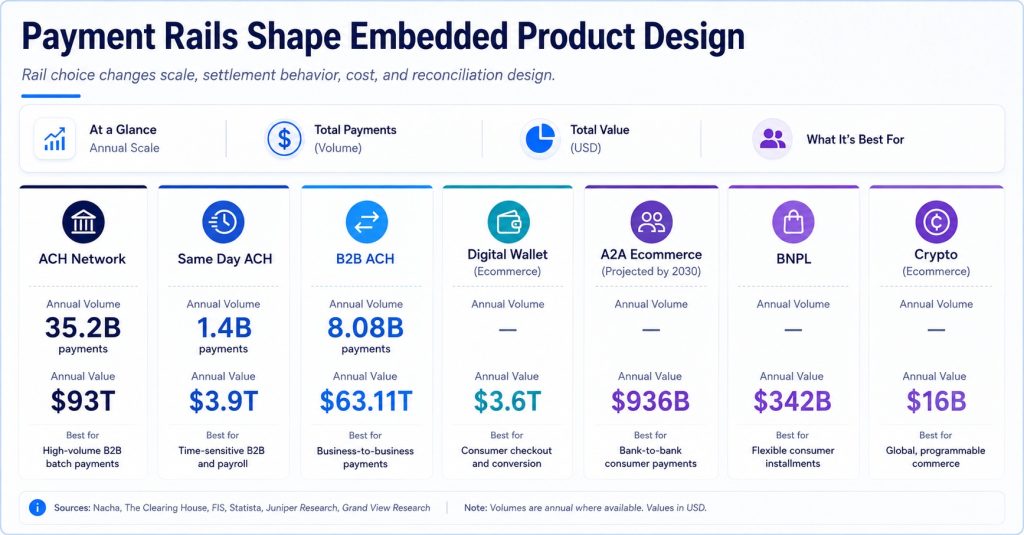

Why Payment Rails Shape Embedded Product Design

A platform can design one user experience, but the rail underneath changes cost, timing, risk, and reconciliation. Cards bring acceptance and chargeback rules. ACH brings bank-account logic and settlement windows. Instant payments bring speed and finality. Wallets bring stored credentials and mobile convenience. BNPL changes the financing decision. A2A rails can reduce card dependency but require customer familiarity and local infrastructure.

The rail decision is especially important because embedded payment products usually promise simplicity. The user sees one button, invoice, or payout screen. Behind that screen, the platform may need KYC/KYB, tokenization, dispute support, settlement reporting, bank-account validation, retries, refunds, tax treatment, and provider reconciliation. Rail choice changes all of those operating details.

Rail-level benchmarks for embedded product teams

• Nacha’s 2025 ACH Network total of 35.2 billion payments and $93 trillion in value shows why bank rails remain central to embedded B2B payments and payouts.

• Same Day ACH reached 1.4 billion payments worth $3.9 trillion in 2025, with volume growth of 16.7% and value growth of 21.4%.

• The ACH Network’s daily scale was already large, with average daily transactions of about 141 million across the network in 2025.

• Business-payment research from the Federal Reserve shows wire transfers at 68% usage, Same Day ACH at 67%, and checks at 63% among businesses in 2024, which means embedded B2B products must handle both old and newer rails.

• Digital wallets remain a consumer embedded-payment anchor, with global ecommerce wallet spend around $3.6 trillion and in-store wallet spend near $12 trillion in Worldpay’s 2024 data.

• A2A payments are gaining ecommerce relevance: Worldpay projects A2A ecommerce spend of $936 billion by 2030, up from $152 billion in 2014.

• BNPL remains part of the embedded-payment toolkit, with online BNPL spend at $342 billion in 2024 after starting around $2.2 billion in 2014.

• Crypto is still comparatively small in this payment-method context, with global spend at $16 billion in 2024 and a projected $38 billion by 2030.

Rail interpretation A platform should not choose rails only by headline growth. The right rail depends on ticket size, chargeback exposure, settlement speed, customer habit, refund logic, recurring use, country, compliance burden, and reconciliation needs. In embedded payments, a cheaper rail that creates support work may be more expensive than a higher-fee rail that fits the workflow cleanly.

Figure 4. Payment rails affect embedded-product design through speed, cost, user habit, settlement, dispute handling, and reconciliation effort.

