Payment gateways are often described as the invisible bridge between a customer and a merchant, but that definition is too small for how modern payments actually work. A gateway does more than move card details from a checkout form to an acquiring bank. It decides which payment methods can be shown, how transaction data is tokenized, how fraud checks are triggered, how declines are returned, how retries are handled, how settlement records are produced, and whether the finance team can match the money back to the right order, invoice, subscription, or customer account.

That is why payment gateway statistics deserve a separate scorecard. The most visible payment moment is the button press, but the most expensive payment problems often happen after the customer has already decided to pay. A legitimate card may be rejected. A local wallet may be missing. An issuer response may be too vague to diagnose. A fraud rule may block good customers. A gateway may accept the payment but produce settlement reports that are difficult to reconcile. In each case, the business loses either revenue, trust, time, or usable cash.

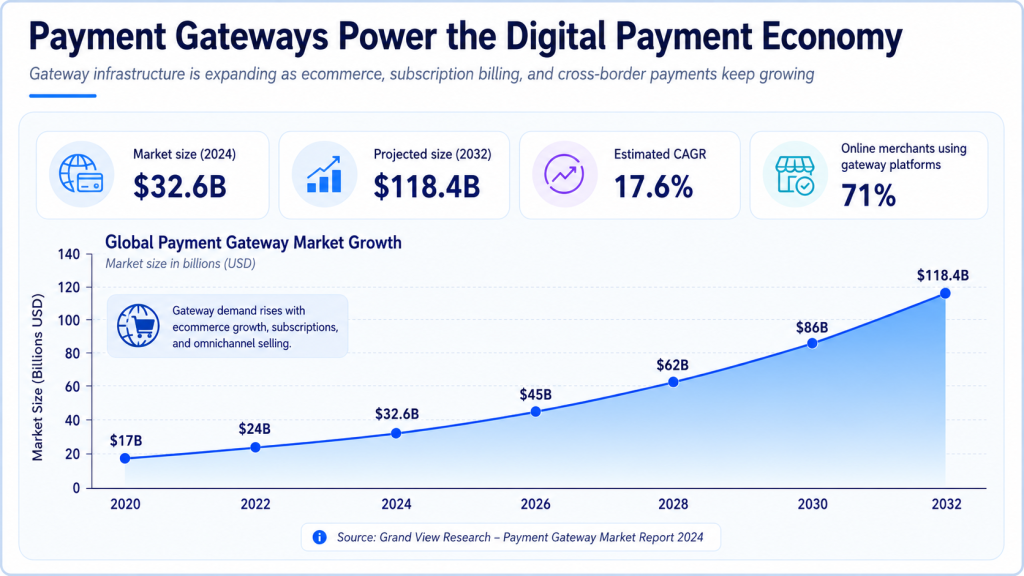

The market context is large enough to make small gateway improvements meaningful. Businesses running on Stripe generated $1.9 trillion in total payment volume in 2025, Adyen reported €1,394.3 billion in processed volume, the ACH Network processed 35.2 billion payments worth $93 trillion, and euro-area non-cash transactions reached 77.7 billion in the first half of 2025. Those figures do not mean every company needs enterprise-grade orchestration. They do show that payment infrastructure is now a strategic operating layer for ecommerce, SaaS, B2B invoicing, marketplaces, subscriptions, and international selling.

Payment gateway statistics work best as business signals rather than as a provider comparison list. Gateway performance affects authorization, fraud control, payment-method coverage, country localization, settlement, reconciliation, and payment operations. A gateway should not be judged only by whether it can process a transaction. It should be judged by how many good payments it approves, how intelligently it blocks bad ones, how clearly it reports failures, and how cleanly the money becomes usable business cash.

Executive Payment Gateway Benchmarks

The executive numbers show why gateway performance belongs in the same conversation as conversion, cash flow, fraud, and accounting quality. A merchant may spend heavily to bring a buyer to checkout, but the gateway still has to convert that intent into an approved, settled, and reconciled payment. The strongest benchmark set therefore combines market scale, authorization quality, payment-method availability, fraud pressure, and regional rail adoption.

• Businesses running on Stripe generated $1.9 trillion in total payment volume in 2025, up 34% from 2024 and equal to roughly 1.6% of global GDP.

• Adyen reported €1,394.3 billion in processed volume for 2025, including €311 billion of point-of-sale volume.

• PayPal reported a large active account and transaction base in 2025, making branded wallet and checkout coverage relevant when businesses compare gateway or PSP options.

• The ACH Network processed 35.2 billion payments worth $93 trillion in 2025, while Same Day ACH reached 1.4 billion payments worth $3.9 trillion.

• Euro-area non-cash payments reached 77.7 billion transactions worth €116.0 trillion in the first half of 2025, with cards leading transaction count and credit transfers leading value.

• Checkout.com research found $50.7 billion in false-decline losses across the U.S., U.K., France, and Germany, showing how payment performance can erase ready-to-pay demand.

• After one false decline, 45% of consumers said they would not retry, and 42% said they would not return to the app or website.

• Adyen’s 2025 retail research found 51% of shoppers may walk away if they cannot use their preferred payment method.

• India’s UPI crossed 2,000 crore monthly transactions for the first time in August 2025 and reached 2,163 crore transactions in December 2025.

• Brazil’s Pix recorded about 68.7 billion transactions in 2024, a reminder that gateways serving Brazil need more than card coverage.

• The U.K. recorded 48.8 billion payments in 2024, with card payments accounting for a large majority of transaction volume and Faster Payments remaining central to bank-transfer behavior.

• Canada’s 2024 payment research found mobile payments approaching 5% of transactions, while online purchases represented a much larger remote-payment surface.

• Checkout.com also reported that 50% of merchants did not receive raw response codes on failed payments, while 45% lacked actionable payment-provider insights.

