Industry Reports

Open Banking Statistics

Open banking allows customers and businesses to share financial data securely with authorized third parties through APIs. The model changes how lenders assess risk,…

Read simple, useful articles on invoicing, templates, payments, cash flow, AI tools, and better small-business workflows.

Open banking allows customers and businesses to share financial data securely with authorized third parties through APIs. The model changes how lenders assess risk,…

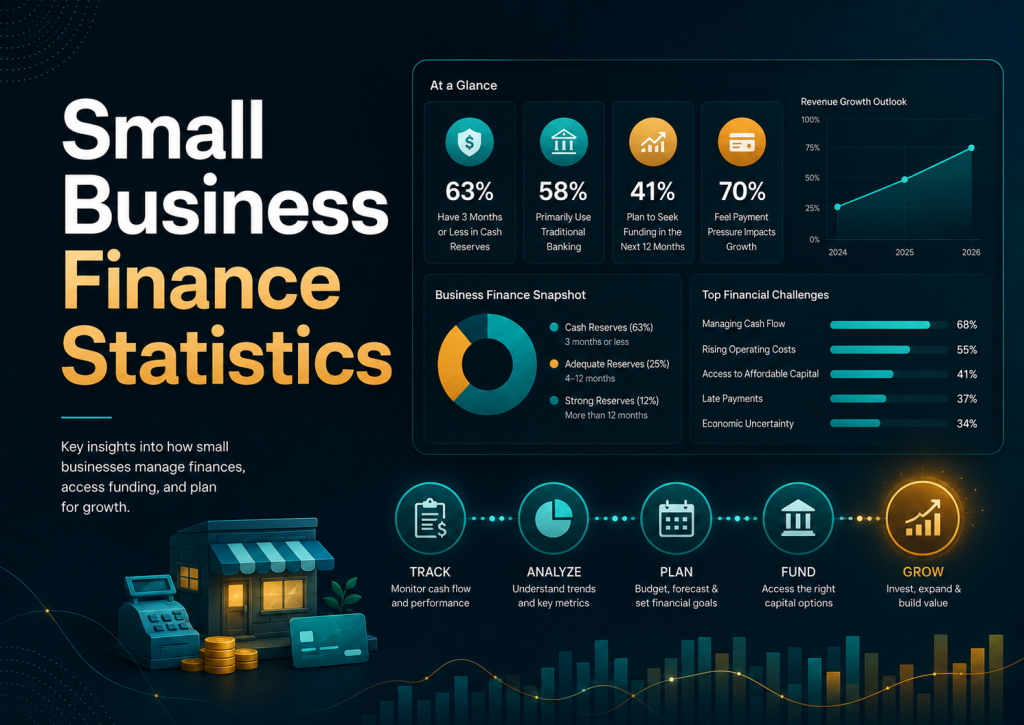

Small-business finance is broader than loans. It includes cash reserves, payment timing, credit use, owner contributions, bookkeeping discipline, vendor terms, receivables collection, tax readiness,…

Invoice financing lets companies borrow against unpaid invoices without necessarily selling the receivable outright. It sits between everyday collections management and broader working-capital finance.…

Factoring services convert unpaid invoices into near-term liquidity by allowing a business to sell receivables or receive an advance against customer invoices. The service…