Vertical SaaS: Where Embedded Payments Become Practical

Embedded payments become easiest to sell when the platform already owns a vertical workflow. A generic payment page competes with banks and processors. A vertical SaaS platform can instead solve a specific job: collecting deposits, charging recurring clients, paying vendors, releasing marketplace payouts, funding supplier invoices, or matching remittance detail to a customer record.

The sector data supports that logic. Mordor’s forecast points to vertical SaaS adoption as one of the drivers of embedded-finance growth. Adyen’s platform data also shows why SMBs are open to finance inside software they already use. The trust is not abstract; it is built from daily workflow dependence. A small business is more willing to use embedded payments when the payment reduces steps inside the system already used to run appointments, jobs, subscriptions, invoices, orders, or payroll.

| Vertical | Embedded-payment opportunity | Stats that shape the decision |

|---|---|---|

| Restaurants and hospitality | Deposits, online orders, table payments, tips, refunds, and reconciliation | Restaurant payment-service demand from platforms reaches 70% in Adyen material; wallets and mobile commerce create strong UX expectations. |

| Field services and contractors | Deposits, milestones, change-order payments, invoice links, card-on-file, ACH | B2B embedded payment value can grow from $0.7T to $2.6T, while ACH and card rails serve different ticket sizes. |

| Healthcare and wellness | Patient payments, payment plans, card-on-file, refunds, claims-adjacent reconciliation | Consumer proposition share of embedded finance reaches 61.52%, but compliance and data security raise implementation stakes. |

| Marketplaces | Buyer collection, seller onboarding, split settlement, payouts, disputes | Platform revenue from embedded consumer payments is projected at $14B, and payout speed affects seller retention. |

| B2B software and AR/AP platforms | Invoice collection, supplier payments, virtual cards, ACH, remittance matching | AP/AR services represent about 90% of B2B payment value, so information quality is as important as funds movement. |

Vertical examples where stats become product decisions

The practical lesson is that vertical fit is more important than feature count. A salon platform that adds basic card acceptance may get some processing revenue. A salon platform that handles deposits, no-show fees, staff tips, memberships, refunds, and daily reconciliation can change how the business runs. That second version is closer to true embedded payments because the money movement is tied to the work record.

The same logic applies to lower-volume categories. A professional-services platform may not process marketplace-sized payment volume, but it can still create value if invoice links, client deposits, retainers, refunds, and aging reports reduce collection effort. Embedded payments should be evaluated through workflow importance as well as raw volume because a smaller payment stream can still make the software much harder to replace.

Implementation Friction: Why Adoption Does Not Follow Market Size Automatically

Large market forecasts can make embedded payments sound inevitable, but adoption usually depends on unglamorous implementation details. The platform must onboard customers, underwrite risk, verify accounts, handle disputes, explain fees, protect sensitive data, support failed payments, reconcile deposits, and stay compliant across markets. If the experience is not simple, users will keep their existing processor or bank workflow even when the embedded option is theoretically better.

Payment experience research also shows why implementation cannot be treated as purely technical. Business users often care about cost, security, speed, integration, automation, and visibility at the same time. A platform can improve one dimension and still fail if the payment does not post correctly, the report is incomplete, or the counterparty does not understand what to do.