Editorial readout Gateway statistics point to five connected questions: can the business offer the customer’s preferred method, can it authorize legitimate payments, can it reduce fraud without over-blocking, can it localize by country, and can it produce clean settlement records after the payment succeeds? A gateway that performs well on only one of those dimensions can still leave revenue or operational clarity on the table.

Why Gateways Matter After the Customer Clicks Pay

A customer pressing the payment button is not the finish line. It is the start of a technical and financial sequence that determines whether the business captures revenue. The gateway collects payment credentials or tokenized wallet data, passes the request into the acquiring or processor environment, triggers fraud and authentication checks, receives an issuer or bank response, returns a success or failure message, and later produces settlement and reporting records. Each step can improve or damage the payment outcome.

This is why gateway quality can be invisible until something goes wrong. A merchant may see a checkout page that looks clean and still have a weak approval rate because card routing is poor, response data is vague, or fraud rules are too aggressive. A subscription company may have an attractive pricing page and still lose recurring revenue because failed-payment retries are badly timed. A B2B seller may accept invoice payments online and still spend hours reconciling deposits because the gateway report does not carry enough customer or invoice detail.

The gateway is therefore a control layer. It affects conversion because payment failure happens after customer intent. It affects cash flow because settlement timing and payout reporting decide when money becomes useful. It affects risk because fraud rules, 3DS, tokenization, and dispute evidence shape both losses and false positives. It affects operations because accounting teams need to match approved transactions to bank deposits, fees, refunds, and chargebacks.

A useful gateway review should begin with the full payment lifecycle: payment shown, payment selected, payment submitted, payment approved or declined, payment retried if needed, funds settled, fees recorded, refund or dispute handled, and transaction matched to a business record. When companies review only the front-end checkout, they usually miss the infrastructure issues that cause the most expensive leaks.

• A polished checkout can still lose money if the gateway returns unclear declines, blocks legitimate customers, or fails to support local methods.

• A gateway should be measured by successful payment outcomes, not only by technical integration or headline transaction fees.

• The most useful gateway dashboard separates customer-side failure from issuer decline, fraud block, processor error, timeout, authentication failure, and reconciliation problem.

• For invoice-led businesses, the gateway should connect payments to customers, invoice numbers, fees, refunds, and settlement batches rather than only showing a transaction ID.

Gateway principle The gateway is not simply a route to a card network. It is the operating system that turns payment intent into approved funds, risk decisions, and accounting records.

Payment Gateway Market Scale and Provider Volume

Gateway scale statistics should be used carefully. A large provider is not automatically the right provider for every business, and a smaller specialist can be better for a narrow regional or business-model requirement. Still, provider and rail scale helps explain why gateway decisions deserve serious attention. The volumes processed through major platforms and bank rails are large enough that small approval, routing, or reporting differences can translate into meaningful business outcomes.

Stripe’s 2025 volume illustrates how much commerce can sit behind one payment infrastructure layer. Businesses running on Stripe generated $1.9 trillion in total volume, up 34% year over year. Adyen provides another global acquiring and platform benchmark, with €1,394.3 billion in processed volume and €311 billion in point-of-sale volume for 2025. Worldpay and Global Payments reporting provides another scale reference, while PayPal’s account and transaction base shows why branded wallet acceptance can still matter for merchants that serve consumers across markets.

Bank rails add a different kind of scale. ACH processed 35.2 billion payments worth $93 trillion in 2025, which is far larger in value than many checkout-centered payment discussions suggest. That matters for gateways and payment platforms because invoice payment, recurring billing, B2B payments, payroll-adjacent flows, and account-to-account methods often depend on bank-based payment infrastructure rather than card-only processing.

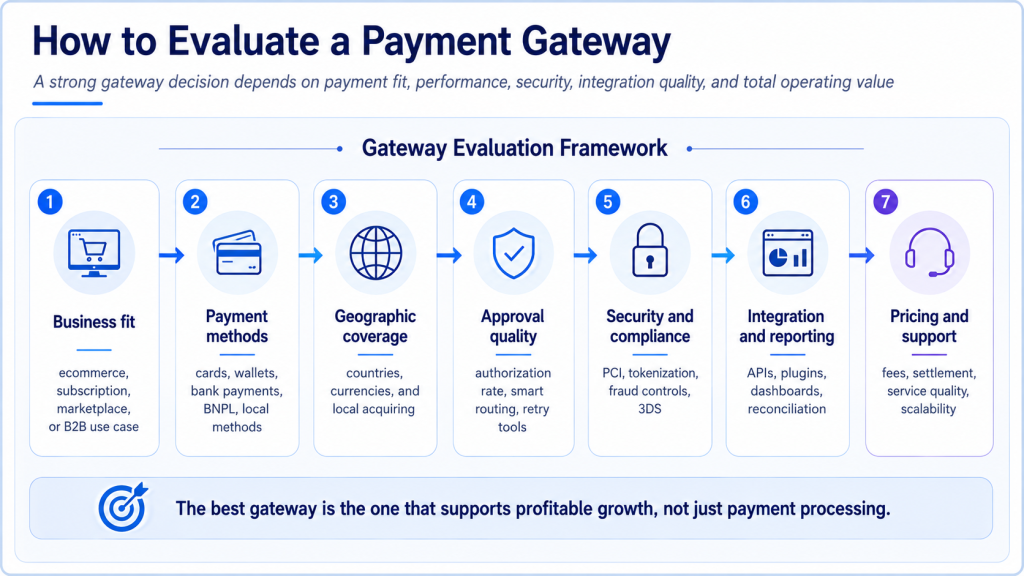

The provider lesson is not to choose the biggest name by default. A business should compare coverage, authorization performance, fraud controls, integration depth, payout timing, dispute handling, regional payment methods, accounting exports, and support quality. Scale may indicate resilience and breadth, but the better question is whether the gateway improves the company’s actual payment outcomes in its actual markets.

Figure 1. Gateway and processor scale should be reviewed as payment infrastructure context, not as a provider ranking.