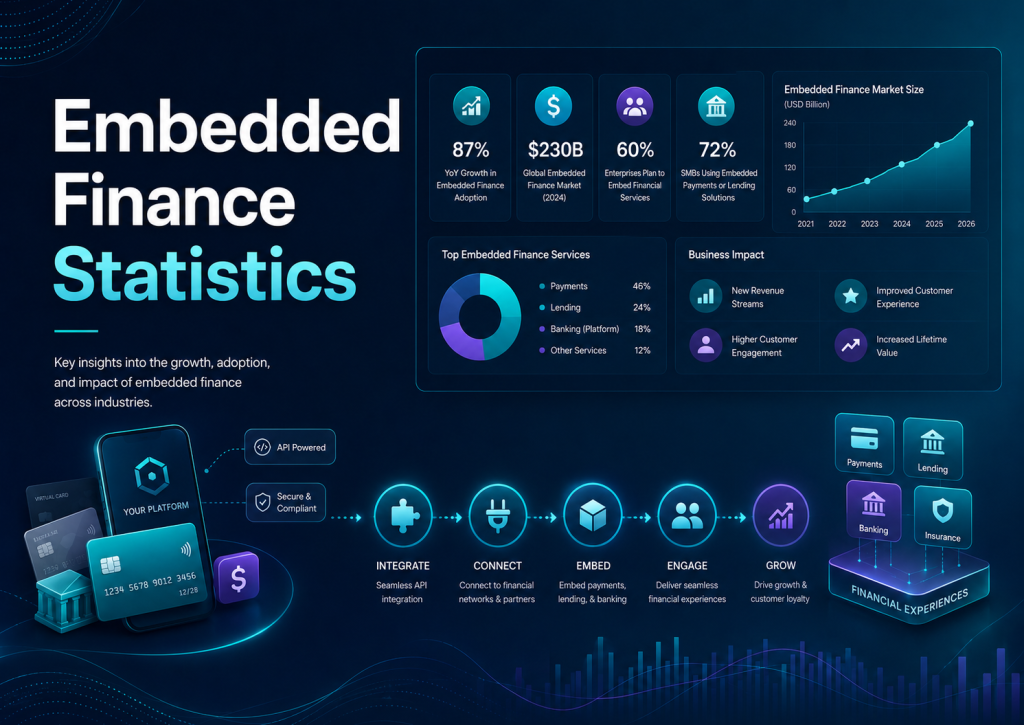

Embedded finance is the practice of placing payments, lending, insurance, banking, cards, or financial accounts inside non-financial customer journeys. The category matters because financial…

Business Banking Statistics looks at how business banking is changing the way businesses manage finance work, reporting, payments, and day-to-day decisions. The numbers matter…

Time Tracking Software Statistics is a detailed research by Zintego’s Editorial Team which looks at how time tracking software is changing the way businesses…

Small Business Accounting Statistics looks at how small business accounting is changing the way businesses manage finance work, reporting, payments, and day-to-day decisions. The…

Key insights on project billing statistics, market growth, workflow quality, automation, cash-flow visibility, controls, and finance-team productivity. Project Billing Statistics looks at how project…

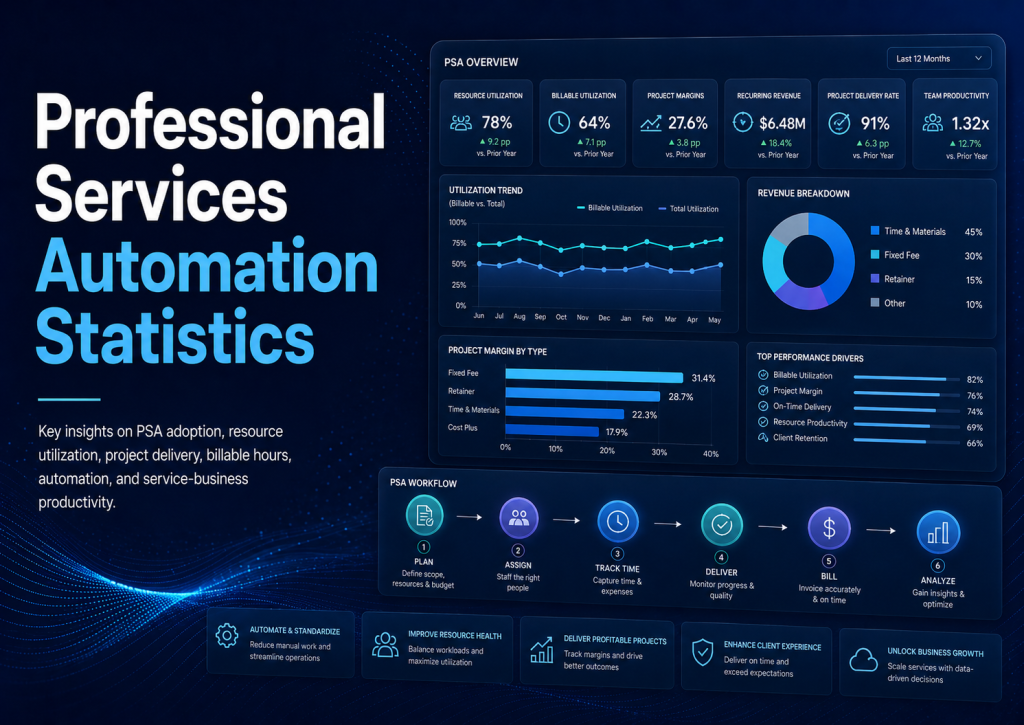

Professional Services Automation Statistics looks at how professional services automation is changing the way businesses manage finance work, reporting, payments, and day-to-day decisions. The…

Invoice Automation Statistics looks at how invoice automation is changing the way businesses manage finance work, reporting, payments, and day-to-day decisions. The numbers matter…

Expense Management Statistics looks at how expense management software is changing the way businesses manage finance work, reporting, payments, and day-to-day decisions. The numbers…