Operational statistics that should shape the roadmap

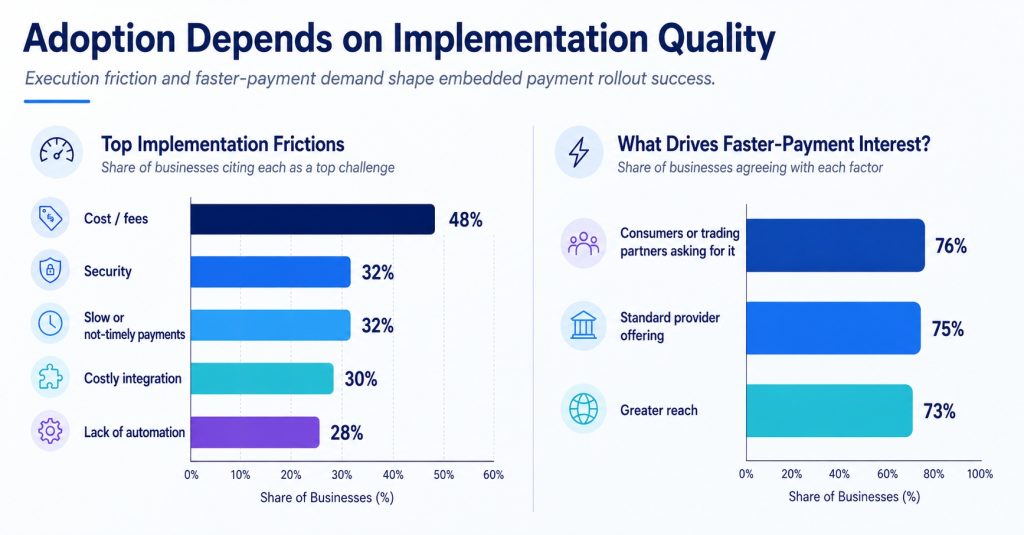

• The Federal Reserve’s business-payment study shows high cost and fees as a top payment pain point for 48% of businesses, which means embedded pricing must be easy to understand before adoption can scale.

• Security issues appear as a top pain point for 32% of businesses, a warning that embedded payment flows must handle account changes, credential storage, fraud review, and user permissions carefully.

• Slow or not-timely payments also register at 32%, which supports embedded products that combine payment initiation, status visibility, and faster settlement options.

• Costly integration appears at 30%, which matters directly to platforms because a payment product that creates ERP, accounting, or reconciliation work may fail even if the payment method itself is modern.

• Lack of automation is cited by 28%, a reminder that the promise of embedded payments is not just collecting money in-app but reducing the manual work around payment exceptions.

• Instant payment interest depends on network effects. In the Federal Reserve study, 76% of businesses said consumers asking for it would increase interest, and 76% said trading partners asking for it would do the same.

• Adoption also depends on defaults: 75% said having the service offered as standard by a provider would increase interest in instant payments.

• Greater reach matters as well, with 73% saying more businesses using the service would increase interest, which shows why embedded payment adoption often accelerates after a rail becomes familiar.

Implementation interpretation The adoption barrier is often not willingness to pay electronically. It is confidence that the embedded product will work with the user’s existing records, counterparties, approval rules, staff roles, bank accounts, refunds, disputes, and reporting. A platform roadmap should therefore treat onboarding, education, reconciliation, and exception handling as core product work.

Figure 5. Embedded payment adoption depends on market demand, implementation quality, counterparty readiness, integration cost, and the ability to automate exception work.

Use-Case Deep Dives: Where the Statistics Become Product Requirements

The embedded-payment opportunity becomes easier to evaluate when the market statistics are translated into concrete platform situations. The same $185 billion platform opportunity can look very different inside a restaurant system, a contractor platform, a marketplace, or a B2B invoice network. Each use case has its own payment timing, risk pattern, rail preference, and data requirement. That is why the strongest embedded-payment products are usually narrow at the beginning: they solve one payment job very well before expanding into a broader finance stack.

Marketplace and seller payout platforms

Marketplaces usually feel embedded from the beginning because the buyer and seller both expect the platform to coordinate trust. The buyer wants a simple checkout. The seller wants a predictable payout. The platform needs to collect its fee, manage refunds, identify risky transactions, and keep settlement records clear enough for support and tax reporting. In that setting, payments are not a side product. They are part of the marketplace promise.

• Marketplace payment products should start with payout reliability because seller experience depends on both the size of the transaction and the timing of the funds.

• Worldpay’s wallet figures show why buyer-side checkout still matters: ecommerce wallet spend reached about $3.6 trillion in 2024, so a marketplace that ignores wallet behavior may create avoidable buyer friction.

• Payout rail selection should vary by country. ACH and Same Day ACH may fit U.S. seller payouts, Faster Payments may fit the UK, Pix may fit Brazil, and UPI-style expectations can influence how Indian users think about speed and confirmation.

• Bain’s projection of platform revenue from embedded consumer payments at $14 billion helps explain why marketplaces invest in payments even when take rates appear small on a single transaction.

• A marketplace should measure dispute rate and payout exception rate alongside payment volume because a high-volume embedded payment system can still hurt seller trust if refunds, holds, or failed payouts are unclear.