• Provider scale can indicate network reach, but approval quality and data transparency matter more to daily revenue capture.

• Processor volume should be compared with business fit: ecommerce, SaaS, marketplace, invoice payment, or local-payment coverage may require different capabilities.

• Bank-rail scale is especially important for B2B and recurring use cases, where ACH, direct debit, open banking, or instant transfers may fit better than card entry.

• A gateway decision should include the cost of operational work: reconciliation, failed-payment analysis, refunds, disputes, and support tickets.

Authorization Rates, False Declines, and Lost Revenue

Authorization is one of the clearest reasons gateway statistics matter. A shopper can choose a product, enter payment details, pass the front-end form, and still fail to become a customer if the payment is declined. Some declines are valid. Others are false positives, soft declines, preventable issuer responses, routing issues, authentication failures, or fraud-rule decisions that should have been tuned differently.

The false-decline data is powerful because it measures lost demand after intent already exists. Checkout.com’s research identified $50.7 billion in false-decline losses across the U.S., U.K., France, and Germany. The customer behavior numbers are just as important: 45% of consumers said they would not retry after one false decline, and 42% said they would not return to the app or website. That means a decline can become a brand and loyalty event, not only a payment error.

Gateway reporting determines whether a business can fix the problem. If the merchant receives only a generic ‘payment failed’ message, the team cannot separate insufficient funds from suspected fraud, issuer decline, authentication failure, expired card, bank outage, processor timeout, or incorrect payment data. Checkout.com’s finding that 50% of merchants did not receive raw response codes and 45% lacked actionable insights shows why gateway analytics can be as important as the payment method itself.

Authorization improvement can involve several layers. A business may need better retry rules for soft declines, local acquiring in specific countries, wallet support for mobile users, account updater tools for subscriptions, clearer payment error messages, fallback methods, or fraud model tuning. The correct fix depends on the decline reason. That is why authorization should be measured by country, issuer, payment method, device, customer segment, and transaction type rather than as one blended approval rate.

For subscriptions and invoice payments, the same logic applies after the first transaction. A failed renewal, expired card, blocked ACH debit, or unclear payment link can become involuntary churn or delayed cash. Gateway statistics should therefore include retry success, recovery after failure, time to recovery, and whether the customer needed manual support to complete the payment.

Figure 2. Payment failure, false declines, and missing response data show why gateway analytics affect revenue recovery.

• False declines are especially expensive because acquisition cost has already been spent and the customer has already shown intent.

• A soft decline should not be treated the same as a hard fraud block; gateway response data should guide retry and customer messaging.

• Authorization rate should be reviewed with fraud rate, chargeback rate, and false-positive behavior so that risk controls do not quietly reject good customers.

• A gateway that improves approval but creates more fraud or chargebacks is not truly better; the scorecard has to combine revenue and risk quality.

Authorization readout The gateway’s job is not to approve every payment. It is to approve legitimate payments as reliably as possible while giving the business enough response data to understand and reduce preventable failure.

Payment Method Coverage: Gateways as Localization Infrastructure

Payment-method coverage is often presented as a feature checklist: cards, wallets, ACH, bank transfer, BNPL, UPI, Pix, Faster Payments, SEPA, and local wallets. That list is useful only if the methods actually match the markets and business models the company serves. A gateway that supports many methods globally may still be weak in the one country where a merchant is trying to grow. A gateway that supports the right local method may still create problems if refunds, settlement, and reporting are difficult.

Adyen’s retail research found that 51% of shoppers may walk away if they cannot use their preferred payment method. That finding should not be read as an instruction to add every method everywhere. It means payment choice should be localized and measured. A wallet button may be critical on mobile. ACH may be better for recurring invoices. UPI may be essential in India. Pix may be necessary for Brazil. Cards may still dominate a U.S. consumer checkout. Credit transfers may matter for high-value euro-area movement.

Gateway localization should also consider the behind-the-scenes work. Does the gateway support local acquiring? Does it return useful decline codes? Does it handle refunds in the same rail? Can it reconcile bank transfers to orders or invoices? Can it support payment links, recurring authorization, statement descriptors, dispute evidence, and settlement timing in the country being served? A method that increases conversion but creates operational confusion may not be a clean improvement.

Gateway planning differs from broad online payment coverage. The question is not simply which payment methods are growing. The gateway question is which provider can reliably expose those methods to customers, authorize them well, settle them predictably, report them clearly, and support refunds or disputes when something changes after payment.

• Cards remain baseline infrastructure in many markets, but card performance depends on authorization, fraud rules, issuer behavior, and routing.

• Wallets reduce typing and can improve mobile completion, but wallet-funded transactions still need authorization, fraud, refund, and reconciliation review.

• ACH and direct debit can be strong for invoices, subscriptions, retainers, and recurring payments when authorization and remittance data are clean.

• UPI and Pix are examples of local rails that can become core gateway requirements rather than optional alternative payment methods.

• BNPL can affect conversion and order value, but gateways and merchants still need to monitor fees, returns, disputes, and customer quality.

Payment-method rule A payment method should be considered supported only when the full operating loop works: display, authentication, approval, settlement, refund, dispute handling, and reporting.

Regional Payment Gateway Intelligence

Regional data deserves a major place in payment gateway planning because gateways are often chosen during expansion. A company may begin with one domestic card processor, then discover that a new market needs local acquiring, a popular wallet, bank transfer, instant payment, invoice payment, or a different settlement structure. Payment localization is not only about showing the right currency. It is about giving customers a familiar payment route and giving the business clean operational records afterward.

The United States remains heavily influenced by cards, wallets, ACH, and subscription-style payment infrastructure. ACH scale is especially important for invoice payment, payroll-adjacent flows, B2B payments, recurring billing, and account-to-account use cases. Same Day ACH’s 1.4 billion payments and $3.9 trillion value in 2025 show that faster bank movement has become material, not experimental. For U.S. gateways, the practical question is whether card approval, ACH authorization, retry logic, fraud controls, and accounting exports are all strong enough for the use case.

