Industry Reports

Payment Links Statistics

Payment links are one of the simplest payment tools a business can send, but the statistics behind them point to a much larger operating…

Read simple, useful articles on invoicing, templates, payments, cash flow, AI tools, and better small-business workflows.

Payment links are one of the simplest payment tools a business can send, but the statistics behind them point to a much larger operating…

Payment gateways are often described as the invisible bridge between a customer and a merchant, but that definition is too small for how modern…

Online payments are no longer a single checkout feature or a card-processing choice. They are a global mix of digital wallets, cards, bank transfers,…

Late payments are easy to describe as a collections problem, but the data shows something broader. A delayed invoice can change payroll timing, force…

Invoice reminders look simple from the outside: an invoice is sent, the due date arrives, and someone follows up if the money does not…

Invoice payment is the point where a completed job, delivered order, or approved service becomes usable cash. A company can send a correct invoice…

Small-business payment performance is not just a question of whether customers can pay by card. It is the set of everyday decisions that determines how quickly revenue…

Embedded payments are no longer just a payment button inside software. They are the transaction layer that lets a platform accept money, move funds,…

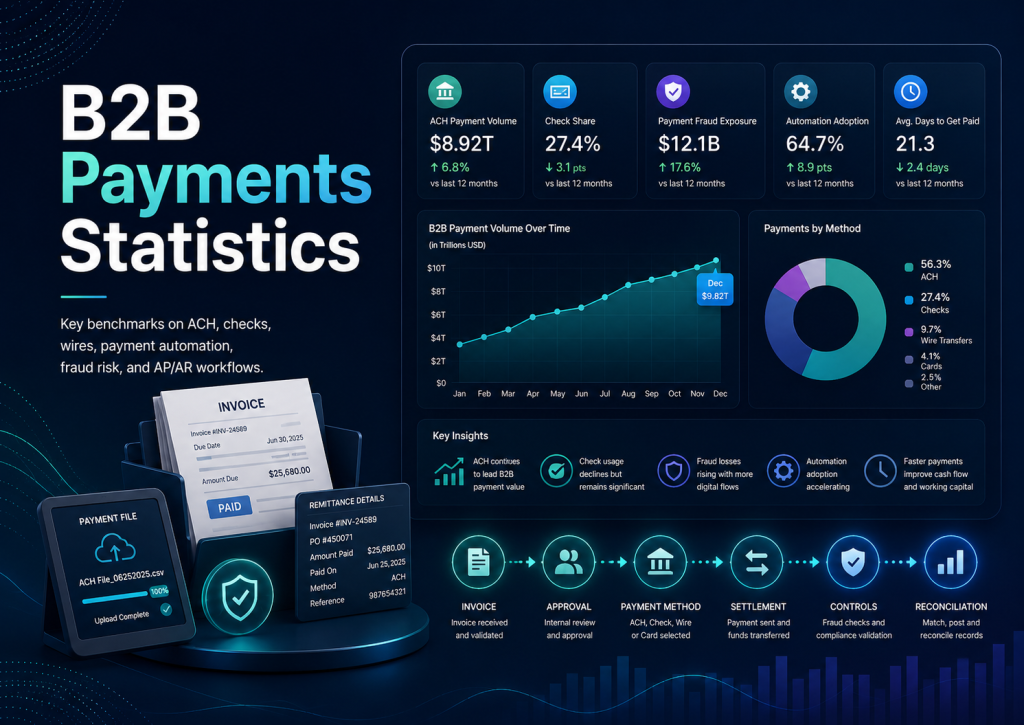

B2B payments look simple only when they are reduced to money moving from one company to another. In practice, the payment is the visible…

A research-backed statistics report on self-employed workers, independent contractors, nonemployer businesses, regional labor-market differences, informal work, income quality, and the future of independent earning.…

A practical statistics report on billable hours, realization, collections, PSA software, e-invoicing, late payments, regional adoption, and the financial controls that help consulting, legal,…

The freelance economy is no longer a narrow side-hustle category. It is a broad labor system that includes full-time independent professionals, occasional project workers,…