Vertical SaaS platforms serving small businesses

Vertical SaaS products often have the best embedded-payment wedge because they already know the workflow. A booking system knows when a customer schedules. A field-service system knows when a job is completed. An invoice product knows the amount due and the customer record. A membership system knows the renewal cycle. Those records make the embedded payment smarter than a generic payment page.

• Adyen and BCG’s finding that about 50% of SMBs would likely use a full suite of embedded finance products from their platform supports the vertical SaaS case, but only when the platform is already trusted for daily operations.

• Adyen’s platform material gives a useful trust signal: when SMB interest reaches 40%, many small businesses are showing a preference for financial tools inside software they already use.

• A restaurant platform has a natural payment use case when 70% restaurant demand for payment services appears in platform research, but the product still has to handle tips, deposits, refunds, no-shows, and end-of-day reporting.

• Mordor’s estimate that SaaS payment monetization can range from 10% to 25% of additional income gives platforms a revenue reason to explore payments, but the product still has to reduce work for the merchant.

• The retail and ecommerce share of 36.05% in one embedded-finance end-use estimate points toward categories where checkout, order management, returns, delivery, loyalty, and refund workflows already sit close to payments.

B2B invoice, procurement, and AR/AP platforms

B2B embedded payments require more patience because adoption depends on both sides of the transaction. The buyer may want controls, approvals, and preferred payment timing. The supplier may want faster collection, usable remittance data, fewer portals, and predictable posting. The platform has to connect those needs without creating a new exception queue.

• Bain’s estimate that AP/AR services account for about 90% of B2B payment value is a reminder that B2B embedded payments are mainly workflow products, not only money-movement products.

• The projected rise from $0.7 trillion to $2.6 trillion in embedded B2B payment value suggests a large growth path, but it also shows that most B2B payments are still outside embedded workflows.

• ACH payment scale matters for invoice platforms because Nacha counted 8.08 billion B2B ACH payments in 2025, worth $63.11 trillion.

• Check and wire persistence still affects product design. Federal Reserve business-payment data shows checks at 63% usage and wires at 68% usage in 2024, so embedded platforms often need migration paths rather than sudden replacement strategies.

• Costly integration is not a minor detail when 30% of businesses name it as a pain point, so B2B platforms should prove accounting, ERP, and bank data connections early.

Regional wallet and account-to-account platforms

The regional layer is where embedded payments stop being a generic global playbook. A payment flow that feels modern in one country may feel incomplete in another. In a card-heavy market, wallet funding and card authorization can be central. In a real-time A2A market, instant confirmation and bank-app behavior may define trust. In a region where cash is declining but still meaningful, embedded payments may need both digital convenience and fallback options.

• India’s UPI scale, with roughly 22,000 crore transactions in 2025, shows how an account-to-account rail can become the default expectation for fast digital payment experiences.

• Brazil’s Pix data points in the same direction from a different market: 68.7 billion transactions in 2024 and 90% person-to-business growth create strong reasons for platforms to embed Pix-like flows locally.

• In the UK, Faster Payments and remote banking reaching 5.6 billion payments in 2024 gives account-to-account flows a practical base, while card payments still account for 64% of all payments.

• Worldpay’s projected A2A ecommerce spend of $936 billion by 2030 suggests more platforms will need bank-payment journeys that feel as natural as card and wallet checkout.

• MENA’s projected rise from $11.2 billion in embedded finance in 2024 to $37.7 billion by 2029 shows why regional partnership, compliance, and local bank connectivity should be planned early rather than added after launch.

Use-case readout These examples show why more statistics do not automatically make a better embedded-payment strategy. The numbers become useful when they answer a specific product question: which payment job should be embedded, which user already trusts the platform, which rail fits the region, and which operational data must travel with the money?

How to Evaluate an Embedded Payments Opportunity

A strong embedded-payments strategy starts with the workflow, not the processor. The product team should first identify where money currently leaves the software experience. Then it should measure whether bringing that payment inside the product will reduce friction, improve cash flow, raise retention, or open a durable revenue stream. Market-size statistics help with prioritization, but the product case still needs a user-level problem.