Canada should not be treated as a small version of the U.S. Bank of Canada research shows mobile payments approaching 5% of transactions in 2024, while remote and online buying remain a distinct payment surface. A Canada-facing gateway needs to consider cards, mobile wallet behavior, Interac-style expectations, bank-transfer habits, and local reporting requirements separately from U.S. assumptions.

The United Kingdom combines card maturity with strong bank-transfer behavior. UK Finance reported 48.8 billion payments in 2024, with card payments representing a large share of transaction volume and Faster Payments remaining central to remote banking. A U.K. gateway decision should compare card authorization, wallet acceptance, open-banking or pay-by-bank options, Direct Debit and recurring payment support, and payout or settlement reporting.

Europe requires even more country-level discipline. ECB statistics show 77.7 billion euro-area non-cash transactions worth €116.0 trillion in the first half of 2025. Cards represented 57% of transaction count, but credit transfers represented most of the value. That split matters for gateway planning. A low-value ecommerce merchant, a high-value B2B seller, and a subscription company may need different European gateway capabilities even if all are operating in the same currency area.

Germany, France, Italy, and Poland are useful reminders that Europe is not one method mix. Poland’s account-to-account strength means a card-only assumption can underperform. Germany and France may require careful handling of wallets, cards, bank transfers, authentication, and local customer trust. Italy can have its own wallet and card behavior. A gateway serving Europe should therefore be evaluated by country coverage, not only by a single regional label.

India is one of the clearest cases where local rail support becomes gateway infrastructure. UPI crossed 2,000 crore monthly transactions for the first time in August 2025 and reached 2,163 crore in December. For an India-facing payment flow, UPI visibility, bank response handling, QR or intent flow quality, failed-payment messaging, and reconciliation are core product requirements.

Brazil offers a different version of the same lesson. Pix recorded about 68.7 billion transactions in 2024 and has become a mainstream payment rail across consumer and business contexts. A Brazil-facing gateway needs to think about Pix confirmation, QR flows, payment links, refunds, recurring Pix developments, settlement timing, and how Pix transactions are matched to orders or invoices. Treating Pix as a minor alternative method would miss the local payment reality.

China and parts of APAC show how wallet-led behavior can make the gateway decision depend heavily on local networks and partnerships. In markets where wallets dominate ecommerce or mobile commerce, the business may need local acquiring, wallet integrations, platform-specific approval behavior, and localized customer support. Latin America adds yet another pattern: local cards, installments, Pix in Brazil, cash alternatives, bank transfers, and country-specific methods can all matter depending on the market.

Figure 3. Regional rail scale shows why gateways must be evaluated by country and use case, not only by global method support.

Figure 4. Euro-area payment data shows why transaction count and payment value may point to different gateway requirements.

The country detail is important because a gateway can appear complete on a provider feature page and still be incomplete in the market where the customer is paying. The useful test is not whether the gateway has a long payment-method list. It is whether the specific method in that country can be shown at the right moment, authorized reliably, refunded cleanly, settled predictably, and matched back to the right customer record.

• For a U.S. invoice or subscription flow, ACH and Same Day ACH support should be evaluated with bank-account authorization, return handling, failed-payment recovery, and invoice matching, not only with payment availability.

• For the euro area, card transaction count and credit-transfer value point to different gateway requirements: consumer checkout needs card and wallet performance, while higher-value business movement often needs transfer reporting and settlement clarity.

• For India, UPI scale means gateway reliability, QR/payment-link behavior, bank response handling, refund paths, and reconciliation references can be central to the product experience rather than optional local features.

• For Brazil, Pix support should be reviewed across checkout, payment links, QR codes, instant confirmation, refunds, and B2B settlement because the same rail can serve several payment jobs.

• For APAC wallet-led markets, the gateway decision may depend on local partnerships, tokenization, wallet routing, authentication, and local dispute or refund norms more than on the global card form.

| Market signal | Gateway lesson |

|---|---|

| United States | Protect card approval, but treat ACH, Same Day ACH, subscriptions, and invoice payment links as operating workflows with return and reconciliation needs. |

| Canada | Do not simply reuse a U.S. setup; review card behavior, online purchase patterns, mobile payments, Interac-style expectations, and local settlement reporting. |

| United Kingdom | Card acceptance remains important, but Faster Payments, Direct Debit, open banking, and pay-by-bank use cases can affect invoice and service payments. |

| Euro area | A gateway serving Europe should separate card checkout from credit-transfer value, SEPA logic, instant transfer adoption, authentication, and country-level method preferences. |

| India | UPI support should be treated as core payment infrastructure for India-facing products, with careful testing of confirmation, refunds, QR flows, and reconciliation. |

| Brazil | Pix should be evaluated as consumer checkout, QR/payment-link, instant bank-payment, and B2B settlement infrastructure rather than one generic local method. |

| Poland / selected Europe | A2A-heavy markets warn against card-only assumptions; local bank-payment behavior may decide whether checkout feels familiar. |

| China / APAC | Wallet-first behavior can make local gateway or partner coverage as important as price, especially for mobile-first commerce. |

Regional gateway rule Local payment support should be tested as an operating workflow. A method is not fully supported until the business can authorize it, reverse or refund it, settle it, explain it to the customer, and reconcile it without manual cleanup.

Fraud, Chargebacks, and Gateway Risk Controls

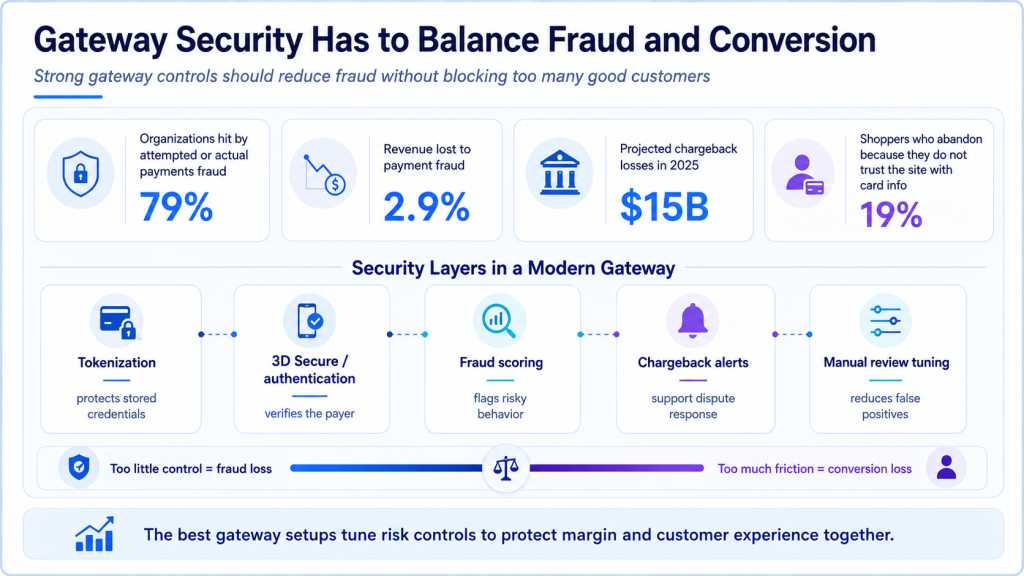

Fraud control is one of the main reasons businesses rely on gateways and payment service providers, but risk management can become a hidden conversion problem if it is measured too narrowly. A fraud system that blocks every suspicious-looking transaction may reduce loss, but it may also reject real customers. A system that approves too freely may raise chargebacks, disputes, and support workload. The gateway’s role is to help the business find the balance.

Chargebacks and fraud are not only ecommerce issues. They also affect subscriptions, digital services, marketplaces, high-ticket retail, travel, professional services, and invoice payments that use card or wallet rails. Mastercard-sponsored research cited in payments coverage estimated that sellers could lose $15 billion to fraudulent chargebacks in 2025. That figure does not mean every dispute is fraud, but it shows why gateway dispute evidence, reason-code analysis, authentication logs, customer communication, and refund history matter.

Gateways influence risk through several mechanisms: tokenization, risk scoring, device data, 3DS or strong customer authentication support, rules-based blocking, machine-learning review, velocity checks, address verification, card security checks, and dispute evidence collection. The quality of those tools matters, but so does how they are configured. A rule that works for domestic low-ticket purchases may be too strict for international customers. A rule that works for physical goods may not fit digital subscriptions. A rule that blocks new cards aggressively may create false declines for legitimate first-time buyers.

The best risk dashboard connects fraud, authorization, and customer impact. If fraud falls while false declines rise, the business may simply be rejecting more good customers. If approvals rise while chargebacks increase, the business may be accepting too much risk. If a new authentication flow reduces fraud but also reduces mobile conversion, the gateway team needs to tune the user experience, not just celebrate lower losses.

• Fraud rate should be reviewed with authorization rate and chargeback rate, not as a standalone success metric.

• Chargeback reason codes can reveal preventable issues such as unclear descriptors, delayed fulfillment, weak refund communication, or subscription cancellation confusion.

• Risk rules should be segmented by market, method, ticket size, product type, customer history, and device rather than applied as one global filter.

• False-positive review is a revenue-protection activity because a legitimate buyer wrongly rejected may not retry.

Risk interpretation Gateway risk controls should protect margin without turning payment acceptance into a blunt instrument. The strongest programs reduce fraud, preserve good approvals, and give teams enough evidence to resolve disputes quickly.

Gateway Reliability, Uptime, and Failed Payment Handling

Reliability is easy to overlook when payments are working. It becomes obvious when customers see spinning buttons, duplicate attempts, unexplained failures, delayed confirmations, or support tickets asking whether an order went through. Gateway uptime, API response, status transparency, retry handling, and incident communication all affect customer trust.

A payment failure is not always a decline. It can be a timeout, authentication interruption, bank response delay, malformed request, duplicate submission, connectivity problem, wallet handoff issue, or processor incident. From the customer’s perspective, many of these problems look the same: the payment did not work. From the business perspective, they need very different fixes. That is why gateway error reporting must separate technical failure from issuer decline and risk block.

Subscription and recurring-payment businesses should pay special attention to reliability because failed renewals can compound. A small outage, card updater issue, or retry timing problem can become involuntary churn if customers are not notified clearly. Invoice payment links create another reliability need: customers may click from an email weeks after an invoice was sent, so links, authorization, and payment status must remain clear.

Larger businesses may use backup routing, provider redundancy, or payment orchestration to reduce the impact of provider-specific incidents. Smaller businesses may not need complex orchestration, but they still need a basic reliability checklist: monitor gateway errors, review decline categories, keep payment pages tested, check settlement reports, and make customer-facing error messages specific enough to reduce support confusion.

| Gateway problem | What the customer sees | What the business should measure |

|---|---|---|

| Timeout or API failure | Payment appears to hang or fail | Gateway error rate, retry success, duplicate-attempt rate |

| Issuer decline | Payment is rejected at checkout | Decline reason, approval rate, customer retry behavior |

| Risk block | A legitimate buyer may be blocked | False-positive review, fraud rule impact, manual review outcome |

| Authentication friction | Customer abandons during 3DS or bank step | Authentication completion, challenge rate, device split |

| Settlement mismatch | Finance cannot match deposit to transaction | Payout report quality, reconciliation match rate, fee visibility |

Payment Orchestration and Multi-Provider Routing

Payment orchestration enters the discussion when a single gateway is not enough. A company selling in multiple countries, handling high transaction volume, or operating several business models may want to route payments by market, method, issuer, cost, risk profile, or provider availability. Orchestration can also support fallback routing when one provider is unavailable or when a transaction has a better chance of approval through another path.