A platform should also be honest about tradeoffs. Payments can improve monetization, but they add risk and responsibility. They can raise retention, but only when the payment experience is reliable. They can reduce churn, but only if users see the platform as the natural place to manage the transaction. They can improve valuation, but only when payment revenue is attached to durable customer behavior rather than a temporary fee stream.

| Question | What to measure | Why it matters |

|---|---|---|

| Does the platform already control the workflow? | Share of transactions, invoices, orders, or bookings created inside the platform | Embedded payments work best when the platform already sees the payment need before the bank or processor does. |

| Is there enough payment volume? | Gross payment volume, average transaction size, frequency, and seasonality | A payment product needs enough volume to support risk, support, compliance, and implementation costs. |

| Will payments improve the user job? | Time saved, fewer tools used, lower failed-payment work, faster posting | The embedded flow should make the workflow better, not simply move fees to the platform. |

| Can the platform manage risk? | Chargebacks, fraud, disputes, account-change requests, refunds, failed payouts | Embedded payments bring operational responsibilities that software teams may not already own. |

| Can the data reconcile cleanly? | Payment-to-record match rate, missing remittance, accounting sync success | Money movement without clean data can increase manual work. |

| Does the region require local rails? | Wallet share, A2A share, card use, BNPL adoption, real-time payment availability | A global platform may need different payment products by country or region. |

Embedded payments decision model

For example, a construction software company might start with invoice links and ACH because the invoice record already lives in the platform. Later it may add card deposits, financing, or contractor payouts. A marketplace may start with buyer collection and seller payouts because it already controls both sides of the transaction. A healthcare scheduling platform may prioritize payment plans and card-on-file because the operational problem is patient collection after service. The same embedded-payments label covers all three, but the product design is different.

Metrics Embedded Payment Teams Should Track

Embedded payments need a scorecard that blends software metrics, payment metrics, finance metrics, and risk metrics. Traditional payment dashboards can miss product adoption. Traditional SaaS dashboards can miss settlement, dispute, fraud, and reconciliation quality. The right scorecard should explain whether the embedded product is growing, whether users trust it, whether it improves the workflow, and whether the economics are sustainable.

| Metric | What it shows | Why it belongs in an embedded-payment scorecard |

|---|---|---|

| Payment attachment rate | Share of eligible users or transactions using the embedded payment product | Shows whether customers see payments as part of the platform workflow. |

| Gross payment volume | Total value processed through embedded payments | Connects user adoption to revenue opportunity and operational scale. |

| Payment-method mix | Cards, ACH, wallets, A2A, instant payments, BNPL, checks, wires | Reveals whether users choose the methods the platform expected. |

| Take rate and net revenue | Payment revenue after provider, network, fraud, and support costs | Prevents the platform from confusing volume with profitable revenue. |

| Authorization and failure rate | Approved payments, failed payments, retries, and decline reasons | Shows whether users can complete the workflow reliably. |

| Reconciliation match rate | Share of payments automatically matched to invoices, orders, or accounts | Measures whether the embedded payment actually reduces back-office work. |

| Payout speed and exception rate | Time to payout, failed payouts, manual reviews, support tickets | Critical for marketplaces, gig platforms, suppliers, and service providers. |

| Disputes and fraud loss | Chargebacks, unauthorized activity, account-change incidents, loss rate | Keeps monetization aligned with risk control. |

| Retention lift | Gross and net revenue retention for users adopting payments | Connects payment product adoption to the platform business model. |

Scorecard principle The healthiest embedded-payment products do not optimize only for volume. They measure whether users adopt the product, whether it reduces workflow friction, whether payments reconcile cleanly, whether risk stays controlled, and whether the platform earns durable revenue after costs. That is why payment, finance, risk, and product teams should share the same scorecard.

90-Day Embedded Payments Review Plan

A platform does not need to build every payment feature at once. A practical review can be organized into a 90-day plan that separates opportunity sizing from product design and risk readiness. The plan below is intentionally operational. It is designed to prevent teams from jumping straight from a market forecast to a processor integration without proving the workflow problem.