The case for orchestration is strongest when payment performance varies meaningfully by country or method. A business may find that one provider performs well for U.S. cards, another has stronger local acquiring in Europe, and a third handles a specific wallet or bank rail better in Latin America. Routing logic can then become a revenue tool rather than only a technical architecture choice.

However, orchestration is not automatically better for every company. It can add integration complexity, reporting complexity, settlement fragmentation, dispute-process variation, and vendor management work. A smaller merchant with one primary country and simple payment needs may be better served by a single provider with strong reporting. A global merchant with high payment volume, many methods, and clear approval-rate differences may benefit from a multi-provider strategy.

A practical orchestration decision should compare the expected gain against the operational burden. If fallback routing improves approval but creates reconciliation confusion, the finance team may lose some of the benefit. If cost routing reduces fees but lowers approval quality, revenue may suffer. The right routing strategy should optimize successful, profitable, reconciled payments, not only the cheapest path.

• Use orchestration when provider performance differences are large enough to justify extra operational complexity.

• Route by country and method before building overly complex rules around small theoretical savings.

• Treat provider redundancy as an availability strategy, but verify that reporting, refunds, and disputes remain manageable.

• Measure cost per successful payment, not just headline processing fee, because failed payments and reconciliation work also cost money.

Orchestration rule Multi-provider routing is valuable only when it improves the full payment outcome: authorization, risk, cost, settlement, reporting, and customer experience.

Settlement, Reconciliation, and Reporting

A gateway has not finished its job when a payment is approved. The business still has to know when money will arrive, which fees were deducted, which transaction belongs to which order or invoice, which refunds changed the payout, which chargebacks reduced settlement, and which bank deposits match the processor report. That is why settlement and reconciliation belong in a complete gateway review.

For ecommerce teams, reconciliation may mean matching orders, refunds, chargebacks, taxes, and shipping adjustments. For subscription companies, it may mean matching renewals, upgrades, credits, failed retries, and customer account changes. For B2B invoice payment, it may mean matching a payment link or ACH debit to invoice number, remittance detail, customer name, and batch deposit. For marketplaces, it may mean splitting fees, seller payouts, reserves, refunds, and dispute holds.

Gateway reporting gaps create hidden labor. A payment can be approved and still create accounting work if the payout report does not line up with the bank deposit. A refund can be issued and still confuse the customer if the original transaction, fee reversal, and timing are unclear. A chargeback can be posted and still create internal confusion if the finance team cannot link it to the order and evidence package quickly.

The most practical gateway reporting test is simple: can a finance person trace one transaction from customer payment to authorization, fee, settlement batch, refund or dispute if applicable, and accounting record without guessing? If not, the gateway may be creating operational drag even if payment acceptance looks healthy.

| Reporting field | Why it matters |

|---|---|

| Transaction ID and customer record | Links payment to order, invoice, subscription, or account |

| Authorization and decline details | Explains whether payment succeeded, failed, or needs retry |

| Settlement batch and payout date | Shows when funds become usable cash |

| Fees and adjustments | Prevents margin and bank-deposit confusion |

| Refunds and chargebacks | Connects customer service events to payment records |

| Payment method and country | Supports regional performance analysis and method-level cost review |

| Reconciliation status | Shows whether accounting has matched funds to the correct record |

Gateway Requirements by Business Model

Different businesses need different gateway strengths. A payment gateway for a high-volume ecommerce store should emphasize checkout speed, wallet support, fraud tuning, authorization, and refunds. A subscription business needs stored credentials, account updater, retry logic, dunning support, and clear renewal reporting. A B2B invoicing business needs ACH, payment links, remittance data, customer-level reporting, and reconciliation. A marketplace needs split payments, seller onboarding, payouts, reserves, chargeback handling, and regulatory controls.

This is why provider comparisons can be misleading when they ignore business model. A gateway with strong card checkout may not be ideal for complex marketplace payouts. A gateway with excellent invoice payment links may not be the best fit for international ecommerce. A gateway with low fees may create too much manual work if settlement reporting is weak. The right evaluation starts with the payment journey and then chooses infrastructure to support it.

For Zintego-style customers, the invoice and business-document angle matters especially. A small business may care less about advanced orchestration and more about whether a customer can pay an invoice link easily, whether ACH and card options are clear, whether the payment is tied to the right invoice, and whether the owner can see paid, unpaid, refunded, and disputed amounts without spreadsheet cleanup.

Practical Gateway Scenarios

The easiest way to keep gateway statistics useful is to connect them to common business situations. The same payment failure can mean different things depending on the model. A failed ecommerce card payment may be a conversion problem. A failed subscription renewal may become churn. A failed invoice payment may delay cash collection. A failed marketplace payout may damage seller trust. A gateway scorecard should therefore start with the job the payment is supposed to complete.

Consider a mid-sized ecommerce brand expanding from one domestic market into three new countries. The front-end checkout may still look polished, but the gateway problem changes by market. One country may need a local wallet, another may need bank transfer, and another may need better issuer routing for cards. If the team only reviews blended conversion, it may miss that the same product page converts well in one country and fails at payment in another.

A SaaS company has a different gateway problem. The first payment matters, but recurring renewal quality matters more over time. The gateway should support stored credentials, smart retries, account updater logic, clear decline reasons, customer notifications, and reporting that separates voluntary cancellation from involuntary churn. A small improvement in retry success can be more valuable than adding another one-time checkout method.

An invoice-based service business needs yet another setup. The customer may not be shopping in a cart; they may be paying a balance after work is completed. For that business, payment links, ACH, card choice, remittance detail, invoice number matching, partial payment handling, and settlement reports can matter more than checkout speed. The gateway should help the owner know which invoice was paid and which deposit includes fees, refunds, or disputes.

Marketplaces and platforms add the hardest layer. The gateway or payment platform must manage buyer collection, seller onboarding, split settlement, payouts, refunds, reserves, disputes, and regulatory checks. A marketplace can process a buyer payment successfully and still fail the seller experience if payouts are late, payout statuses are unclear, or disputes reduce settlement without enough explanation.

| Scenario | Gateway question | Metric to watch |

|---|---|---|

| Mobile ecommerce checkout | Is the preferred wallet or local method visible and reliable on the device the customer uses? | Mobile payment completion, wallet conversion, authorization by country |

| SaaS renewal | Can the gateway recover good customers after a failed recurring payment? | Retry success, involuntary churn, decline reason, updater rate |

| Invoice payment link | Can the payment be matched to the right customer, invoice, fee, refund, or dispute? | Time to paid, reconciliation match rate, ACH/card mix, unapplied payments |

| Marketplace payout | Can the platform collect from buyers and pay sellers predictably? | Payout timing, failed payout rate, reserve holds, dispute impact |

| International expansion | Does the gateway support the methods and settlement rules customers expect locally? | Country conversion, local-method share, refund time, support tickets |

• A gateway problem should be diagnosed by business model before the team changes providers or adds payment methods.

• A provider that works well for card checkout may not be enough for subscriptions, invoice payment links, payouts, or cross-border settlement.

• The best scenario review asks what the payment must accomplish after approval: renewal, invoice closure, seller payout, refund, reconciliation, or fraud decision.

Scenario readout Gateway performance is strongest when the provider, rail, risk rules, settlement reports, and support process fit the business model. A generic gateway comparison misses that operating context.

International sellers need an additional layer: local method coverage, currency handling, tax and receipt clarity, refund expectations, and settlement geography. The payment gateway becomes part of the expansion plan because a weak local payment experience can make a new market look less attractive than it really is.

| Business model | Gateway priorities |

|---|---|

| Ecommerce | Wallets, card approval, fraud rules, refunds, mobile checkout, payment-method testing |

| SaaS / subscriptions | Stored credentials, retries, account updater, failed-payment recovery, renewal reporting |

| B2B invoices | ACH, payment links, remittance detail, invoice matching, settlement reporting |

| Marketplaces | Split payments, seller onboarding, payouts, reserves, disputes, KYB controls |

| Professional services | Deposits, retainers, card/ACH choice, payment links, refund clarity |

| International sellers | Local methods, FX, taxes, local acquiring, country-level settlement and support |

| High-risk categories | Stronger fraud scoring, manual review, dispute evidence, chargeback monitoring |

Common Gateway Decision Mistakes

Gateway decisions often go wrong when teams focus on one visible metric and ignore the rest of the payment lifecycle. The most common example is choosing by headline processing fee. Fees matter, especially for low-margin businesses, but the cheapest route may not be the lowest-cost route if it lowers authorization, creates more support tickets, delays settlement, or makes reconciliation harder.

Another mistake is adding payment methods without measuring completion. A new wallet, BNPL option, bank rail, or local method should be tested by method-level conversion, approval, cost, refund behavior, dispute rate, and support volume. If the method attracts clicks but does not complete cleanly, the business needs to understand why.

A third mistake is separating fraud from revenue. Fraud teams may optimize for fewer bad transactions, while growth teams optimize for more approvals. A gateway scorecard should force those metrics together. Otherwise, the business may celebrate fraud reduction while missing that legitimate customers are being blocked, or celebrate approval gains while chargebacks rise.

The last major mistake is ignoring reporting until after implementation. Payment reporting is not a back-office detail. It determines whether the business can trust its numbers. If settlement exports, fees, refunds, disputes, and invoice references are unclear, the gateway creates work every month. That work may not appear in the provider quote, but it is still part of the real cost.

• Do not choose a gateway only by headline fee; compare cost per successful, settled, and reconciled payment.

• Do not add payment methods only because they are available; measure whether they improve completed, profitable payments.

• Do not judge fraud tools without measuring false positives and customer retry behavior.

• Do not expand internationally without checking local payment methods, local acquiring, refunds, and reporting.

• Do not treat settlement and reconciliation as finance-only issues; they are part of payment product quality.

Payment Gateway Metrics Businesses Should Track

The best gateway scorecard is not the largest dashboard. It is the one that helps the business decide where payment value is being lost or where operational work is increasing. A merchant that tracks only total payments processed may miss preventable declines. A company that tracks only fraud may miss false positives. A finance team that tracks only bank deposits may miss which payment method or provider created the reconciliation issue.

Gateway metrics should be segmented by country, payment method, device, customer type, product type, and transaction size where volume supports it. A blended approval rate may look stable while one country, issuer, card type, or wallet flow performs poorly. A blended chargeback rate may hide one product line or customer segment. The point of segmentation is not complexity for its own sake; it is to identify the leak that can actually be fixed.

Figure 5. Gateway scorecards should combine customer choice, authorization quality, risk, settlement, and operating visibility.

| Metric | Why it matters |

|---|---|

| Authorization rate | Shows how many submitted payments become approved transactions |

| Decline rate by reason | Separates issuer decline, fraud block, authentication failure, and technical error |

| False-decline estimate | Identifies legitimate demand being wrongly rejected |

| Retry success rate | Shows whether failed payments are recovered or lost |

| Payment-method conversion | Compares cards, wallets, ACH, bank transfer, BNPL, UPI, Pix, and local methods |

| Gateway error rate | Measures timeout, API failure, duplicate attempt, or provider incident impact |

| Fraud rate | Tracks confirmed bad transactions and suspicious activity |

| Chargeback rate | Measures dispute exposure and possible customer-experience issues |

| Settlement time | Shows when approved money becomes usable cash |

| Reconciliation match rate | Shows whether payments connect cleanly to accounting records |

| Refund processing time | Connects payment operations to customer support quality |

| Cost per successful payment | Combines fees, failed payments, disputes, and operational work |

A 90-Day Payment Gateway Improvement Plan

Payment gateway improvement does not need to begin with a full provider migration. In many businesses, the first gains come from measuring the current setup properly, identifying preventable failures, cleaning up reporting, and changing a small number of high-impact rules. A 90-day review is long enough to observe payment behavior but short enough to prevent gateway issues from becoming normal background noise.