| Timing | What to do | Output |

|---|---|---|

| Days 1-30 | Map eligible payment moments: invoices, orders, bookings, subscriptions, deposits, payouts, refunds, disputes, and failed-payment work. Pull baseline volume, method mix, support tickets, reconciliation pain, and payment timing. | A clear map of where payments already touch the product and where users leave the workflow to pay or get paid. |

| Days 31-60 | Choose the first embedded-payment use case. Compare cards, ACH, wallets, A2A, instant payments, BNPL, and payouts by region, user segment, risk, and operational value. | A use-case-specific product plan with adoption target, rail choice, pricing approach, risk requirements, and reporting needs. |

| Days 61-90 | Test adoption, support, reconciliation, failure handling, and economics before scaling. Review the plan with finance, risk, support, sales, compliance, and product. | A launch-ready scorecard that includes payment volume, attachment, net revenue, failure rate, reconciliation quality, disputes, and user feedback. |

The strategy should lead to a clear business decision rather than stopping at a simple prototype. Some platforms may realize that embedded payments should be implemented immediately because the workflow is already streamlined and the required transaction data is easily available. Others may discover that they first need stronger accounting systems, improved counterparty onboarding, or better financial documentation through tools like a web design invoice template to organize billing processes more effectively. That insight is important because it prevents businesses from investing in payment features that appear modern but fail to improve the user’s everyday workflow or operational efficiency.

Embedded Payments Statistics FAQ

Common questions

• What are embedded payments?

Embedded payments are payment capabilities built directly into a software, marketplace, app, or platform workflow. The user can pay, get paid, store credentials, receive payouts, or reconcile transactions without leaving the product experience.

• How large is the embedded payments market?

The answer depends on whether the estimate covers consumer payments, B2B payments, or the wider embedded-finance market. Bain estimates U.S. consumer embedded payment spend at $1.7 trillion today and projects $3.5 trillion, while Adyen and BCG estimate a $185 billion embedded payments and finance opportunity for platforms.

• Why are embedded payments important for SaaS platforms?

Payments can increase revenue per customer, improve retention, and make the platform more central to daily work. William Blair and Stripe benchmarks show stronger net revenue retention and valuation multiples for embedded-finance platforms than for software-only peers, but those benefits depend on real adoption and clean operations.

• Which regions matter most for embedded payments?

North America is a large embedded-finance market, while Asia-Pacific has strong growth momentum. The UK, India, Brazil, MENA, Canada, Europe, and the U.S. all matter for different reasons because local rails such as Faster Payments, UPI, Pix, ACH, cards, wallets, and BNPL shape product design.

• Do embedded payments only mean card processing?

No. Cards are important, but embedded payments can also include ACH, instant payments, bank transfers, wallets, BNPL, payouts, virtual cards, payment links, account validation, and reconciliation services.

• What makes embedded B2B payments different?

B2B payments carry invoice data, remittance detail, approval rules, vendor records, tax documents, and reconciliation needs. Bain estimates AP/AR services represent about 90% of B2B payment value, which shows why embedded B2B products must move information as well as funds.

• Which metrics should embedded payment teams track?

The most useful scorecard combines payment attachment, gross payment volume, net revenue, payment-method mix, authorization rate, failure rate, reconciliation match rate, payout speed, disputes, fraud loss, and retention impact.

• What is the biggest mistake platforms make?

The biggest mistake is treating payments as a monetization feature before proving that the embedded flow improves a real workflow. A platform should first prove that payments reduce user effort, improve cash flow, strengthen records, or make a transaction easier to complete.

Final Takeaway

Embedded payments are becoming a core part of platform strategy because money movement is often the missing step inside digital workflows. A platform can help users book appointments, manage invoices, match buyers and sellers, run subscriptions, or organize supplier records. But the workflow is incomplete when the user still has to leave the product to collect money, send a payment, track settlement, or reconcile the result.

The statistics show why the opportunity is large, but they also show why implementation must be selective. Consumer embedded payments are already measured in trillions. B2B embedded payment volume has a much larger transaction base to penetrate. Platform economics can improve when payment adoption is real. Regional rails such as UPI, Pix, ACH, Faster Payments, cards, wallets, and A2A methods shape what users expect. And business pain points around cost, security, timeliness, integration, and automation explain why payment products must solve workflow problems, not only process transactions.

For platform leaders, the practical goal is not to add every payment method. It is to identify the payment moment where the platform already owns the context, then build a reliable embedded flow around that moment. The strongest products make payment acceptance, payouts, reconciliation, refunds, reporting, and risk handling feel like part of the same workflow. That is when embedded payments stop being an added feature and become infrastructure that users depend on every day.