The first month should build the baseline. The business should measure authorization, decline reasons, gateway errors, fraud, chargebacks, refund timing, settlement timing, and reconciliation issues by country and method. This baseline often reveals that the biggest leak is not the one the team expected. A merchant may discover that one country has weak authorization, one wallet has high abandonment, one fraud rule blocks too many good customers, or one settlement report creates most of the accounting work.

The second month should focus on high-confidence fixes. These may include clearer payment error messages, better retry rules, payment-link cleanup, local method placement, fraud-rule tuning, settlement report changes, or adding a payment method in one market where demand is clear. The goal is not to redesign everything. It is to fix visible leaks with before-and-after metrics.

The third month should decide whether larger changes are needed. If approval remains weak in a key country, the business may need local acquiring or another provider. If outages or gateway errors are material, fallback routing may be worth exploring. If reconciliation remains messy, accounting integration may be the priority. If fraud and false positives both remain high, risk tooling needs a deeper review.

| Timing | What to do | Output |

|---|---|---|

| Days 1-30 | Baseline gateway performance by country, method, device, decline reason, fraud, chargebacks, settlement, and reconciliation | A clear map of where payments fail or create work |

| Days 31-60 | Fix high-confidence leaks such as unclear declines, weak retries, missing local methods, excessive risk blocks, and reporting gaps | Controlled improvements with before/after metrics |

| Days 61-90 | Review provider fit, orchestration need, risk tuning, settlement quality, and accounting integration | A repeatable gateway scorecard and improvement roadmap |

Payment Gateway Statistics FAQ

Common questions

• What is a payment gateway?

A payment gateway is the infrastructure layer that captures payment information, routes the transaction for authorization, applies risk or authentication logic, returns the payment result, and supports settlement and reporting. In practice, many gateway or payment-service-provider platforms also support wallets, bank payments, fraud tools, subscriptions, invoices, and reconciliation exports.

• Why do payment gateway statistics matter?

They show where payment value can be lost after the customer has already decided to pay. Gateway statistics help businesses understand authorization, false declines, payment-method fit, fraud exposure, settlement timing, and reporting quality.

• What is a good gateway authorization rate?

There is no universal rate because approval depends on country, method, issuer, fraud mix, ticket size, and customer type. The useful benchmark is improvement by segment: card type, issuer, wallet, country, device, and decline reason.

• How do false declines affect revenue?

False declines reject legitimate customers. Checkout.com research found $50.7 billion in false-decline losses across four major markets, and many customers say they will not retry or return after a failed payment.

• What payment methods should a gateway support?

The right mix depends on the market and business model. Cards and wallets may be essential in one market, ACH or direct debit in another, UPI in India, Pix in Brazil, and bank transfers or open banking in selected European use cases.

• How do gateways help prevent fraud?

Gateways can support tokenization, fraud scoring, device checks, velocity rules, 3DS or strong customer authentication, manual review, and dispute evidence. The challenge is reducing fraud without blocking too many legitimate buyers.

• What is payment orchestration?

Payment orchestration routes transactions across providers, methods, acquirers, or regions to improve approval, cost, redundancy, or coverage. It is most useful when transaction volume and country complexity justify the added operational work.

• How should businesses compare payment gateways?

They should compare authorization quality, local method coverage, fraud tools, reporting, settlement timing, integration fit, support, refunds, disputes, and cost per successful payment, not only headline processing fees.

• Why does regional payment support matter?

Customers in different countries expect different payment paths. A gateway that performs well for U.S. cards may not be enough for India UPI, Brazil Pix, euro-area credit transfers, U.K. Faster Payments, or local wallets in APAC.

• Which gateway metrics should businesses track?

Core metrics include authorization rate, decline reason, false-decline estimate, retry success, payment-method conversion, fraud rate, chargeback rate, gateway error rate, settlement time, reconciliation match rate, refund time, and cost per successful payment.

Final Takeaway

Payment gateways should be judged by completed outcomes, not by payment forms alone. A customer can see a payment button and still fail to pay. A merchant can receive an approval and still struggle to reconcile the deposit. A fraud rule can protect the business and still reject too many good customers. A gateway can support a long list of methods and still underperform in a specific country if the local method, authorization, refund, or reporting workflow is weak.

The statistics point to a practical conclusion: gateway performance sits at the intersection of revenue, risk, localization, and operations. Stripe’s $1.9 trillion payment-volume scale, Adyen’s €1,394.3 billion processed volume, ACH’s $93 trillion value, euro-area non-cash transaction scale, UPI’s 2,163 crore monthly transaction milestone, and Pix’s 68.7 billion annual transactions all show that payment infrastructure is now deeply regional and deeply operational.

For business leaders, the most important question is not just, “Can we accept payments?” It is whether customers can pay using familiar methods, whether legitimate transactions are approved smoothly, whether fraud can be managed without blocking genuine buyers, whether funds settle on time, and whether financial records remain clear and organized afterward. A reliable payment system combined with a professional freelance invoice template helps businesses streamline billing, improve customer trust, and create a stronger revenue-capture process rather than simply handling transactions.

That is also why payment gateway statistics should not be read as a ranking of payment providers. The more useful question is fit. A retailer with heavy mobile traffic, a consultant sending invoice links, a SaaS company protecting renewals, and a marketplace paying sellers all need different gateway strengths. The same headline fee can produce very different real costs once failed payments, false positives, settlement delays, refunds, disputes, support time, and reconciliation work are included.

The strongest next step is a measured one: baseline the current gateway, identify where payment failures or reporting gaps are concentrated, and fix the leaks that have clear ownership. Over time, that approach produces a payment setup that is faster, more local, more trusted, easier to reconcile, and better at converting ready-to-pay demand into usable cash.